|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

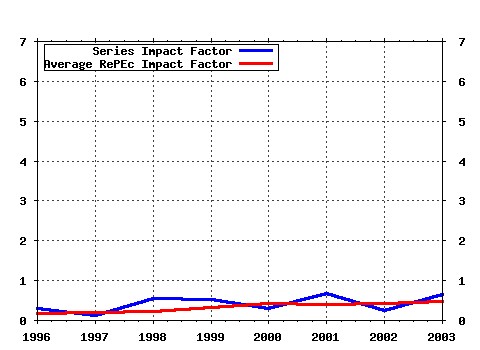

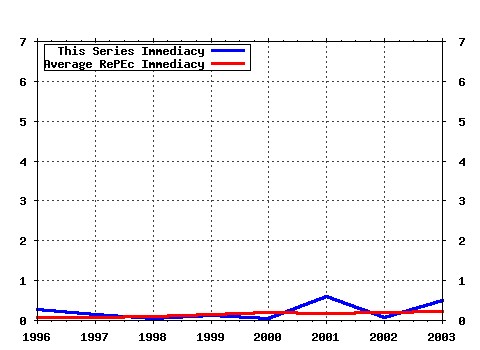

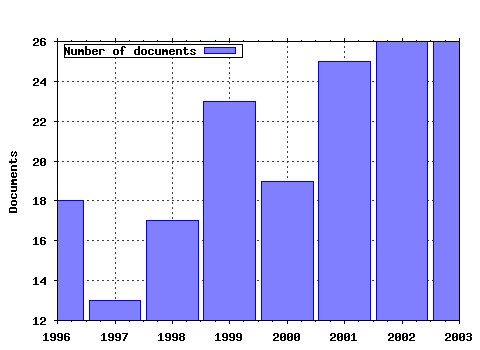

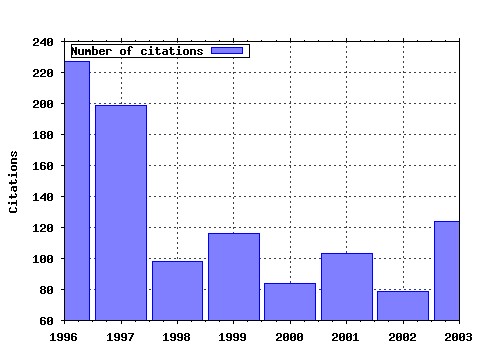

Journal of Empirical Finance Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:empfin:v:1:y:1993:i:1:p:83-106 A long memory property of stock market returns and a new model (1993). Journal of Empirical Finance (2) RePEc:eee:empfin:v:3:y:1996:i:2:p:123-192 The forward discount anomaly and the risk premium: A survey of recent evidence (1996). Journal of Empirical Finance (3) RePEc:eee:empfin:v:4:y:1997:i:2-3:p:115-158 Intraday periodicity and volatility persistence in financial markets (1997). Journal of Empirical Finance (4) RePEc:eee:empfin:v:3:y:1996:i:1:p:15-102 The econometrics of financial markets (1996). Journal of Empirical Finance (5) RePEc:eee:empfin:v:5:y:1998:i:4:p:397-416 Volatility and cross correlation across major stock markets (1998). Journal of Empirical Finance (6) RePEc:eee:empfin:v:4:y:1997:i:2-3:p:73-114 High frequency data in financial markets: Issues and applications (1997). Journal of Empirical Finance (7) RePEc:eee:empfin:v:4:y:1997:i:4:p:317-340 The incremental volatility information in one million foreign exchange quotations (1997). Journal of Empirical Finance (8) RePEc:eee:empfin:v:10:y:2003:i:1-2:p:3-56 Emerging markets finance (2003). Journal of Empirical Finance (9) RePEc:eee:empfin:v:1:y:1994:i:3-4:p:313-341 Alternative constructions of Tobins q: An empirical comparison (1994). Journal of Empirical Finance (10) RePEc:eee:empfin:v:9:y:2002:i:5:p:495-510 Market timing and return prediction under model instability (2002). Journal of Empirical Finance (11) RePEc:eee:empfin:v:6:y:1999:i:5:p:457-477 Forecasting financial market volatility: Sample frequency vis-a-vis forecast horizon (1999). Journal of Empirical Finance (12) RePEc:eee:empfin:v:4:y:1997:i:2-3:p:213-239 Volatilities of different time resolutions -- Analyzing the dynamics of market components (1997). Journal of Empirical Finance (13) RePEc:eee:empfin:v:10:y:2003:i:1-2:p:81-103 A simple measure of the intensity of capital controls (2003). Journal of Empirical Finance (14) RePEc:eee:empfin:v:9:y:2002:i:3:p:271-285 Asymmetric information and price discovery in the FX market: does Tokyo know more about the yen? (2002). Journal of Empirical Finance (15) RePEc:eee:empfin:v:8:y:2001:i:5:p:573-637 The specification of conditional expectations (2001). Journal of Empirical Finance (16) RePEc:eee:empfin:v:7:y:2000:i:3-4:p:271-300 Estimation of tail-related risk measures for heteroscedastic financial time series: an extreme value approach (2000). Journal of Empirical Finance (17) RePEc:eee:empfin:v:7:y:2000:i:3-4:p:225-245 Sensitivity analysis of Values at Risk (2000). Journal of Empirical Finance (18) RePEc:eee:empfin:v:1:y:1994:i:2:p:133-160 A contingent claim approach to performance evaluation (1994). Journal of Empirical Finance (19) RePEc:eee:empfin:v:1:y:1994:i:2:p:211-248 Testing the covariance stationarity of heavy-tailed time series: An overview of the theory with applications to several financial datasets (1994). Journal of Empirical Finance (20) RePEc:eee:empfin:v:8:y:2001:i:5:p:459-491 Why long horizons? A study of power against persistent alternatives (2001). Journal of Empirical Finance (21) RePEc:eee:empfin:v:4:y:1997:i:4:p:295-315 Public information releases, private information arrival and volatility in the foreign exchange market (1997). Journal of Empirical Finance (22) RePEc:eee:empfin:v:4:y:1997:i:2-3:p:187-212 Forecasting the frequency of changes in quoted foreign exchange prices with the autoregressive conditional duration model (1997). Journal of Empirical Finance (23) RePEc:eee:empfin:v:1:y:1993:i:1:p:3-31 Common stock offerings across the business cycle : Theory and evidence (1993). Journal of Empirical Finance (24) RePEc:eee:empfin:v:10:y:2003:i:4:p:505-531 Univariate and multivariate stochastic volatility models: estimation and diagnostics (2003). Journal of Empirical Finance (25) RePEc:eee:empfin:v:6:y:1999:i:2:p:193-215 Real exchange rates and nontradables: A relative price approach (1999). Journal of Empirical Finance (26) RePEc:eee:empfin:v:4:y:1997:i:1:p:17-46 An artificial neural network-GARCH model for international stock return volatility (1997). Journal of Empirical Finance (27) RePEc:eee:empfin:v:1:y:1993:i:1:p:107-131 International asset pricing with alternative distributional specifications (1993). Journal of Empirical Finance (28) RePEc:eee:empfin:v:5:y:1998:i:3:p:281-296 International evidence on the stock market and aggregate economic activity (1998). Journal of Empirical Finance (29) RePEc:eee:empfin:v:6:y:1999:i:4:p:335-353 Multivariate unit root tests of the PPP hypothesis (1999). Journal of Empirical Finance (30) RePEc:eee:empfin:v:8:y:2001:i:1:p:83-110 Recovering the probability density function of asset prices using garch as diffusion approximations (2001). Journal of Empirical Finance (31) RePEc:eee:empfin:v:8:y:2001:i:3:p:325-342 Testing and comparing Value-at-Risk measures (2001). Journal of Empirical Finance (32) RePEc:eee:empfin:v:6:y:1999:i:3:p:309-331 A primer on hedge funds (1999). Journal of Empirical Finance (33) RePEc:eee:empfin:v:7:y:2000:i:5:p:531-554 Value-at-Risk: a multivariate switching regime approach (2000). Journal of Empirical Finance (34) RePEc:eee:empfin:v:2:y:1995:i:3:p:225-251 The relationship between GARCH and symmetric stable processes: Finding the source of fat tails in financial data (1995). Journal of Empirical Finance (35) RePEc:eee:empfin:v:2:y:1995:i:1:p:71-93 Small sample rank tests with applications to asset pricing (1995). Journal of Empirical Finance (36) RePEc:eee:empfin:v:11:y:2004:i:3:p:379-398 Modelling daily Value-at-Risk using realized volatility and ARCH type models (2004). Journal of Empirical Finance (37) RePEc:eee:empfin:v:2:y:1995:i:3:p:173-197 The structure of international stock returns and the integration of capital markets (1995). Journal of Empirical Finance (38) RePEc:eee:empfin:v:1:y:1994:i:3-4:p:279-311 Neglected common factors in exchange rate volatility (1994). Journal of Empirical Finance (39) RePEc:eee:empfin:v:3:y:1996:i:2:p:215-238 Unit roots and the estimation of interest rate dynamics (1996). Journal of Empirical Finance (40) RePEc:eee:empfin:v:6:y:1999:i:4:p:355-384 Mean reversion in Southeast Asian stock markets (1999). Journal of Empirical Finance (41) RePEc:eee:empfin:v:10:y:2003:i:5:p:641-660 Central bank interventions and jumps in double long memory models of daily exchange rates (2003). Journal of Empirical Finance (42) RePEc:eee:empfin:v:7:y:2000:i:1:p:87-111 Coincident and leading indicators of the stock market (2000). Journal of Empirical Finance (43) RePEc:eee:empfin:v:8:y:2001:i:2:p:111-155 Testing for mean-variance spanning: a survey (2001). Journal of Empirical Finance (44) RePEc:eee:empfin:v:1:y:1993:i:1:p:33-55 The performance of international asset allocation strategies using conditioning information (1993). Journal of Empirical Finance (45) RePEc:eee:empfin:v:8:y:2001:i:5:p:537-572 The independence axiom and asset returns (2001). Journal of Empirical Finance (46) RePEc:eee:empfin:v:4:y:1997:i:4:p:341-372 The analysis of foreign exchange data using waveform dictionaries (1997). Journal of Empirical Finance (47) RePEc:eee:empfin:v:11:y:2004:i:3:p:399-421 Occasional structural breaks and long memory with an application to the S&P 500 absolute stock returns (2004). Journal of Empirical Finance (48) RePEc:eee:empfin:v:12:y:2005:i:3:p:476-489 Testing for contagion: a conditional correlation analysis (2005). Journal of Empirical Finance (49) RePEc:eee:empfin:v:6:y:1999:i:2:p:177-192 Target zones and conditional volatility: The role of realignments (1999). Journal of Empirical Finance (50) RePEc:eee:empfin:v:7:y:2000:i:5:p:509-530 Bivariate FIGARCH and fractional cointegration (2000). Journal of Empirical Finance Latest citations received in: | 2003 | 2002 | 2001 | 2000 Latest citations received in: 2003 (1) RePEc:cfs:cfswop:wp200335 Some Like it Smooth, and Some Like it Rough: Untangling Continuous and Jump Components in Measuring, Modeling, and Forecasting Asset Return Volatility (2003). Center for Financial Studies / CFS Working Paper Series (2) RePEc:dgr:umamet:2003057 Central Bank Forex Interventions Assessed Using Realized Moments (2003). Maastricht : METEOR, Maastricht Research School of Economics of Technology and Organization / Research Memoranda (3) RePEc:fip:fedcwp:0315 Government intervention in the foreign exchange market (2003). Federal Reserve Bank of Cleveland / Working Paper (4) RePEc:fip:fedgif:755 Diversification, original sin, and international bond portfolios (2003). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (5) RePEc:fip:fedgif:770 Cross-board listings, capital controls, and equity flows to emerging markets (2003). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (6) RePEc:fip:fedgif:771 U.S. investors emerging market equity portfolios: a security-level analysis (2003). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (7) RePEc:hhs:umnees:0614 Temporal Aggregation of the Returns of a Stock Index Series (2003). Umeå University, Department of Economics / Umeå Economic Studies (8) RePEc:imf:imfwpa:03/236 Cross-Border Listings, Capital Controls, and U.S. Equity Flows to Emerging Markets (2003). International Monetary Fund / IMF Working Papers (9) RePEc:imf:imfwpa:03/238 U.S. Investors Emerging Market Equity Portfolios: A Security-Level Analysis (2003). International Monetary Fund / IMF Working Papers (10) RePEc:imf:imfwpa:03/86 International Financial Integration (2003). International Monetary Fund / IMF Working Papers (11) RePEc:ind:icrier:109 The Dynamics of foreign portfolio inflows and equity returns in India (2003). Indian Council for Research on International Economic Relations, New Delhi, India / Indian Council for Research on International Economic Relations, (12) RePEc:ivi:wpasad:2003-34 FORECASTING THE CONDITIONAL COVARIANCE MATRIX OF A PORTFOLIO UNDER LONG-RUN TEMPORAL DEPENDENCE (2003). Instituto Valenciano de Investigaciones Económicas, S.A. (Ivie) / Working Papers. Serie AD (13) RePEc:wpa:wuwpfi:0305007 CONDITIONAL VOLATILITY OF MOST ACTIVE SHARES OF CASABLANCA STOCK EXCHANGE (2003). EconWPA / Finance Latest citations received in: 2002 (1) RePEc:cte:wsrepe:ws025414 ESTIMATION METHODS FOR STOCHASTIC VOLATILITY MODELS: A SURVEY (2002). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (2) RePEc:fip:fedkrw:rwp02-05 Forecast-based model selection in the presence of structural breaks (2002). Federal Reserve Bank of Kansas City / Research Working Paper Latest citations received in: 2001 (1) RePEc:bdi:wptemi:td_399_01 Labor Income and Risky Assets under Market Incompleteness: Evidence from Italian Data (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (2) RePEc:bdi:wptemi:td_400_01 Is the Italian Labour market segmented? (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (3) RePEc:bdi:wptemi:td_404_01 The Effects of Bank Consolidation and Market Entry on Small Business Lending (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (4) RePEc:bdi:wptemi:td_405_01 Money demand in the euro area: do national differences matter? (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (5) RePEc:bdi:wptemi:td_406_01 The Evolution of Confidence for European Consumers and Businesses in France, Germany and Italy (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (6) RePEc:bdi:wptemi:td_411_01 Why is the Business-Cycle Behavior of Fundamentals Alike Across Exchange-Rate Regimes? (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (7) RePEc:bdi:wptemi:td_412_01 Political Institutions and Policy Outcomes: What are the Stylized Facts? (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (8) RePEc:bdi:wptemi:td_414_01 Insurance within the Firm (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (9) RePEc:bdi:wptemi:td_415_01 Limited Financial Market Participation: A Transaction Cost-Based Explanation (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (10) RePEc:bdi:wptemi:td_418_01 Ingredients for the New Economy: How Much does finance matter? (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (11) RePEc:bdi:wptemi:td_419_01 ICT accumulation and productivity growth in the United States: an analysis based on industry data (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (12) RePEc:fip:fedawp:2001-24 Minimum-variance kernels, economic risk premia, and tests of multi-beta models (2001). Federal Reserve Bank of Atlanta / Working Paper (13) RePEc:fip:fedfap:2002-06 Macro factors and the affine term structure of interest rates (2001). Federal Reserve Bank of San Francisco / Working Papers in Applied Economic Theory (14) RePEc:nbr:nberwo:8678 Expectations of Equity Risk Premia, Volatility and Asymmetry from a Corporate Finance Perspective (2001). National Bureau of Economic Research, Inc / NBER Working Papers (15) RePEc:nzt:nztwps:01/32 Saving and growth in an open economy (2001). New Zealand Treasury / Treasury Working Paper Series Latest citations received in: 2000 (1) RePEc:bcb:wpaper:7 Leading Indicators of Inflation for Brazil (2000). Central Bank of Brazil, Research Department / Working Papers Series Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |