|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

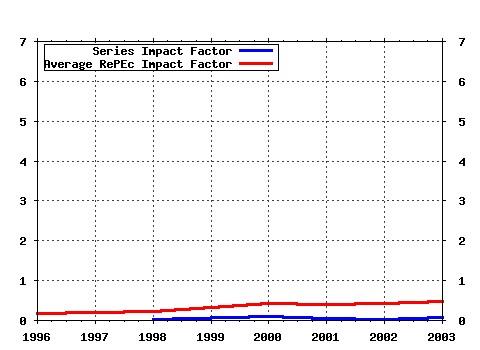

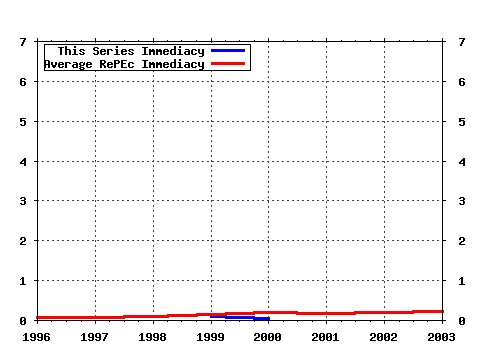

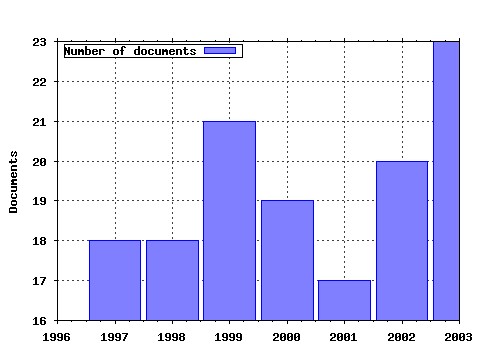

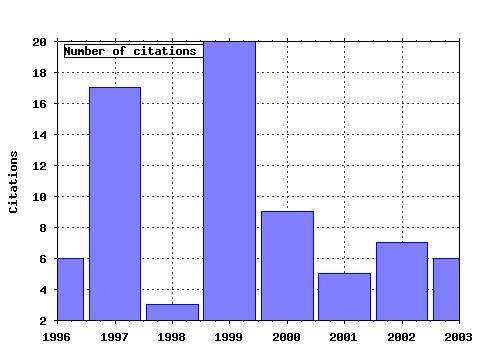

Journal of Accounting and Public Policy Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:jappol:v:16:y:1997:i:1:p:1-34 Determinants of the variability in corporate effective tax rates: Evidence from longitudinal data (1997). Journal of Accounting and Public Policy (2) RePEc:eee:jappol:v:2:y:1983:i:4:p:289-307 Failure prediction: Sensitivity of classification accuracy to alternative statistical methods and variable sets (1983). Journal of Accounting and Public Policy (3) RePEc:eee:jappol:v:18:y:1999:i:2:p:179-180 Discussion (1999). Journal of Accounting and Public Policy (4) RePEc:eee:jappol:v:14:y:1995:i:3:p:179-201 Evidence on opinion shopping from audit opinion conservatism (1995). Journal of Accounting and Public Policy (5) RePEc:eee:jappol:v:13:y:1994:i:1:p:79-94 The ethics of managing earnings: An empirical investigation (1994). Journal of Accounting and Public Policy (6) RePEc:eee:jappol:v:19:y:2000:i:4-5:p:313-345 Research design issues in earnings management studies (2000). Journal of Accounting and Public Policy (7) RePEc:eee:jappol:v:8:y:1989:i:1:p:1-27 Taxpayer compliance under uncertainty (1989). Journal of Accounting and Public Policy (8) RePEc:eee:jappol:v:13:y:1994:i:2:p:121-139 The use of audit committees for monitoring (1994). Journal of Accounting and Public Policy (9) RePEc:eee:jappol:v:18:y:1999:i:2:p:97-98 Editorial (1999). Journal of Accounting and Public Policy (10) RePEc:eee:jappol:v:18:y:1999:i:2:p:165-177 Taxpayer behavior in response to taxation: comment and new experimental evidence (1999). Journal of Accounting and Public Policy (11) RePEc:eee:jappol:v:17:y:1998:i:4-5:p:329-329 Editorial (1998). Journal of Accounting and Public Policy (12) RePEc:eee:jappol:v:16:y:1997:i:2:p:215-241 Investors assessment of implicit environmental liabilities: An empirical investigation (1997). Journal of Accounting and Public Policy (13) RePEc:eee:jappol:v:15:y:1996:i:2:p:161-181 A revised classification pattern of hospital financial ratios (1996). Journal of Accounting and Public Policy (14) RePEc:eee:jappol:v:22:y:2003:i:4:p:325-345 Corporate governance and voluntary disclosure (2003). Journal of Accounting and Public Policy (15) RePEc:eee:jappol:v:20:y:2001:i:2:p:129-153 Non-US Firms Accounting Standard Choices (2001). Journal of Accounting and Public Policy (16) RePEc:eee:jappol:v:19:y:2000:i:4-5:p:347-376 Identifying unexpected accruals: a comparison of current approaches (2000). Journal of Accounting and Public Policy (17) RePEc:eee:jappol:v:9:y:1990:i:1:p:19-36 The incentives for voluntary audit committee formation (1990). Journal of Accounting and Public Policy (18) RePEc:eee:jappol:v:25:y:2006:i:4:p:409-434 Corporate governance and firm valuation (2006). Journal of Accounting and Public Policy (19) RePEc:eee:jappol:v:15:y:1996:i:2:p:111-136 Forecast disclosure by initial public offering firms in a low-litigation environment (1996). Journal of Accounting and Public Policy (20) RePEc:eee:jappol:v:24:y:2005:i:5:p:431-447 Earnings-based bonus plans and the agency costs of debt (2005). Journal of Accounting and Public Policy (21) RePEc:eee:jappol:v:18:y:1999:i:2:p:99-139 The farmers home administration and farm debt failure prediction (1999). Journal of Accounting and Public Policy (22) RePEc:eee:jappol:v:7:y:1988:i:1:p:1-28 Taxpayer behavior in response to taxation: An experimental analysis (1988). Journal of Accounting and Public Policy (23) RePEc:eee:jappol:v:21:y:2002:i:2:p:137-145 Enron: sad but inevitable (2002). Journal of Accounting and Public Policy (24) RePEc:eee:jappol:v:9:y:1990:i:2:p:79-110 Financial disclosure regulation and its environment: A review and further analysis (1990). Journal of Accounting and Public Policy (25) RePEc:eee:jappol:v:8:y:1989:i:3:p:199-217 Political interests and governmental accounting disclosure (1989). Journal of Accounting and Public Policy (26) RePEc:eee:jappol:v:14:y:1995:i:4:p:311-368 Firm-specific determinants of the comprehensiveness of mandatory disclosure in the corporate annual reports of firms listed on the stock exchange of Hong Kong (1995). Journal of Accounting and Public Policy (27) RePEc:eee:jappol:v:21:y:2002:i:4-5:p:371-394 The determinants of Internet financial reporting (2002). Journal of Accounting and Public Policy (28) RePEc:eee:jappol:v:16:y:1997:i:3:p:271-309 Detecting GAAP violation: implications for assessing earnings management among firms with extreme financial performance (1997). Journal of Accounting and Public Policy (29) RePEc:eee:jappol:v:14:y:1995:i:3:p:233-261 Financial analysts earnings forecasts and insider trading (1995). Journal of Accounting and Public Policy (30) RePEc:eee:jappol:v:21:y:2002:i:2:p:147-149 Regulatory competition for low cost-of-capital accounting rules (2002). Journal of Accounting and Public Policy (31) RePEc:eee:jappol:v:16:y:1997:i:2:p:187-214 Environmental regulations and incentives for compliance audits (1997). Journal of Accounting and Public Policy (32) RePEc:eee:jappol:v:14:y:1995:i:2:p:143-160 An application of data envelopment analysis to public sector performance measurement and accountability (1995). Journal of Accounting and Public Policy (33) RePEc:eee:jappol:v:21:y:2002:i:2:p:105-127 Enron: what happened and what we can learn from it (2002). Journal of Accounting and Public Policy (34) RePEc:eee:jappol:v:3:y:1984:i:2:p:91-106 The role of generally accepted reporting methods in the public sector: An empirical test (1984). Journal of Accounting and Public Policy (35) RePEc:eee:jappol:v:11:y:1992:i:1:p:1-42 An empirical analysis of theories on factors influencing state government accounting disclosure (1992). Journal of Accounting and Public Policy (36) RePEc:eee:jappol:v:6:y:1987:i:1:p:35-57 Lobbying against proposed accounting standards: The case of employers pension accounting (1987). Journal of Accounting and Public Policy (37) RePEc:eee:jappol:v:13:y:1994:i:2:p:141-158 The voluntary review of earnings forecasts disclosed in IPO prospectuses (1994). Journal of Accounting and Public Policy (38) RePEc:eee:jappol:v:20:y:2001:i:2:p:97-128 Off-balance sheet R&D assets and market liquidity (2001). Journal of Accounting and Public Policy (39) RePEc:eee:jappol:v:8:y:1989:i:4:p:239-265 Voluntary formation of corporate audit committees among NASDAQ firms (1989). Journal of Accounting and Public Policy (40) RePEc:eee:jappol:v:10:y:1991:i:2:p:105-134 The influence of political competition on the decision to adopt GAAP (1991). Journal of Accounting and Public Policy (41) RePEc:eee:jappol:v:18:y:1999:i:4-5:p:311-332 Audit committee activity and agency costs (1999). Journal of Accounting and Public Policy (42) RePEc:eee:jappol:v:22:y:2003:i:3:p:203-230 Governance structures and accounting at large municipalities (2003). Journal of Accounting and Public Policy (43) RePEc:eee:jappol:v:5:y:1986:i:4:p:267-285 Accounting measures of unfunded pension liabilities and the expected present value of future pension cash flows (1986). Journal of Accounting and Public Policy (44) RePEc:eee:jappol:v:16:y:1997:i:4:p:339-353 Trends in independent auditor liability: The emergence of a sane consensus? (1997). Journal of Accounting and Public Policy (45) RePEc:eee:jappol:v:1:y:1982:i:1:p:5-17 An analysis of the role of accounting standards for enhancing corporate governance and social responsibility (1982). Journal of Accounting and Public Policy (46) RePEc:eee:jappol:v:14:y:1995:i:4:p:265-291 Gender and earnings of certain accountants and auditors: A comparative study of industries and regions (1995). Journal of Accounting and Public Policy (47) RePEc:eee:jappol:v:21:y:2002:i:4-5:p:357-369 Dissemination of information for investors at corporate Web sites (2002). Journal of Accounting and Public Policy (48) RePEc:eee:jappol:v:4:y:1985:i:3:p:201-223 Cultural influence on corporate and governmental involvement in accounting policy determination in Japan (1985). Journal of Accounting and Public Policy (49) RePEc:eee:jappol:v:12:y:1993:i:2:p:113-133 The effect of supplemental reserve-based accounting data on the market microstructure (1993). Journal of Accounting and Public Policy (50) RePEc:eee:jappol:v:19:y:2000:i:4-5:p:399-420 Earnings management under changing regulatory regimes: state accreditation in the insurance industry (2000). Journal of Accounting and Public Policy Latest citations received in: | 2003 | 2002 | 2001 | 2000 Latest citations received in: 2003 Latest citations received in: 2002 Latest citations received in: 2001 Latest citations received in: 2000 (1) RePEc:taf:euract:v:9:y:2000:i:4:p:499-517 To whom are IAS earnings informative? Domestic versus foreign shareholders perspectives (2000). European Accounting Review Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |