|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

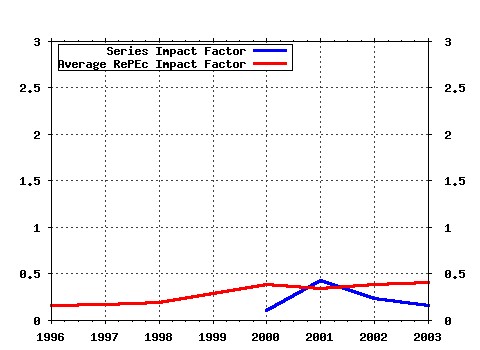

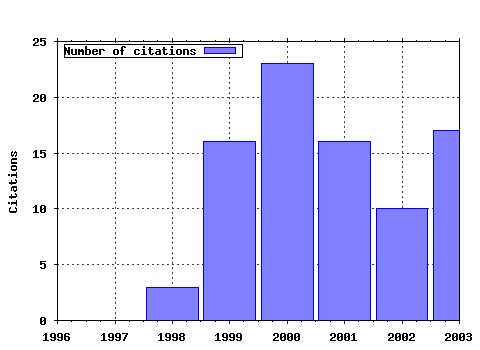

International Center for Financial Asset Management and Engineering / FAME Research Paper Series Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:fam:rpseri:rp13 European Financial Markets After EMU: A First Assessment (2000). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (2) RePEc:fam:rpseri:rp11 Dynamic Consumption and Portfolio Choice with Stochastic Volatility in Incomplete Markets (1999). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (3) RePEc:fam:rpseri:rp34 Variable Selection for Portfolio Choice (2001). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (4) RePEc:fam:rpseri:rp156 Rational Inattention: A Solution to the Forward Discount Puzzle (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (5) RePEc:fam:rpseri:rp100 Mutual Fund Flows and Performance in Rational Markets (2002). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (6) RePEc:fam:rpseri:rp84 European Financial Integration and Equity Returns: A Theory-Based Assessment (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (7) RePEc:fam:rpseri:rp155 Can Information Heterogeneity Explain the Exchange Rate Determination? (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (8) RePEc:fam:rpseri:rp130 Financial Intermediation and the Costs of Trading in an Opaque Market (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (9) RePEc:fam:rpseri:rp32 Portfolio Diversification: Alive and Well in Euroland! (2001). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (10) RePEc:fam:rpseri:rp5 Who Should Buy Long-Term Bonds? (1998). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (11) RePEc:fam:rpseri:rp57 Nonparametric Estimation of Copulas for Time Series (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (12) RePEc:fam:rpseri:rp76 Profitable Innovation Without Patent Protection: The Case of Derivatives. (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (13) RePEc:fam:rpseri:rp18 Extreme Value Theory for Tail-Related Risk Measures (2000). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (14) RePEc:fam:rpseri:rp110 Higher Order Expectations in Asset Pricing (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (15) RePEc:fam:rpseri:rp119 A Simple Alternative House Price Index Method (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (16) RePEc:fam:rpseri:rp35 Country, Sector or Style: What Matters Most When Constructing Global Equity Portfolios? An Empirical Investigation from 1990-2001 (2001). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (17) RePEc:fam:rpseri:rp122 Investment under Uncertainty and Incomplete Markets (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (18) RePEc:fam:rpseri:rp136 Direct Preference Wealth in Aggregate Household Portfolios (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (19) RePEc:fam:rpseri:rp67 Linear-Quadratic Jump-Diffusion Modeling with Application to Stochastic Volatility (2002). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (20) RePEc:fam:rpseri:rp117 Equity Returns and Integration: Is Europe Changing? (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (21) RePEc:fam:rpseri:rp93 A Simple Calibration Procedure of Stochastic Volatility Models with Jumps by Short Term Asymptotics (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (22) RePEc:fam:rpseri:rp132 Conditional Asset Allocation under Non-Normality: How Costly is the Mean-Variance Criterion? (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (23) RePEc:fam:rpseri:rp59 Implicit Forward Rents as Predictors of Future Rents (2002). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (24) RePEc:fam:rpseri:rp16 Prospect Theory and Asset Prices (2000). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (25) RePEc:fam:rpseri:rp108 SOME STATISTICAL PITFALLS IN COPULA MODELING FOR FINANCIAL APPLICATIONS (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (26) RePEc:fam:rpseri:rp77 Competition Between Stock Exchanges: A Survey (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (27) RePEc:fam:rpseri:rp125 Capital Structure, Credit Risk, and Macroeconomic Conditions (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (28) RePEc:fam:rpseri:rp103 Portfolio Optimization with Concave Transaction Costs (2002). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (29) RePEc:fam:rpseri:rp138 Growth Options in General Equilibrium: Some Asset Pricing Implications (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (30) RePEc:fam:rpseri:rp68 The capital structure of Swiss companies: an empirical analysis using dynamic panel data (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (31) RePEc:fam:rpseri:rp31 EMU and Portfolio Diversification Opportunities (2000). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (32) RePEc:fam:rpseri:rp99 Irreversible Investment with Regime Shifts (2002). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (33) RePEc:fam:rpseri:rp133 Are European Corporate Bond and Default Swap Markets Segmented? (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (34) RePEc:fam:rpseri:rp66 Optimal asset allocation for pension funds under mortality risk during the accumulation and ecumulation phases (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (35) RePEc:fam:rpseri:rp112 Nonparametric Estimation of Conditional Expected Shortfall (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (36) RePEc:fam:rpseri:rp163 False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (37) RePEc:fam:rpseri:rp88 The Macroeconomics of Delegated Management (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (38) RePEc:fam:rpseri:rp78 Why Government Bonds Are Sold by Auction and Corporate Bonds by Posted-Price Selling (2003). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (39) RePEc:fam:rpseri:rp126 The Dynamics of Mergers and Acquisitions (2004). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (40) RePEc:fam:rpseri:rp107 Theory and Calibration of Swap Market Models (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series (41) RePEc:fam:rpseri:rp151 Spatial Dependence, Housing Submarkets, and House Prices (2005). International Center for Financial Asset Management and Engineering / FAME Research Paper Series Latest citations received in: | 2003 | 2002 | 2001 | 2000 Latest citations received in: 2003 (1) RePEc:ecb:ecbwps:20030230 The Euro area financial system: structure, integration and policy initiatives. (2003). European Central Bank / Working Paper Series (2) RePEc:fip:fednsr:162 Nonparametric pricing of multivariate contingent claims (2003). Federal Reserve Bank of New York / Staff Reports (3) RePEc:tcd:tcduee:20034 Divergent Inflation Rates in EMU (2003). Trinity College Dublin, Department of Economics / Trinity Economics Papers Latest citations received in: 2002 Latest citations received in: 2001 (1) RePEc:cdl:anderf:1003 Dynamic Portfolio Choice: A Simulation Approach (2001). Anderson Graduate School of Management, UCLA / University of California at Los Angeles, Anderson Graduate School of Management (2) RePEc:cpr:ceprdp:3070 A Multivariate Model of Strategic Asset Allocation (2001). C.E.P.R. Discussion Papers / CEPR Discussion Papers (3) RePEc:cte:wbrepe:wb012308 OPTIMAL DEMAND FOR LONG-TERM BONDS WHEN RETURNS ARE PREDICTABLE (2001). Universidad Carlos III, Departamento de Economía de la Empresa / Business Economics Working Papers (4) RePEc:nbr:nberwo:8566 A Multivariate Model of Strategic Asset Allocation (2001). National Bureau of Economic Research, Inc / NBER Working Papers Latest citations received in: 2000 (1) RePEc:ecb:ecbops:20020001 The impact of the euro on money and bond markets (2000). European Central Bank / Occasional Paper Series (2) RePEc:kie:kieliw:1004 Financial Market Integration in the US: Lessons for Europe? (2000). Kiel Institute for World Economics / Working Papers (3) RePEc:wop:chispw:529 Belief-dependent Utilities, Aversion to State-Uncertainty and Asset Prices, (2000). Center for Research in Security Prices, Graduate School of Business, University of Chicago / CRSP working papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |