|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

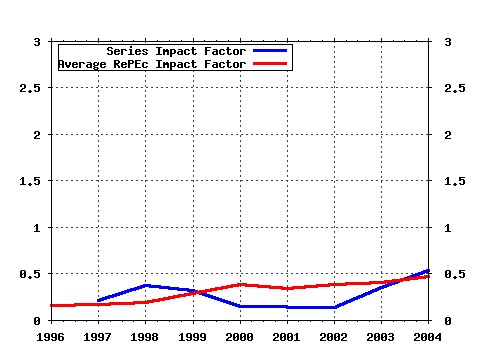

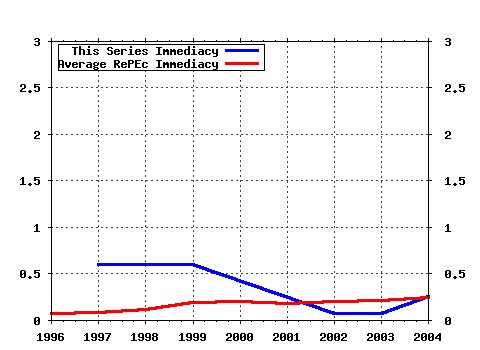

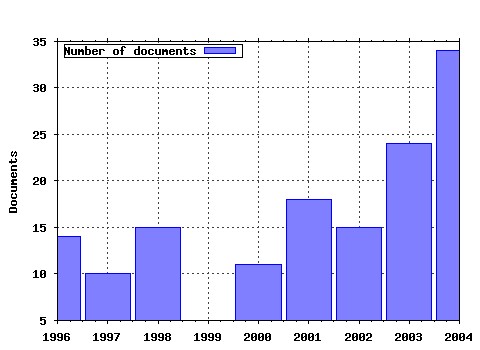

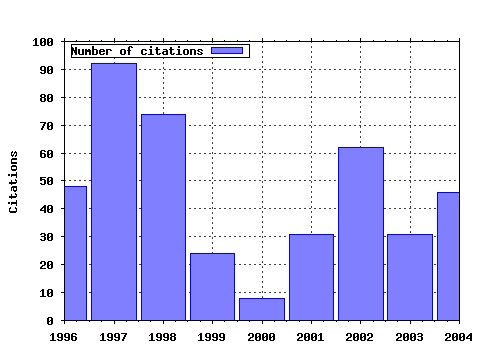

Studies in Nonlinear Dynamics & Econometrics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:bep:sndecm:2:1997:1:1-14 Inference in TAR Models (1997). (2) RePEc:bep:sndecm:3:1998:1:23-42 The Decomposition of Economic Relationships by Time Scale Using Wavelets: Expenditure and Income (1998). (3) RePEc:bep:sndecm:6:2002:2:1006-1006 Asymmetries in Monetary Policy Reaction Function: Evidence for U.S. French and German Central Banks (2002). (4) RePEc:bep:sndecm:2:1997:1:15-22 Investigating Cyclical Asymmetries (1997). (5) RePEc:bep:sndecm:1:1996:1:35-46 A Check on the Robustness of Hamiltons Markov Switching Model Approach to the Economic Analysis of the Business Cycle (1996). (6) RePEc:bep:sndecm:6:2002:3:1090-1090 Wavelets in Economics and Finance: Past and Future (2002). (7) RePEc:bep:sndecm:3:1999:4:169-188 Stability Analysis of Continuous-Time Macroeconometric Systems (1999). (8) RePEc:bep:sndecm:2:1998:4:133-149 GARCH for Irregularly Spaced Financial Data: The ACD-GARCH Model (1998). (9) RePEc:bep:sndecm:3:1998:2:61-78 Smooth-Transition GARCH Models (1998). (10) RePEc:bep:sndecm:8:2004:3:1155-1155 Nonlinear Monetary Policy Rules: Some New Evidence for the U.S. (2004). (11) RePEc:bep:sndecm:1:1996:1:1-2 On Cycles and Chaos in Economics (1996). (12) RePEc:bep:sndecm:9:2005:1:1219-1219 A Practitioners Guide to Lag Order Selection For VAR Impulse Response Analysis (2005). (13) RePEc:bep:sndecm:5:2001:1:87-102 Wavelet Analysis of the Cost-of-Carry Model (2001). (14) RePEc:bep:sndecm:3:1998:3:119-140 Information-Theoretic Analysis of Serial Dependence and Cointegration (1998). (15) RePEc:bep:sndecm:7:2003:4:1125-1125 Nonlinearities and Cyclical Behavior: The Role of Chartists and Fundamentalists (2003). (16) RePEc:bep:sndecm:5:2001:3:1077-1077 Real Exchange Rate Dynamics in Transition Economies: A Nonlinear Analysis (2001). (17) RePEc:bep:sndecm:9:2005:1:1170-1170 Wavelet Transforms and Commodity Prices (2005). (18) RePEc:bep:sndecm:1:1996:1:47-64 Forecasting Using First-Available Versus Fully Revised Economic Time-Series Data (1996). (19) RePEc:bep:sndecm:1:1996:3:169-176 SIMANN: A Global Optimization Algorithm using Simulated Annealing (1996). (20) RePEc:bep:sndecm:2:1997:2:35-51 Finite Sample Properties of the Efficient Method of Moments (1997). (21) RePEc:bep:sndecm:5:2002:4:1083-1083 Microeconomic Models for Long Memory in the Volatility of Financial Time Series (2002). (22) RePEc:bep:sndecm:1:1997:4:175-185 Endogenous Cycles in Competitive Models: An Overview (1997). (23) RePEc:bep:sndecm:6:2002:1:1002-1002 Characterizing the Degree of Stability of Non-linear Dynamic Models (2002). (24) RePEc:bep:sndecm:3:1999:4:191-200 Sectoral Investigation of Asymmetries in the Conditional Mean Dynamics of the Real U.S. GDP (1999). (25) RePEc:bep:sndecm:8:2004:2:1223-1223 Mixture Processes for Financial Intradaily Durations (2004). (26) RePEc:bep:sndecm:8:2004:3:1182-1182 Household Income Dynamics in Two Transition Economies (2004). (27) RePEc:bep:sndecm:8:2004:1:1200-1200 An Investigation of Current Account Solvency in Latin America Using Non Linear Nonstationarity Tests (2004). (28) RePEc:bep:sndecm:6:2002:3:1091-1091 Power Properties of Nonlinearity Tests for Time Series with Markov Regimes (2002). (29) RePEc:bep:sndecm:7:2003:4:1183-1183 The Relationship Between Financial Variables and Real Economic Activity: Evidence From Spectral and Wavelet Analyses (2003). (30) RePEc:bep:sndecm:9:2005:4:1328-1328 The International CAPM and a Wavelet-Based Decomposition of Value at Risk (2005). (31) RePEc:bep:sndecm:7:2003:4:1112-1112 Credit Market Imperfections and Business Cycle Dynamics: A Nonlinear Approach (2003). (32) RePEc:bep:sndecm:5:2001:3:1078-1078 Evaluating the Persistence and Structuralist Theories of Unemployment from a Nonlinear Perspective (2001). (33) RePEc:bep:sndecm:3:1998:1:1-22 Avoiding the Pitfalls: Can Regime-Switching Tests Reliably Detect Bubbles? (1998). (34) RePEc:bep:sndecm:9:2005:4:1147-1147 Dual Long Memory in Inflation Dynamics across Countries of the Euro Area and the Link between Inflation Uncertainty and Macroeconomic Performance (2005). (35) RePEc:bep:sndecm:8:2004:2:1218-1218 Inference and Forecasting for ARFIMA Models With an Application to US and UK Inflation (2004). (36) RePEc:bep:sndecm:9:2005:2:1263-1263 Solving Ramsey Problems with Nonlinear Projection Methods (2005). (37) RePEc:bep:sndecm:8:2004:3:1226-1226 The Long Memory of the Efficient Market (2004). (38) RePEc:bep:sndecm:3:1999:4:223-237 Monetary Policy with a Nonlinear Phillips Curve and Asymmetric Loss (1999). (39) RePEc:bep:sndecm:8:2004:2:1210-1210 Estimating Stochastic Volatility Models: A Comparison of Two Importance Samplers (2004). (40) RePEc:bep:sndecm:2:1998:4:159-177 The Current Depth-of-Recession and Unemployment-Rate Forecasts (1998). (41) RePEc:bep:sndecm:7:2003:3:1119-1119 Industrial Sector Mode-Locking and Business Cycle Formation (2003). (42) RePEc:bep:sndecm:3:1998:3:141-156 Characterizing Asymmetries in Business Cycles Using Smooth-Transition Structural Time-Series Models (1998). (43) RePEc:bep:sndecm:6:2002:3:1092-1092 Common Persistent Factors in Inflation and Excess Nominal Money Growth and a New Measure of Core Inflation (2002). (44) RePEc:bep:sndecm:2:1998:4:1034-1034 Early News is Good News: The Effects of Market Opening on Market Volatility (1998). (45) RePEc:bep:sndecm:7:2003:1:1108-1108 Conditional and Unconditional Asymmetry in U.S. Macroeconomic Time Series (2003). (46) RePEc:bep:sndecm:10:2006:3:1362-1362 Point and Interval Forecasting of Spot Electricity Prices: Linear vs. Non-Linear Time Series Models (2006). (47) RePEc:bep:sndecm:4:2001:4:183-212 The Formation of Inflation Expectations under Changing Inflation Regimes (2001). (48) RePEc:bep:sndecm:3:1999:4:203-220 Should Policy Makers Worry about Asymmetries in the Business Cycle? (1999). (49) RePEc:bep:sndecm:1:1996:3:131-143 Detecting Asymmetries in Observed Linear Time Series and Unobserved Disturbances (1996). (50) RePEc:bep:sndecm:2:1997:2:23-34 Technical Trading Rules and the Size of the Risk Premium in Security Returns (1997). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 (1) RePEc:ces:ceswps:_1280 Inflation Targeting and Nonlinear Policy Rules: The Case of Asymmetric Preferences (2004). CESifo GmbH / CESifo Working Paper Series (2) RePEc:dgr:uvatin:20040016 Forecasting Daily Variability of the S&P 100 Stock Index using Historical, Realised and Implied Volatility Measurements (2004). Tinbergen Institute / Tinbergen Institute Discussion Papers (3) RePEc:ecm:ausm04:272 Duration and Order Type Clusters (2004). Econometric Society / Econometric Society 2004 Australasian Meetings (4) RePEc:ecm:feam04:730 Duration and Order Type Clusters (2004). Econometric Society / Econometric Society 2004 Far Eastern Meetings (5) RePEc:kls:series:0013 Asymmetric Dynamics in the Current Account: Evidence from Long-Horizon Data (2004). University of Cologne, Seminar of Economics / Working Paper Series in Economics (6) RePEc:pit:wpaper:322 Classical and Bayesian Analysis of Univariate and Multivariate Stochastic Volatility Models (2004). University of Pittsburgh, Department of Economics / Working Papers (7) RePEc:sce:scecf4:306 Aggregation of Dependent Risks with Specific Marginals by the Family of Koehler-Symanowski Distributions (2004). Society for Computational Economics / Computing in Economics and Finance 2004 (8) RePEc:ukc:ukcedp:0412 Current Account Sustainability in the US: What Do We Really Know About It? (2004). Department of Economics, University of Kent / Studies in Economics (9) RePEc:zbw:cauewp:2443 Classical and Bayesian Analysis of Univariate and Multivariate Stochastic Volatility Models (2004). Christian-Albrechts-University of Kiel, Department of Economics / Economics working papers Latest citations received in: 2003 (1) RePEc:ecb:ecbwps:20030283 US, Japan and the euro area - comparing business-cycle features. (2003). European Central Bank / Working Paper Series (2) RePEc:smu:ecowpa:0508 A Robust Entropy-Based Test for Asymmetry (2003). Southern Methodist University, Department of Economics / Departmental Working Papers Latest citations received in: 2002 (1) RePEc:man:cgbcrp:18 Nonlinearity in the Feds Monetary Policy Rule (2002). The School of Economic Studies, The Univeristy of Manchester / Centre for Growth and Business Cycle Research Discussion Paper Series Latest citations received in: 2001 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |