|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

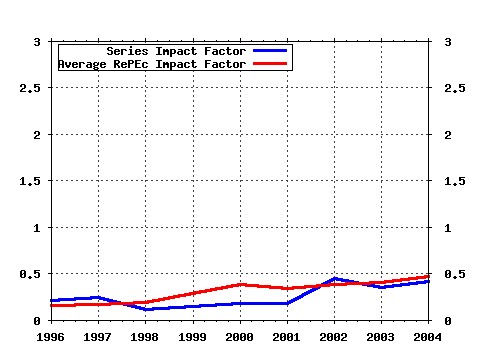

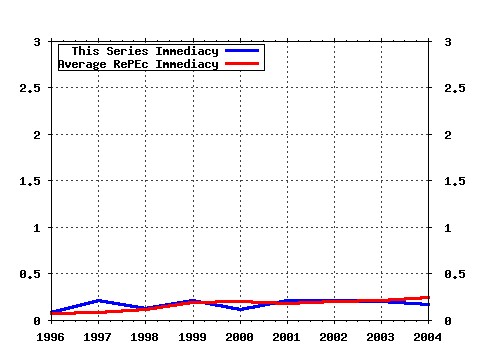

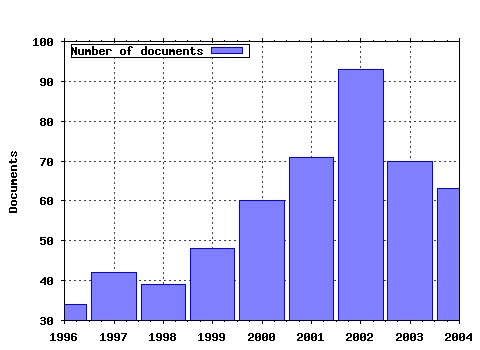

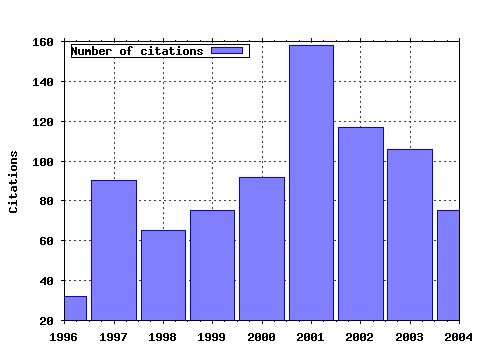

CIRANO / CIRANO Working Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:cir:cirwor:94s-23 High-Wage Workers and High-Wage Firms (1994). (2) RePEc:cir:cirwor:2000s-19 Rolling-Sample Volatility Estimators: Some New Theoretical, Simulation and Empirical Results (2000). (3) RePEc:cir:cirwor:98s-08 Job Characteristics and the Form of Compensation (1998). (4) RePEc:cir:cirwor:2001s-16 Marriage Market, Divorce Legislation and Household Labor Supply (2001). (5) RePEc:cir:cirwor:2001s-57 The Unreliability of Output Gap Estimates in Real Time (2001). (6) RePEc:cir:cirwor:97s-14 Methods of Pay and Earnings: A Longitudinal Analysis (1997). (7) RePEc:cir:cirwor:2002s-19 Unobserved Ability and the Return to Schooling (2002). (8) RePEc:cir:cirwor:2003s-01 The Reliability of Inflation Forecasts Based on Output Gap Estimates in Real Time (2003). (9) RePEc:cir:cirwor:2001s-70 An Eigenfunction Approach for Volatility Modeling (2001). (10) RePEc:cir:cirwor:95s-26 Industry-Specific Capital and the Wage Profile: Evidence from the NLSY and the PSID (1995). (11) RePEc:cir:cirwor:2003s-61 Short Run and Long Run Causality in Time Series: Inference (2003). (12) RePEc:cir:cirwor:97s-12 Equilibrium Asset Prices and No-Arbitrage with Portfolio Constraints (1997). (13) RePEc:cir:cirwor:96s-15 Markov Perfect Nash Equilibria in a Class of Resource Games (1996). (14) RePEc:cir:cirwor:2001s-42 Nonlinear Features of Realized FX Volatility (2001). (15) RePEc:cir:cirwor:2001s-46 Forecasting Some Low-Predictability Time Series Using Diffusion Indices (2001). (16) RePEc:cir:cirwor:2003s-17 Bootstrapping Autoregressions with Conditional Heteroskedasticity of Unknown Form (2003). (17) RePEc:cir:cirwor:2003s-49 Identification, Weak Instruments and Statistical Inference in Econometrics (2003). (18) RePEc:cir:cirwor:2002s-75 Trust and Reputation Building in E-Commerce (2002). (19) RePEc:cir:cirwor:95s-50 Environmental Protection, Producer Insolvency and Lender Liability (1995). (20) RePEc:cir:cirwor:2004s-19 Predicting Volatility: Getting the Most out of Return Data Sampled at Different Frequencies (2004). (21) RePEc:cir:cirwor:99s-24 Mobility and Cooperation: On the Run (1999). (22) RePEc:cir:cirwor:2001s-60 The Public-Private Sector Risk-Sharing in the French Insurance Cat. Nat. System (2001). (23) RePEc:cir:cirwor:2004s-20 The MIDAS Touch: Mixed Data Sampling Regression Models (2004). (24) RePEc:cir:cirwor:95s-31 Stochastic Volatility and Time Deformation: An Application to Trading Volume and Leverage Effects (1995). (25) RePEc:cir:cirwor:2002s-25 What Type Of Enterprise Forges Close Links With Universities And Government Labs? Evidence From CIS 2 (2002). (26) RePEc:cir:cirwor:95s-06 Are the Effects of Monetary Policy Asymmetric? (1995). (27) RePEc:cir:cirwor:2002s-90 Analytic Evaluation of Volatility Forecasts (2002). (28) RePEc:cir:cirwor:99s-08 Non-Traded Asset Valuation with Portfolio Constraints: A Binomial Approach (1999). (29) RePEc:cir:cirwor:94s-22 Environmental Risks and Bank Liability (1994). (30) RePEc:cir:cirwor:97s-34 Do Canadian Firms Respond to Fiscal Incentives to Research and Development? (1997). (31) RePEc:cir:cirwor:95s-32 Market Time and Asset Price Movements Theory and Estimation (1995). (32) RePEc:cir:cirwor:2000s-20 Towards an Innovation Intensity Index: The Case of CIS 1 in Denmark and Ireland (2000). (33) RePEc:cir:cirwor:2002s-58 Alternative Models for Stock Price Dynamics (2002). (34) RePEc:cir:cirwor:2000s-22 Temporal Aggregation of Volatility Models (2000). (35) RePEc:cir:cirwor:95s-16 On Stable Factor Structures in the Pricing of Risk (1995). (36) RePEc:cir:cirwor:2001s-19 The Bootstrap of the Mean for Dependent Heterogeneous Arrays (2001). (37) RePEc:cir:cirwor:99s-41 Travail pendant les études, performance scolaire et abandon (1999). (38) RePEc:cir:cirwor:2004s-04 The Econometrics of Option Pricing (2004). (39) RePEc:cir:cirwor:99s-48 A New Class of Stochastic Volatility Models with Jumps: Theory and Estimation (1999). (40) RePEc:cir:cirwor:95s-49 Stochastic Volatility (1995). (41) RePEc:cir:cirwor:97s-03 Competition and Access in Telecoms: ECPR, Global Price Cap, and Auctions (1997). (42) RePEc:cir:cirwor:99s-05 Seasonal Nonstationarity and Near-Nonstationarity (1999). (43) RePEc:cir:cirwor:2001s-25 Simulation-Based Finite-Sample Tests for Heteroskedasticity and ARCH Effects (2001). (44) RePEc:cir:cirwor:2001s-03 Testing and Comparing Value-at-Risk Measures (2001). (45) RePEc:cir:cirwor:95s-43 Empirical Martingale Simulation for Asset Prices (1995). (46) RePEc:cir:cirwor:2000s-35 Strategically Planned Behavior in Public Good Experiments (2000). (47) RePEc:cir:cirwor:99s-26 Stochastic Volatility: Univariate and Multivariate Extensions (1999). (48) RePEc:cir:cirwor:2004s-55 The Determinants of Credit Default Swap Premia (2004). (49) RePEc:cir:cirwor:94s-14 Disappointment Aversion as a Solution to the Equity Premium and the Risk-Free Rate Puzzles (1994). (50) RePEc:cir:cirwor:95s-42 Trading Patterns, Time Deformation and Stochastic Volatility in Foreign Exchange Markets (1995). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 (1) RePEc:cir:cirwor:2004s-14 Overcoming Natural Resource Constraints Through R&D (2004). CIRANO / CIRANO Working Papers (2) RePEc:cir:cirwor:2004s-19 Predicting Volatility: Getting the Most out of Return Data Sampled at Different Frequencies (2004). CIRANO / CIRANO Working Papers (3) RePEc:cir:cirwor:2004s-24 There is a Risk-Return Tradeoff After All (2004). CIRANO / CIRANO Working Papers (4) RePEc:cir:cirwor:2004s-26 Monitoring for Disruptions in Financial Markets (2004). CIRANO / CIRANO Working Papers (5) RePEc:ecb:ecbwps:20040366 The information content of over-the-counter currency options (2004). European Central Bank / Working Paper Series (6) RePEc:ecm:nasm04:585 Promotions, State Dependence and Intrafirm Job Mobility: Evidence From Personnel Records (2004). Econometric Society / Econometric Society 2004 North American Summer Meetings (7) RePEc:kof:wpskof:04-91 Bestimmungsfaktoren der Innovationstätigkeit und deren Einfluss auf Arbeitsproduktivität, Beschäftigung und Qualifikationsstruktur : Eine mikroökonometrische Untersuchung anhand von Paneldaten 198 (2004). Swiss Institute for Business Cycle Research (KOF), Swiss Federal Institute of Technology Zurich (ETH), / Working papers (8) RePEc:nbr:nberwo:10447 A Jackknife Estimator for Tracking Error Variance of Optimal Portfolios Constructed Using Estimated Inputs1 (2004). National Bureau of Economic Research, Inc / NBER Working Papers (9) RePEc:nbr:nberwo:10912 Jump and Volatility Risk and Risk Premia: A New Model and Lessons from S&P 500 Options (2004). National Bureau of Economic Research, Inc / NBER Working Papers (10) RePEc:rut:rutres:200424 Assessing Central Bank Credibility During the EMS Crises: Comparing Option and Spot Market-Based Forecasts (2004). Rutgers University, Department of Economics / Departmental Working Papers (11) RePEc:sbs:wpsefe:2004fe01 Econometrics of testing for jumps in financial economics using bipower variation (2004). Oxford Financial Research Centre / OFRC Working Papers Series Latest citations received in: 2003 (1) RePEc:cdl:anderf:1155 There is a Risk-Return Tradeoff After All (2003). Anderson Graduate School of Management, UCLA / University of California at Los Angeles, Anderson Graduate School of Management (2) RePEc:cir:cirwor:2003s-64 Directors and Officers Insurance and Shareholders Protection (2003). CIRANO / CIRANO Working Papers (3) RePEc:cla:levrem:506439000000000336 Market Research and Market Design (2003). UCLA Department of Economics / Levine's Bibliography (4) RePEc:cte:wsrepe:ws035212 GENERALIZED SPECTRAL TESTS FOR THE MARTINGALE DIFFERENCE HYPOTHESIS (2003). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (5) RePEc:fip:fedawp:2003-21 Inflation scares and forecast-based monetary policy (2003). Federal Reserve Bank of Atlanta / Working Paper (6) RePEc:fip:fedfap:2003-11 Inflation scares and forecast-based monetary policy (2003). Federal Reserve Bank of San Francisco / Working Papers in Applied Economic Theory (7) RePEc:fip:fedgfe:2003-32 Itô conditional moment generator and the estimation of short rate processes (2003). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (8) RePEc:fip:fedgfe:2003-36 Historical monetary policy analysis and the Taylor rule (2003). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (9) RePEc:fip:fedgfe:2003-41 Inflation scares and forecast-based monetary policy (2003). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (10) RePEc:fip:fedlwp:2003-025 Does idiosyncratic risk matter: another look (2003). Federal Reserve Bank of St. Louis / Working Papers (11) RePEc:ide:wpaper:1044 On the Asymptotic Efficiency of GMM (2003). Institut d'Économie Industrielle (IDEI), Toulouse / IDEI Working Papers (12) RePEc:lvl:lagrcr:0312 Are New Keynesian Phillips Curved Identified? (2003). (13) RePEc:yca:wpaper:2003_5 An Empirical Assessment of a Consumption CAPM with a Reference Level under Incomplete Consumption Insurance (2003). York University, Department of Economics / Working Papers (14) RePEc:zbw:bubdp1:4473 How wacky is the DAX? The changing structure of German stock market volatility (2003). Deutsche Bundesbank, Research Centre / Discussion Paper Series 1: Economic Studies Latest citations received in: 2002 (1) RePEc:cir:cirwor:2002s-16 Asymmetric Information And Product Differentiation (2002). CIRANO / CIRANO Working Papers (2) RePEc:cir:cirwor:2002s-76 Enforcing Contracts: Should Courts Seek the Truth? (2002). CIRANO / CIRANO Working Papers (3) RePEc:cir:cirwor:2002s-91 Correcting the Errors: A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). CIRANO / CIRANO Working Papers (4) RePEc:cir:cirwor:2002s-92 ARMA Representation of Two-Factor Models (2002). CIRANO / CIRANO Working Papers (5) RePEc:cir:cirwor:2002s-93 ARMA Representation of Integrated and Realized Variances (2002). CIRANO / CIRANO Working Papers (6) RePEc:cpr:ceprdp:3600 Earnings Dispersion, Risk Aversion and Education (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (7) RePEc:cpr:ceprdp:3601 A Structure Analysis of the Correlated Random Coefficient Wage Regression Model (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (8) RePEc:esi:discus:2002-46 Reputationsmechanismen auf Internet-Marktplattformen - Theorie und Empirie - (2002). Max Planck Institute of Economics, Strategic Interaction Group / Discussion Papers on Strategic Interaction (9) RePEc:hrr:papers:0204 Should Workers Care About Firm Size? (2002). Industrial Relations Center, University of Minnesota (Twin Cities Campus) / Working Papers (10) RePEc:ioe:doctra:222 Protección de la Competencia en Chile: El Estado y Laboratorios Chile y Recalcine (1992-93) (2002). Instituto de Economía. Pontificia Universidad Católica de Chile. / Documentos de Trabajo (11) RePEc:iza:izadps:dp508 Unobserved Ability and the Return to Schooling (2002). Institute for the Study of Labor (IZA) / IZA Discussion Papers (12) RePEc:iza:izadps:dp512 A Structural Analysis of the Correlated Random Coefficient Wage Regression Model (2002). Institute for the Study of Labor (IZA) / IZA Discussion Papers (13) RePEc:iza:izadps:dp513 Earnings Dispersion, Risk Aversion and Education (2002). Institute for the Study of Labor (IZA) / IZA Discussion Papers (14) RePEc:lec:leecon:02/14 Wage Growth, Human Capital and Risk Preference: Evidence From The British Household Panel Survey (2002). Department of Economics, University of Leicester / Discussion Papers in Economics (15) RePEc:mtl:montde:2002-21 Correcting the Errors : A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). Universite de Montreal, Departement de sciences economiques / Cahiers de recherche (16) RePEc:mtl:montec:21-2002 Correcting the Errors : A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). Centre interuniversitaire de recherche en économie quantitative, CIREQ / Cahiers de recherche (17) RePEc:nbr:nberwo:9056 On the Relationship Between the Conditional Mean and Volatility of Stock Returns: A Latent VAR Approach (2002). National Bureau of Economic Research, Inc / NBER Working Papers (18) RePEc:nbr:nberwo:9145 Using Heteroscedasticity to Estimate the Returns to Education (2002). National Bureau of Economic Research, Inc / NBER Working Papers (19) RePEc:nuf:econwp:0221 Measuring and forecasting financial variability using realised variance with and without a model (2002). Economics Group, Nuffield College, University of Oxford / Economics Papers (20) RePEc:shr:wpaper:02-07 Effects of government debt on interest rates: evidence from causality tests in johansen-type models (2002). Departement d'Economique de la Faculte d'administration à l'Universite de Sherbrooke / Cahiers de recherche Latest citations received in: 2001 (1) RePEc:bca:bocawp:01-18 Evaluating Factor Models: An Application to Forecasting Inflation in Canada (2001). Bank of Canada / Working Papers (2) RePEc:cir:cirwor:2001s-02 Empirical Assessment of an Intertemporal Option Pricing Model with Latent Variables (Note : New version February 2002) / Empirical Assessment of an Intertemporal Option Pricing Model with Latent Varia (2001). CIRANO / CIRANO Working Papers (3) RePEc:cir:cirwor:2001s-53 Environmental Regulation and Productivity: New Findings on the Porter Analysis (2001). CIRANO / CIRANO Working Papers (4) RePEc:cir:cirwor:2001s-61 Conditional Quantiles of Volatility in Equity Index and Foreign Exchange Data (2001). CIRANO / CIRANO Working Papers (5) RePEc:cir:cirwor:2001s-63 Dropout, School Performance and Working while in School : An Econometric Model with Heterogeneous Groups (2001). CIRANO / CIRANO Working Papers (6) RePEc:cir:cirwor:2001s-66 Incentives in Common Agency (2001). CIRANO / CIRANO Working Papers (7) RePEc:cir:cirwor:2001s-70 An Eigenfunction Approach for Volatility Modeling (2001). CIRANO / CIRANO Working Papers (8) RePEc:cir:cirwor:2001s-71 A Theoretical Comparison Between Integrated andRealized Volatilities / A Theoretical Comparison Between Integrated and Realized Volatilities (2001). CIRANO / CIRANO Working Papers (9) RePEc:cre:crefwp:140 Collective Household Labor Supply: Nonparticipation and Income Taxation (2001). CREFE, Université du Québec à Montréal / Cahiers de recherche CREFE / CREFE Working Papers (10) RePEc:cre:crefwp:141 Collective Female Labor Supply: Theory and Application (2001). CREFE, Université du Québec à Montréal / Cahiers de recherche CREFE / CREFE Working Papers (11) RePEc:iza:izadps:dp341 Testing for Asymmetry in British, German and US Unemployment Data (2001). Institute for the Study of Labor (IZA) / IZA Discussion Papers (12) RePEc:iza:izadps:dp368 How Do Sex Ratios Affect Marriage and Labor Markets? Evidence from Americas Second Generation (2001). Institute for the Study of Labor (IZA) / IZA Discussion Papers (13) RePEc:nuf:econwp:0104 Econometric analysis of realised volatility and its use in estimating stochastic volatility models (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (14) RePEc:nuf:econwp:0118 Realised power variation and stochastic volatility models (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (15) RePEc:oxf:wpaper:071 Econometric Analysis of Realised Volatility and Its Use in Estimating Stochastic Volatility Models (2001). University of Oxford, Department of Economics / Economics Series Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |