|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

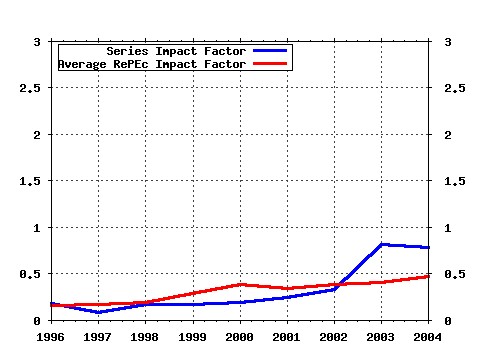

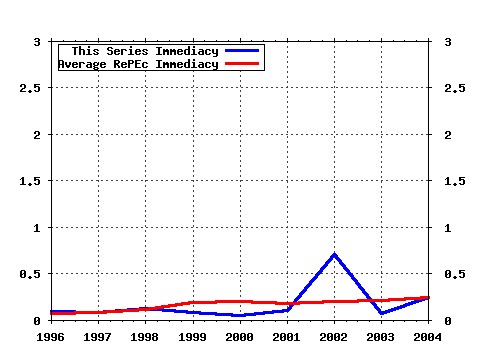

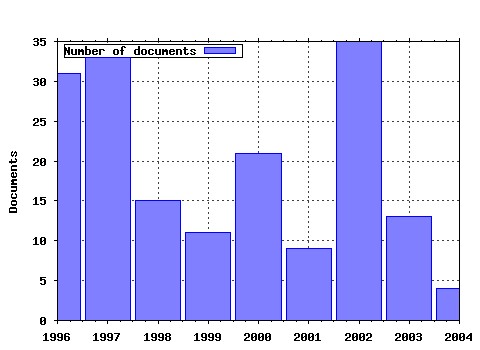

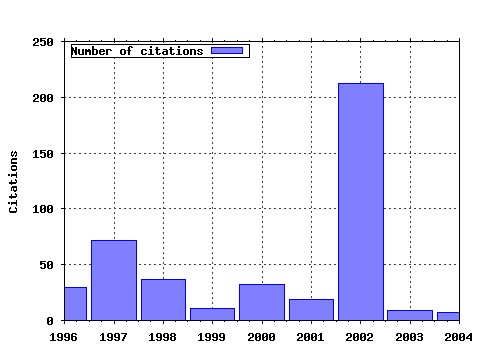

Duke University, Department of Economics / Working Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:duk:dukeec:02-16 Micro Effects of Macro Announcements: Real-Time Price Discovery in Foreign Exchange (2002). (2) RePEc:duk:dukeec:02-03 Alternative Models for Stock Price Dynamic (2002). (3) RePEc:duk:dukeec:95-36 Estimation of Stochastic Volatility Models with Diagnostics (1995). (4) RePEc:duk:dukeec:97-09 Reprojecting Partially Observed Systems with Application to Interest Rate Diffusions (1997). (5) RePEc:duk:dukeec:02-12 Modeling and Forecasting Realized Volatility (2002). (6) RePEc:duk:dukeec:95-37 Aggregate Population and Economic Growth Correlations: The Role of the Components of Demographic Change (1995). (7) RePEc:duk:dukeec:96-17 Qualitative and Asymptotic Performance of SNP Density Estimators (1996). (8) RePEc:duk:dukeec:98-02 Empirical Puzzles of Chilean Stabilization Policy (1998). (9) RePEc:duk:dukeec:02-06 Efficient Method of Moments (2002). (10) RePEc:duk:dukeec:95-20 Which Moments to Match (1995). (11) RePEc:duk:dukeec:95-42 New Minimum Chi-Square Methods in Empirical Finance (1995). (12) RePEc:duk:dukeec:97-30 The Syndrome of Exchange-Rate-Based Stabilizations and the Uncertain Duration of Currency Pegs (1997). (13) RePEc:duk:dukeec:97-02 Rural-Urban Disparity and Sectoral Labor Allocation in China (1997). (14) RePEc:duk:dukeec:02-13 Introducing School Choice into Multi-District Public School Systems (2002). (15) RePEc:duk:dukeec:97-19 The Economics of Giving (1997). (16) RePEc:duk:dukeec:97-26 Rational Herd Behavior and the Globalization of Securities Markets (1997). (17) RePEc:duk:dukeec:98-12 Public School Segregation in Metropolitan Areas (1998). (18) RePEc:duk:dukeec:95-26 SNP: A Program for Nonparametric Time Series Analysis. Version 8.4. Users Guide (1995). (19) RePEc:duk:dukeec:00-19 Oligopoly Banking and Capital Accumulation (2000). (20) RePEc:duk:dukeec:00-02 Peer Effects, Financial Aid, and Selection of Students into Colleges and Universities: An Empirical Analysis (2000). (21) RePEc:duk:dukeec:95-09 Education and Off-Farm Work (1995). (22) RePEc:duk:dukeec:02-08 Confidence Intervals for Half-life Deviations from Purchasing Power Parity (2002). (23) RePEc:duk:dukeec:02-17 School Finance, Spatial Income Segregation and the Nature of Communities (2002). (24) RePEc:duk:dukeec:01-07 Factor Taxation with Heterogeneous Agents (2001). (25) RePEc:duk:dukeec:01-03 Fiscal Policy with Heterogeneous Agents and Incomplete Markets (2001). (26) RePEc:duk:dukeec:95-05 Temporal Reliability of Estimates from Contingent Valuation (1995). (27) RePEc:duk:dukeec:95-02 Volume, Volatility and Leverage: A Dynamic Analysis (1995). (28) RePEc:duk:dukeec:01-05 Financial Globalization and Real Regionalization (2001). (29) RePEc:duk:dukeec:02-18 The Impact of Jumps in Volatility and Returns (2002). (30) RePEc:duk:dukeec:00-01 On the Benefits of Dollarization when Stabilization Policy Is Not Credible and Financial Markets are Imperfect (2000). (31) RePEc:duk:dukeec:96-02 Nonparametric Estimation of a Survivor Function with Across-Interval-Censored Data (1996). (32) RePEc:duk:dukeec:95-17 Referendum Design and Contingent Valuation: TheNOAA Panels No-Vote Recommendation (1995). (33) RePEc:duk:dukeec:99-08 North-South Technological Diffusion: A New Case for Dynamic Gains from Trade (1999). (34) RePEc:duk:dukeec:02-09 Simulated Score Methods and Indirect Inference for Continuous-time Models (2002). (35) RePEc:duk:dukeec:04-05 Efficient Allocations with Moral Hazard and Hidden Borrowing and Lending (2004). (36) RePEc:duk:dukeec:07-04 Information Criteria for Impulse Response Function Matching Estimation of DSGE Models (2007). (37) RePEc:duk:dukeec:05-11 Public Information and Electoral Bias (2005). (38) RePEc:duk:dukeec:95-21 A Mixture Model of Willingness to Pay Distributions (1995). (39) RePEc:duk:dukeec:06-04 Asymptotic Properties for a Class of Partially Identified Models (2006). (40) RePEc:duk:dukeec:97-17 Procedural cum Endstate Justice: An Implementation Viewpoint (1997). (41) RePEc:duk:dukeec:98-03 Priority Rules and Other Inequitable Rationing Methods (1998). (42) RePEc:duk:dukeec:98-10 Approximate Distributions in Essentially Linear Models (1998). (43) RePEc:duk:dukeec:03-10 Privacy in Competitive Markets (2003). (44) RePEc:duk:dukeec:96-31 Strategyproof Sharing of Submodular Access Costs: Budget Balance versus Efficiency (1996). (45) RePEc:duk:dukeec:95-56 Education in Production: Measuring Labor Quality and Management (1995). (46) RePEc:duk:dukeec:02-05 Optimal Tests for Nested Model Selection with Underlying Parameter Instability (2002). (47) RePEc:duk:dukeec:95-55 Econometric Analysis of Sequential Discrete Choice Models (1995). (48) RePEc:duk:dukeec:96-21 Was the NOAA Panel Correct about Contingent Valuation? (1996). (49) RePEc:duk:dukeec:95-46 The Supply of Childrens Time to Disabled Elderly Parents (1995). (50) RePEc:duk:dukeec:03-23 Do Technology Shocks Drive Hours Up or Down? A Little Evidence from an Agnostic Procedure (2003). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 (1) RePEc:cla:levrem:122247000000000050 On the Recursive Saddle Point Method (2004). UCLA Department of Economics / Levine's Bibliography Latest citations received in: 2003 (1) RePEc:emo:wp2003:0326 Do Technology Shocks Drive Hours Up or Down? A Little Evidence From an Agnostic Procedure (2003). Department of Economics, Emory University (Atlanta) / Emory Economics Latest citations received in: 2002 (1) RePEc:cir:cirwor:2002s-02 Financial Asset Returns, Market Timing, and Volatility Dynamics (2002). CIRANO / CIRANO Working Papers (2) RePEc:cir:cirwor:2002s-03 Macro Surprises And Short-Term Behaviour In Bond Futures (2002). CIRANO / CIRANO Working Papers (3) RePEc:cir:cirwor:2002s-58 Alternative Models for Stock Price Dynamics (2002). CIRANO / CIRANO Working Papers (4) RePEc:cir:cirwor:2002s-63 Testing Normality: A GMM Approach (2002). CIRANO / CIRANO Working Papers (5) RePEc:cir:cirwor:2002s-90 Analytic Evaluation of Volatility Forecasts (2002). CIRANO / CIRANO Working Papers (6) RePEc:cir:cirwor:2002s-92 ARMA Representation of Two-Factor Models (2002). CIRANO / CIRANO Working Papers (7) RePEc:cir:cirwor:2002s-93 ARMA Representation of Integrated and Realized Variances (2002). CIRANO / CIRANO Working Papers (8) RePEc:ecb:ecbwps:20020194 Sensitivity analysis of volatility - a new tool for risk management. (2002). European Central Bank / Working Paper Series (9) RePEc:ecb:ecbwps:20020200 Interdependence between the euro area and the US: what role for EMU? (2002). European Central Bank / Working Paper Series (10) RePEc:fip:fedfap:2002-13 Statistical nonlinearities in the business cycle: a challenge for the canonical RBC model (2002). Federal Reserve Bank of San Francisco / Working Papers in Applied Economic Theory (11) RePEc:fip:fedfap:2002-15 The impact of financial frictions on a small open economy: when current account borrowing hits a limit (2002). Federal Reserve Bank of San Francisco / Working Papers in Applied Economic Theory (12) RePEc:fip:fedgfe:2002-45 Insolvency or liquidity squeeze? Explaining very short-term corporate yield spreads (2002). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (13) RePEc:fip:fedkrw:rwp02-05 Forecast-based model selection in the presence of structural breaks (2002). Federal Reserve Bank of Kansas City / Research Working Paper (14) RePEc:ide:wpaper:1037 Efficient Estimation of Jump Diffusions and General Dynamic Models with a Continuum of Moment Conditions (2002). Institut d'Économie Industrielle (IDEI), Toulouse / IDEI Working Papers (15) RePEc:jae:japmet:v:17:y:2002:i:5:p:457-477 Estimating quadratic variation using realized variance (2002). Journal of Applied Econometrics (16) RePEc:msh:ebswps:2002-17 A Class of Nonlinear Stochastic Volatility Models and Its Implications on Pricing Currency Options (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (17) RePEc:msh:ebswps:2002-19 Influence Diagnostics in GARCH Processes (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (18) RePEc:msh:ebswps:2002-2 Bayesian Estimation of a Stochastic Volatility Model Using Option and Spot Prices. (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (19) RePEc:mtl:montde:2002-14 Testing Normality : A GMM Approach (2002). Universite de Montreal, Departement de sciences economiques / Cahiers de recherche (20) RePEc:nbr:nberwo:9056 On the Relationship Between the Conditional Mean and Volatility of Stock Returns: A Latent VAR Approach (2002). National Bureau of Economic Research, Inc / NBER Working Papers (21) RePEc:nuf:econwp:0213 Econometric Analysis of Realised Covariation: High Frequency Covariance, Regression and Correlation in Financial Economics (2002). Economics Group, Nuffield College, University of Oxford / Economics Papers (22) RePEc:nuf:econwp:0221 Measuring and forecasting financial variability using realised variance with and without a model (2002). Economics Group, Nuffield College, University of Oxford / Economics Papers (23) RePEc:sbs:wpsefe:2002fe03 Econometric analysis of realised covariation: high frequency covariance, regression and correlation in financial economics (2002). Oxford Financial Research Centre / OFRC Working Papers Series (24) RePEc:taf:jpolrf:v:5:y:2002:i:3:p:127-131 Is Talk Cheap? (2002). Journal of Policy Reform (25) RePEc:wop:pennin:02-27 Parametric and Nonparametric Volatility Measurement (2002). Wharton School Center for Financial Institutions, University of Pennsylvania / Center for Financial Institutions Working Papers Latest citations received in: 2001 (1) RePEc:red:issued:v:4:y:2001:i:2:p:406-437 Idiosyncratic Risk in the United States and Sweden: Is There a Role for Government Insurance? (2001). Review of Economic Dynamics Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |