|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

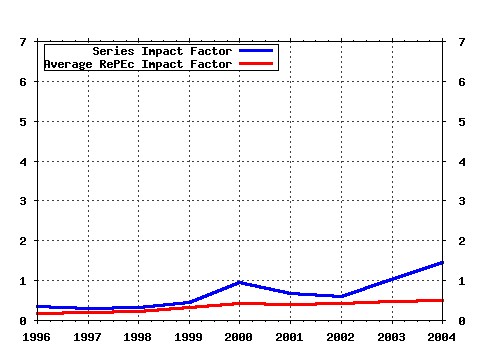

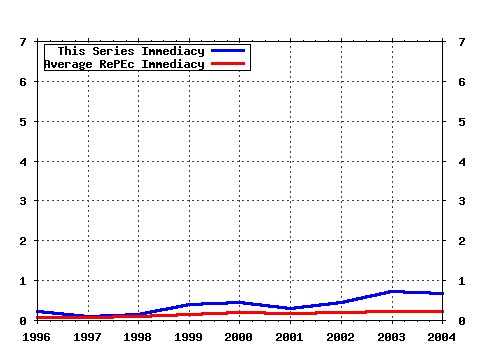

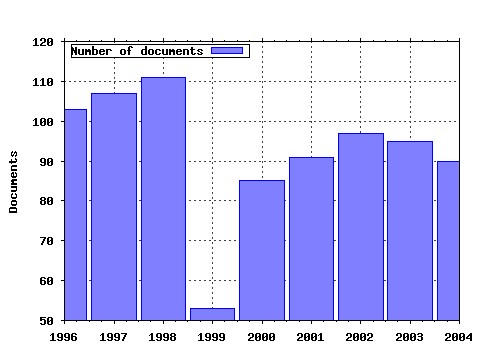

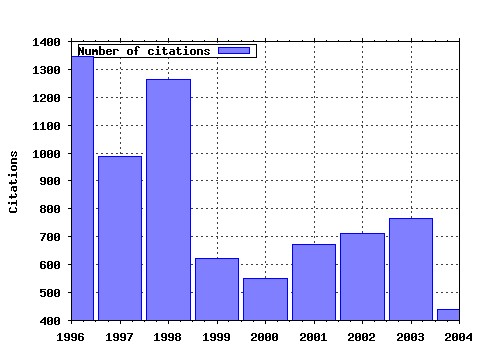

Journal of Econometrics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:econom:v:31:y:1986:i:3:p:307-327 Generalized autoregressive conditional heteroskedasticity (1986). (2) RePEc:eee:econom:v:87:y:1998:i:1:p:115-143 Initial conditions and moment restrictions in dynamic panel data models (1998). (3) RePEc:eee:econom:v:6:y:1977:i:1:p:21-37 Formulation and estimation of stochastic frontier production function models (1977). (4) RePEc:eee:econom:v:2:y:1974:i:2:p:111-120 Spurious regressions in econometrics (1974). (5) RePEc:eee:econom:v:54:y:1992:i:1-3:p:159-178 Testing the null hypothesis of stationarity against the alternative of a unit root : How sure are we that economic time series have a unit root? (1992). (6) RePEc:eee:econom:v:115:y:2003:i:1:p:53-74 Testing for unit roots in heterogeneous panels (2003). (7) RePEc:eee:econom:v:32:y:1986:i:3:p:385-397 Random group effects and the precision of regression estimates (1986). (8) RePEc:eee:econom:v:52:y:1992:i:1-2:p:5-59 ARCH modeling in finance : A review of the theory and empirical evidence (1992). (9) RePEc:eee:econom:v:68:y:1995:i:1:p:29-51 Another look at the instrumental variable estimation of error-components models (1995). (10) RePEc:eee:econom:v:68:y:1995:i:1:p:79-113 Estimating long-run relationships from dynamic heterogeneous panels (1995). (11) RePEc:eee:econom:v:18:y:1982:i:1:p:47-82 Formulation and estimation of dynamic models using panel data (1982). (12) RePEc:eee:econom:v:31:y:1986:i:1:p:93-118 Errors in variables in panel data (1986). (13) RePEc:eee:econom:v:108:y:2002:i:1:p:1-24 Unit root tests in panel data: asymptotic and finite-sample properties (2002). (14) RePEc:eee:econom:v:4:y:1976:i:2:p:115-145 Exact and superlative index numbers (1976). (15) RePEc:eee:econom:v:16:y:1981:i:1:p:155-155 Panel data and unobservable individual effects (1981). (16) RePEc:eee:econom:v:74:y:1996:i:1:p:119-147 Impulse response analysis in nonlinear multivariate models (1996). (17) RePEc:eee:econom:v:30:y:1985:i:1-2:p:239-267 Alternative methods for evaluating the impact of interventions : An overview (1985). (18) RePEc:eee:econom:v:80:y:1997:i:2:p:355-385 Further evidence on breaking trend functions in macroeconomic variables (1997). (19) RePEc:eee:econom:v:61:y:1994:i:1:p:5-21 On discrimination and the decomposition of wage differentials (1994). (20) RePEc:eee:econom:v:33:y:1986:i:3:p:311-340 Understanding spurious regressions in econometrics (1986). (21) RePEc:eee:econom:v:44:y:1990:i:1-2:p:215-238 Seasonal integration and cointegration (1990). (22) RePEc:eee:econom:v:18:y:1982:i:1:p:83-114 The use of time series processes to model the error structure of earnings in a longitudinal data analysis (1982). (23) RePEc:eee:econom:v:73:y:1996:i:1:p:5-59 Long memory processes and fractional integration in econometrics (1996). (24) RePEc:eee:econom:v:19:y:1982:i:2-3:p:233-238 On the estimation of technical inefficiency in the stochastic frontier production function model (1982). (25) RePEc:eee:econom:v:14:y:1980:i:2:p:227-238 Long memory relationships and the aggregation of dynamic models (1980). (26) RePEc:eee:econom:v:45:y:1990:i:1-2:p:39-70 Analysis of time series subject to changes in regime (1990). (27) RePEc:eee:econom:v:53:y:1992:i:1-3:p:211-244 Testing structural hypotheses in a multivariate cointegration analysis of the PPP and the UIP for UK (1992). (28) RePEc:eee:econom:v:60:y:1994:i:1-2:p:203-233 Five alternative methods of estimating long-run equilibrium relationships (1994). (29) RePEc:eee:econom:v:16:y:1981:i:1:p:121-130 Some properties of time series data and their use in econometric model specification (1981). (30) RePEc:eee:econom:v:39:y:1988:i:3:p:347-366 Limited information estimators and exogeneity tests for simultaneous probit models (1988). (31) RePEc:eee:econom:v:39:y:1988:i:1-2:p:199-211 Some recent development in a concept of causality (1988). (32) RePEc:eee:econom:v:74:y:1996:i:1:p:3-30 Fractionally integrated generalized autoregressive conditional heteroskedasticity (1996). (33) RePEc:eee:econom:v:64:y:1994:i:1-2:p:307-333 Autoregressive conditional heteroskedasticity and changes in regime (1994). (34) RePEc:eee:econom:v:31:y:1986:i:3:p:255-274 The frequency of price adjustment : A study of the newsstand prices of magazines (1986). (35) RePEc:eee:econom:v:74:y:1996:i:1:p:59-75 Testing the adequacy of smooth transition autoregressive models (1996). (36) RePEc:eee:econom:v:90:y:1999:i:1:p:1-44 Spurious regression and residual-based tests for cointegration in panel data (1999). (37) RePEc:eee:econom:v:53:y:1992:i:1-3:p:165-188 Maximum likelihood estimation of stationary univariate fractionally integrated time series models (1992). (38) RePEc:eee:econom:v:70:y:1996:i:1:p:99-126 Residual-based tests for cointegration in models with regime shifts (1996). (39) RePEc:eee:econom:v:68:y:1995:i:1:p:5-27 Efficient estimation of models for dynamic panel data (1995). (40) RePEc:eee:econom:v:30:y:1985:i:1-2:p:109-126 Panel data from time series of cross-sections (1985). (41) RePEc:eee:econom:v:71:y:1996:i:1-2:p:161-173 Interpreting tests of the convergence hypothesis (1996). (42) RePEc:eee:econom:v:45:y:1990:i:1-2:p:267-290 Alternative models for conditional stock volatility (1990). (43) RePEc:eee:econom:v:18:y:1982:i:1:p:115-168 New methods for analyzing structural models of labor force dynamics (1982). (44) RePEc:eee:econom:v:66:y:1995:i:1-2:p:225-250 Statistical inference in vector autoregressions with possibly integrated processes (1995). (45) RePEc:eee:econom:v:52:y:1992:i:3:p:389-402 Cointegration in partial systems and the efficiency of single-equation analysis (1992). (46) RePEc:eee:econom:v:38:y:1988:i:3:p:387-399 Prediction of firm-level technical efficiencies with a generalized frontier production function and panel data (1988). (47) RePEc:eee:econom:v:68:y:1995:i:1:p:53-78 On bias, inconsistency, and efficiency of various estimators in dynamic panel data models (1995). (48) RePEc:eee:econom:v:105:y:2001:i:1:p:85-110 Tests of equal forecast accuracy and encompassing for nested models (2001). (49) RePEc:eee:econom:v:29:y:1985:i:3:p:229-256 Generalized method of moments specification testing (1985). (50) RePEc:eee:econom:v:60:y:1994:i:1-2:p:1-22 Dynamic linear models with Markov-switching (1994). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 (1) RePEc:aea:aecrev:v:94:y:2004:i:3:p:656-690 Workers Education, Spillovers, and Productivity: Evidence from Plant-Level Production Functions (2004). American Economic Review (2) RePEc:bbk:bbkefp:0403 Unobserved Heterogeneity in Panel Time Series Models (2004). Birkbeck, School of Economics, Mathematics & Statistics / Birkbeck Working Papers in Economics and Finance (3) RePEc:bcl:bclwop:cahier_etude_12 INFLATION PERSISTENCE IN LUXEMBOURG A COMPARISON WITH EU15 COUNTRIES AT THE DISAGGREGATE LEVEL (2004). Central Bank of Luxembourg / BCL working papers (4) RePEc:bon:bonedp:bgse1_2005 Price Convergence across Regions in India (2004). University of Bonn, Germany / Bonn Econ Discussion Papers (5) RePEc:cam:camdae:0434 âRandom Coefficient Panel Data Modelsâ (2004). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (6) RePEc:cam:camdae:0441 Cost of Capital and Regulatorâs Preferences: Investigation into a new method of estimating regulatory bias (2004). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (7) RePEc:cdl:agrebk:971 Forecasting Chinas Carbon Dioxide Emissions: A Provincial Approach (2004). Department of Agricultural & Resource Economics, UC Berkeley / Department of Agricultural & Resource Economics, UC Berkeley, Working Paper Series (8) RePEc:cdl:ucsdec:2004-08 Optimal Power for Testing Potential Cointegrating Vectors with Known (2004). Department of Economics, UC San Diego / University of California at San Diego, Economics Working Paper Series (9) RePEc:ces:ceswps:_1233 Random Coefficient Panel Data Models (2004). CESifo GmbH / CESifo Working Paper Series (10) RePEc:ces:ceswps:_1335 Why Does Educational Attainment Differ Across U.S. States? (2004). CESifo GmbH / CESifo Working Paper Series (11) RePEc:cir:cirwor:2004s-26 Monitoring for Disruptions in Financial Markets (2004). CIRANO / CIRANO Working Papers (12) RePEc:cir:cirwor:2004s-37 Conditionally Heteroskedastic Factor Models: Identification and Instrumental Variables Estimation (2004). CIRANO / CIRANO Working Papers (13) RePEc:cmf:wpaper:wp2004_0409 INDIRECT ESTIMATION OF CONDITIONALLY HETEROSKEDASTIC FACTOR MODELS (2004). CEMFI / Working Papers (14) RePEc:cty:dpaper:0408 Robust inference on seasonal unit roots via a bootstrap applied to OECD macroeconomic series (2004). Department of Economics, City University, London / City University Economics Discussion Papers (15) RePEc:dgr:umamet:2004040 Panel Unit Root Tests in the Presence of Cross-Sectional Dependencies: Comparison and Implications for Modelling (2004). Maastricht : METEOR, Maastricht Research School of Economics of Technology and Organization / Research Memoranda (16) RePEc:ebl:ecbull:v:3:y:2004:i:24:p:1-11 Detecting changes in persistence in linear time series (2004). Economics Bulletin (17) RePEc:ebl:ecbull:v:3:y:2004:i:39:p:1-10 Some New Tests for a Change in Persistence (2004). Economics Bulletin (18) RePEc:ecb:ecbwps:20040415 How persistent is disaggregate inflation? An analysis across EU15 countries and HICP sub-indices (2004). European Central Bank / Working Paper Series (19) RePEc:ecm:ausm04:124 International linkage of real interest rates: the case of East Asian countries (2004). Econometric Society / Econometric Society 2004 Australasian Meetings (20) RePEc:ecm:ausm04:313 Testing for Dependence in Non-Gaussian Time Series Data (2004). Econometric Society / Econometric Society 2004 Australasian Meetings (21) RePEc:ecm:ausm04:348 Testing for Nonlinearity in Mean in the Presence of Heteroskedasticity (2004). Econometric Society / Econometric Society 2004 Australasian Meetings (22) RePEc:ecm:ausm04:64 Modified Tests for a Change in Persistence (2004). Econometric Society / Econometric Society 2004 Australasian Meetings (23) RePEc:ecm:nasm04:161 Finite Sample and Optimal Inference in Possibly Nonstationary ARCH Models with Gaussian and Heavy-Tailed Errors (2004). Econometric Society / Econometric Society 2004 North American Summer Meetings (24) RePEc:egc:wpaper:892 Schooling Returns for Wage Earners in Burkina Faso: Evidence from the 1994 and 1998 National Surveys (2004). Economic Growth Center, Yale University / Working Papers (25) RePEc:ema:worpap:2004-13 Conditionaly Heteroskedastic Factor Models : Identificationand Instrumental variables Estmation (2004). THEMA / Working papers (26) RePEc:eui:euiwps:eco2004/29 Efficient Tests of the Seasonal Unit Root Hypothesis (2004). European University Institute / Economics Working Papers (27) RePEc:eui:euiwps:eco2004/31 Properties of Recursive Trend-Adjusted Unit Root Tests (2004). European University Institute / Economics Working Papers (28) RePEc:fip:fedgfe:2004-03 Measuring the effects of monetary policy: a factor-augmented vector autoregressive (FAVAR) approach (2004). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (29) RePEc:fip:fedkrw:rwp04-10 Improving forecast accuracy by combining recursive and rolling forecasts (2004). Federal Reserve Bank of Kansas City / Research Working Paper (30) RePEc:fip:fedlwp:2003-045 A common model approach to macroeconomics: using panel data to reduce sampling error (2004). Federal Reserve Bank of St. Louis / Working Papers (31) RePEc:fip:fedlwp:2004-005 The information content of regional employment data for forecasting aggregate conditions (2004). Federal Reserve Bank of St. Louis / Working Papers (32) RePEc:hhs:ifauwp:2005_003 Labor market discrimination and racial differences in premarket factors (2004). IFAU - Institute for Labour Market Policy Evaluation / Working Paper Series (33) RePEc:hhs:lunewp:2004_017 Testing for Stationarity in Panel Data Models when Disturbances are Cross-Sectionally Correlated (2004). Lund University, Department of Economics / Working Papers (34) RePEc:hhs:osloec:2004_022 Can Random Coefficient Cobb-Douglas Production Functions Be Aggregated to Similar Macro Functions? (2004). Oslo University, Department of Economics / Memorandum (35) RePEc:iza:izadps:dp1236 Random Coefficient Panel Data Models (2004). Institute for the Study of Labor (IZA) / IZA Discussion Papers (36) RePEc:iza:izadps:dp1382 Firm-Level Social Returns to Education (2004). Institute for the Study of Labor (IZA) / IZA Discussion Papers (37) RePEc:jae:japmet:v:19:y:2004:i:4:p:505-524 Nonparametric analysis of returns to scale in the US hospital industry (2004). Journal of Applied Econometrics (38) RePEc:jae:japmet:v:19:y:2004:i:4:p:533-535 Predictor relevance and extramarital affairs (2004). Journal of Applied Econometrics (39) RePEc:lec:leecon:04/27 Bayesian Approaches to Cointegration (2004). Department of Economics, University of Leicester / Discussion Papers in Economics (40) RePEc:lec:leecon:04/31 Forecasting and Estimating Multiple Change-point Models with an Unknown Number of Change-points (2004). Department of Economics, University of Leicester / Discussion Papers in Economics (41) RePEc:may:mayecw:n1370804 EARNINGS RISK AND DEMAND FOR HIGHER EDUCATION: A CROSS-SECTION TEST FOR SPAIN (2004). Department of Economics, National University of Ireland - Maynooth / Economics Department Working Paper Series (42) RePEc:met:wpaper:0417 Gender Differences in Academic Performance in a Large Public University in Turkey (2004). ERC - Economic Research Center, Middle East Technical University / Working Papers (43) RePEc:msh:ebswps:2004-13 Testing for Dependence in Non-Gaussian Time Series Data (2004). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (44) RePEc:msh:ebswps:2004-26 Box-Cox Stochastic Volatility Models with Heavy-Tails and Correlated Errors (2004). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (45) RePEc:nbr:nberwo:10220 Measuring the Effects of Monetary Policy: A Factor-Augmented Vector Autoregressive (FAVAR) Approach (2004). National Bureau of Economic Research, Inc / NBER Working Papers (46) RePEc:nbr:nberwo:10366 Would the Elimination of Affirmative Action Affect Highly Qualified Minority Applicants? Evidence from California and Texas (2004). National Bureau of Economic Research, Inc / NBER Working Papers (47) RePEc:nbr:nberwo:10666 Good Principals or Good Peers? Parental Valuation of School Characteristics, Tiebout Equilibrium, and the Effects of Inter-district Competition (2004). National Bureau of Economic Research, Inc / NBER Working Papers (48) RePEc:nbr:nberwo:10809 The Effect of College Curriculum on Earnings: Accounting for Non-Ignorable Non-Response Bias (2004). National Bureau of Economic Research, Inc / NBER Working Papers (49) RePEc:nbr:nberwo:10811 Testing a Roy Model with Productivity Spillovers: Evidence from the Treatment of Heart Attacks (2004). National Bureau of Economic Research, Inc / NBER Working Papers (50) RePEc:rut:rutres:200415 A Likelihood-Based Evaluation of the Segmented Markets Friction in Equilibrium Monetary Models (2004). Rutgers University, Department of Economics / Departmental Working Papers (51) RePEc:rut:rutres:200418 Bootstrap Procedures for Recursive Estimation Schemes With Applications to Forecast Model Selection (2004). Rutgers University, Department of Economics / Departmental Working Papers (52) RePEc:san:crieff:0404 Firm-Level Social Returns to Education (2004). Centre for Research into Industry, Enterprise, Finance and the Firm / CRIEFF Discussion Papers (53) RePEc:scp:wpaper:04-5 Reducing Bias of MLE in a Dynamic Panel Model (2004). Institute of Economic Policy Research (IEPR) / IEPR Working Papers (54) RePEc:ube:dpvwib:dp0418 The Carbon Kuznets Curve: A Cloudy Picture Emitted by Bad Econometrics? (2004). Universitat Bern, Volkswirtschaftliches Institut / Diskussionsschriften (55) RePEc:ubs:wpaper:ubs0408 The Dynamics of Firms Entry and Diversification: A Bayesian Panel Probit Approach. A Cross-country analysis (2004). University of Brescia, Department of Economics / Working Papers (56) RePEc:upf:upfgen:925 The transmission of US shocks to Latin America (2004). Department of Economics and Business, Universitat Pompeu Fabra / Economics Working Papers (57) RePEc:upj:weupjo:04-106 Increasing the Economic Development Benefits of Higher Education in Michigan (2004). W.E. Upjohn Institute for Employment Research / Staff Working Papers (58) RePEc:wpa:wuwpdc:0409063 Monetary Union in West Africa and Asymmetric Shocks: A Dynamic Structural Factor Model Approach (2004). EconWPA / Development and Comp Systems (59) RePEc:wpa:wuwpem:0409005 Bias Reduction by Recursive Mean Adjustment in Dynamic Panel Data Models (2004). EconWPA / Econometrics (60) RePEc:wrk:warwec:694 Sensitivity of the Chi-Squared Goodness-of-Fit Test to the Partitioning of Data (2004). University of Warwick, Department of Economics / The Warwick Economics Research Paper Series (TWERPS) (61) RePEc:zbw:cauewp:2442 The Markov-Switching Multi-Fractal Model of Asset Returns : GMM Estimation and Linear Forecasting of Volatility (2004). Christian-Albrechts-University of Kiel, Department of Economics / Economics working papers Latest citations received in: 2003 (1) RePEc:bon:bonedp:bgse27_2003 Cointegration and Regime-Switching Risk Premia in the U.S. Term Structure of Interest Rates (2003). University of Bonn, Germany / Bonn Econ Discussion Papers (2) RePEc:bri:uobdis:03/552 Sibling Death Clustering in India: Genuine Scarring vs Unobserved Heterogeneity (2003). Department of Economics, University of Bristol, UK / Bristol Economics Discussion Papers (3) RePEc:cam:camdae:0346 A Simple Panel Unit Root Test in the Presence of Cross Section Dependence (2003). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (4) RePEc:cam:camdae:0347 On The Panel Unit Root Tests Using Nonlinear Instrumental Variables (2003). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (5) RePEc:ces:ceswps:_1030 Relationship Between Maternal Behavior During Pregnancy, Birth Outcome, and Early Childhood Development: An Exploratory Study (2003). CESifo GmbH / CESifo Working Paper Series (6) RePEc:ces:ceswps:_1111 Intra-and International Risk-Sharing in the Short Run and the Long Run (2003). CESifo GmbH / CESifo Working Paper Series (7) RePEc:cfs:cfswop:wp200335 Some Like it Smooth, and Some Like it Rough: Untangling Continuous and Jump Components in Measuring, Modeling, and Forecasting Asset Return Volatility (2003). Center for Financial Studies / CFS Working Paper Series (8) RePEc:chb:bcchwp:215 Purchasing Power Parity in an Emerging Market Economy: A Long-Span Study for Chile. (2003). Central Bank of Chile / Working Papers Central Bank of Chile (9) RePEc:cin:ucecwp:2003-06 An Improved Panel Unit Root Test Using GLS-Detrending (2003). University of Cincinnati, Department of Economics / University of Cincinnati, Economics Working Papers Series (10) RePEc:cir:cirwor:2003s-02 Efficient Estimation of Jump Diffusions and General Dynamic Models with a Continuum of Moment Conditions (2003). CIRANO / CIRANO Working Papers (11) RePEc:cir:cirwor:2003s-11 Asymptotic Properties of Monte Carlo Estimators of Diffusion Processes (2003). CIRANO / CIRANO Working Papers (12) RePEc:cir:cirwor:2003s-26 There is a Risk-Return Tradeoff After All (2003). CIRANO / CIRANO Working Papers (13) RePEc:cir:cirwor:2003s-38 News Arrival, Jump Dynamics and Volatility Components for Individual Stock Returns (2003). CIRANO / CIRANO Working Papers (14) RePEc:cir:cirwor:2003s-50 Option Valuation with Conditional Skewness (2003). CIRANO / CIRANO Working Papers (15) RePEc:cpr:ceprdp:4102 The European Phillips Curve: Does the NAIRU Exist? (2003). C.E.P.R. Discussion Papers / CEPR Discussion Papers (16) RePEc:crr:crrwps:2003-10 Becoming Oldest-Old: Evidence From Historical U.S. Data (2003). Center for Retirement Research / Working Papers, Center for Retirement Research at Boston College (17) RePEc:cte:wsrepe:ws035212 GENERALIZED SPECTRAL TESTS FOR THE MARTINGALE DIFFERENCE HYPOTHESIS (2003). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (18) RePEc:cte:wsrepe:ws036313 DETECTING LEVEL SHIFTS IN THE PRESENCE OF CONDITIONAL HETEROSCEDASTICITY. (2003). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (19) RePEc:dgr:uvatin:20030081 Misspecification in Linear Spatial Regression Models (2003). Tinbergen Institute / Tinbergen Institute Discussion Papers (20) RePEc:diw:diwwpp:dp391 International Migration to Germany : Estimation of a Time-Series Model and Inference in Panel Cointegration (2003). DIW Berlin, German Institute for Economic Research / Discussion Papers of DIW Berlin (21) RePEc:emo:wp2003:0326 Do Technology Shocks Drive Hours Up or Down? A Little Evidence From an Agnostic Procedure (2003). Department of Economics, Emory University (Atlanta) / Emory Economics (22) RePEc:erm:papers:0317 Health Status and Socio-Economic Inequalities : A Review of the French Litterature (2003). ERMES, University Paris 2 / Working Papers ERMES (23) RePEc:ese:iserwp:2003-02 The Impact of Atypical Employment on Individual Wellbeing: evidence from a panel of British Workers (2003). Institute for Social and Economic Research / ISER working papers (24) RePEc:fip:fedgfe:2003-32 Itô conditional moment generator and the estimation of short rate processes (2003). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (25) RePEc:fip:fedgif:768 What happens after a technology shock? (2003). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (26) RePEc:fip:fedgif:774 How do Canadian hours worked respond to a technology shock? (2003). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (27) RePEc:fip:fedkpr:y:2003:p:9-56 Has the business cycle changed? (2003). Proceedings (28) RePEc:hhs:rbnkwp:0156 Monetary Policy Analysis in a Small Open Economy using Bayesian Cointegrated Structural VARs (2003). Sveriges Riksbank (Central Bank of Sweden) / Working Paper Series (29) RePEc:ide:wpaper:1034 Non Parametric Instrumental Regression (2003). Institut d'Économie Industrielle (IDEI), Toulouse / IDEI Working Papers (30) RePEc:iec:inveco:v:27:y:2003:i:3:p:423-458 Discrete choices with panel data (2003). Investigaciones Economicas (31) RePEc:ifs:ifsewp:03/22 Consequences and predictors of new health events (2003). Institute for Fiscal Studies / IFS Working Papers (32) RePEc:ind:isipdp:03-05 Awareness and the demand for environmental quality: Drinking water in urban India (2003). Indian Statistical Institute, New Delhi, India / Indian Statistical Institute, Planning Unit, New Delhi Discussion Papers (33) RePEc:iza:izadps:dp851 Treatment Effect Heterogeneity in Theory and Practice (2003). Institute for the Study of Labor (IZA) / IZA Discussion Papers (34) RePEc:iza:izadps:dp876 The European Phillips Curve: Does the NAIRU Exist? (2003). Institute for the Study of Labor (IZA) / IZA Discussion Papers (35) RePEc:kud:kuieca:2003_10 Testing for unit roots in panels by using a mixture model (2003). University of Copenhagen. Institute of Economics. Centre for Applied Microeconometrics / CAM Working Papers (36) RePEc:kud:kuieca:2003_12 Estimating Consumption Economies of Scale, Adult Equivalence Scales, and Household Bargaining Power (2003). University of Copenhagen. Institute of Economics. Centre for Applied Microeconometrics / CAM Working Papers (37) RePEc:kud:kuieca:2003_13 Unit root inference in panel data models where the time-series dimension is fixed: A comparison of different tests (2003). University of Copenhagen. Institute of Economics. Centre for Applied Microeconometrics / CAM Working Papers (38) RePEc:lec:leecon:04/17 Bayesian Semiparametric Inference in Multiple Equation Models (2003). Department of Economics, University of Leicester / Discussion Papers in Economics (39) RePEc:lvl:lagrcr:0312 Are New Keynesian Phillips Curved Identified? (2003). (40) RePEc:mcm:qseprr:387 Socioeconomic Influence on the Health of Older People: Estimates Based on Two Longitudinal Surveys (2003). McMaster University / Quantitative Studies in Economics and Population Research Reports (41) RePEc:mcm:sedapp:112 Socioeconomic Influence on the Health of Older People: Estimates Based on Two Longitudinal Surveys (2003). McMaster University / Social and Economic Dimensions of an Aging Population Research Papers (42) RePEc:msh:ebswps:2003-17 Bayesian Estimation of a Stochastic Volatility Model Using Option and Spot Prices: Application of a Bivariate Kalman Filter (2003). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (43) RePEc:nbr:nberwo:10063 Consequences and Predictors of New Health Events (2003). National Bureau of Economic Research, Inc / NBER Working Papers (44) RePEc:nbr:nberwo:9708 Treatment Effect Heterogeneity in Theory and Practice (2003). National Bureau of Economic Research, Inc / NBER Working Papers (45) RePEc:nbr:nberwo:9819 What Happens After a Technology Shock? (2003). National Bureau of Economic Research, Inc / NBER Working Papers (46) RePEc:nbr:nberwo:9933 Becoming Oldest-Old: Evidence from Historical U.S. Data (2003). National Bureau of Economic Research, Inc / NBER Working Papers (47) RePEc:nbr:nberwo:9944 Trade Disruptions and Americas Early Industrialization (2003). National Bureau of Economic Research, Inc / NBER Working Papers (48) RePEc:nsr:niesrd:216 The Determinants of International Migration into the UK: A Panel Based Modelling Approach (2003). National Institute of Economic and Social Research / NIESR Discussion Papers (49) RePEc:qed:wpaper:1014 Technology Adoption Under Relative Factor Price Uncertainty: The Putty-Clay Investment Model (2003). Queen's University, Department of Economics / Working Papers (50) RePEc:rpi:rpiwpe:0302 The Rise and Fall of the Environmental Kuznets Curve (2003). Rensselaer Polytechnic Institute, Department of Economics / Rensselaer Working Papers in Economics (51) RePEc:rut:rutres:200317 Predicting Inflation: Does The Quantity Theory Help? (2003). Rutgers University, Department of Economics / Departmental Working Papers (52) RePEc:taf:apeclt:v:10:y:2003:i:10:p:627-631 The time series behaviour of Brazilian inflation rate: new evidence from unit root tests with good size and power (2003). Applied Economics Letters (53) RePEc:taf:applec:v:35:y:2003:i:9:p:1043-1051 Analysing the effects of labour standards on US export performance. A time series approach with structural change (2003). Applied Economics (54) RePEc:upf:upfgen:711 Measurement and Explanation of Socioeconomic Inequality in Health with Longitudinal Data (2003). Department of Economics and Business, Universitat Pompeu Fabra / Economics Working Papers (55) RePEc:upf:upfses:711 Measurement and Explanation of Socioeconomic Inequality in Health with Longitudinal Data (2003). Department of Economics and Business, Universitat Pompeu Fabra / Working Papers, Research Center on Health and Economics (56) RePEc:wbk:wbrwps:3166 On Measuring Aggregate Social Efficiency (2003). The World Bank / Policy Research Working Paper Series (57) RePEc:wdi:papers:2003-615 Initial Conditions, Institutional Dynamics and Economic Performance: Evidence from the American States (2003). William Davidson Institute at the University of Michigan Stephen M. Ross Business School / William Davidson Institute Working Papers Series (58) RePEc:wdi:papers:2003-625 Generalizing the Causal Effect of Fertility on Female Labor Supply (2003). William Davidson Institute at the University of Michigan Stephen M. Ross Business School / William Davidson Institute Working Papers Series (59) RePEc:wly:hlthec:v:12:y:2003:i:10:p:803-819 Measuring income related inequality in health: standardisation and the partial concentration index (2003). Health Economics (60) RePEc:wpa:wuwpem:0311005 Panel Stationarity Tests with Cross-sectional Dependence (2003). EconWPA / Econometrics (61) RePEc:wpa:wuwpfi:0308002 Testing for Non-Linearity in ASEAN Financial Markets (2003). EconWPA / Finance (62) RePEc:wpa:wuwpfi:0311001 Consistent Estimation of Pricing Kernels from Noisy Price Data (2003). EconWPA / Finance (63) RePEc:wpa:wuwpif:0308001 The Validity of PPP Revisited: An Application of Non-linear Unit Root Test (2003). EconWPA / International Finance (64) RePEc:wpa:wuwpif:0311014 Exchange Rate Relative Price Relationship: Nonlinear Evidence from Malaysia (2003). EconWPA / International Finance (65) RePEc:wpa:wuwpif:0312001 Exchange Rate Relative Price Relationship: Nonlinear Evidence from Malaysia (2003). EconWPA / International Finance (66) RePEc:wpa:wuwpla:0310002 Generalizing the Causal Effect of Fertility on Female Labor Supply (2003). EconWPA / Labor and Demography (67) RePEc:wpa:wuwpma:0309016 Turbulence, Heterogeneity, and Wage Earnings Inequality (2003). EconWPA / Macroeconomics (68) RePEc:wpe:papers:wpechco Quand un et un ne font plus deux: calcul déchelles déquivalence intra-familiales au moyen dun modèle collectif (2003). Latest citations received in: 2002 (1) RePEc:aah:aarhec:2002-18 Multivariate Lagrange Multiplier Tests for Fractional Integration (2002). Department of Economics, University of Aarhus / Department of Economics, Working Papers (2) RePEc:aah:aarhec:2002-6 Efficient Inference in Multivariate Fractionally Integrated Time Series Models (2002). Department of Economics, University of Aarhus / Department of Economics, Working Papers (3) RePEc:aah:aarhec:2002-8 Local Whittle Analysis of Stationary Fractional Cointegration (2002). Department of Economics, University of Aarhus / Department of Economics, Working Papers (4) RePEc:cir:cirwor:2002s-85 Testing Mean-Variance Efficiency in CAPM with Possibly Non-Gaussian Errors: an Exact Simulation-Based Approach (2002). CIRANO / CIRANO Working Papers (5) RePEc:cir:cirwor:2002s-90 Analytic Evaluation of Volatility Forecasts (2002). CIRANO / CIRANO Working Papers (6) RePEc:cir:cirwor:2002s-91 Correcting the Errors: A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). CIRANO / CIRANO Working Papers (7) RePEc:cir:cirwor:2002s-92 ARMA Representation of Two-Factor Models (2002). CIRANO / CIRANO Working Papers (8) RePEc:cir:cirwor:2002s-93 ARMA Representation of Integrated and Realized Variances (2002). CIRANO / CIRANO Working Papers (9) RePEc:cpd:pd2002:a4-1 Aggregate vs Disaggregate Data Analysis - A Paradox in the Estimation of Money Demand Function of Japan Under the Low Interest Rate Policy (2002). International Conferences on Panel Data / 10th International Conference on Panel Data, Berlin, July 5-6, 2002 (10) RePEc:cpd:pd2002:a5-2 Panel VAR Models with Spatial Dependence (2002). International Conferences on Panel Data / 10th International Conference on Panel Data, Berlin, July 5-6, 2002 (11) RePEc:cpd:pd2002:d3-1 Statistical Measurement of Income Polarization. A cross-national comparison (2002). International Conferences on Panel Data / 10th International Conference on Panel Data, Berlin, July 5-6, 2002 (12) RePEc:cpr:ceprdp:3671 In-Sample or Out-of-Sample Tests of Predictability: Which One Should We Use? (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (13) RePEc:cte:wsrepe:ws025414 ESTIMATION METHODS FOR STOCHASTIC VOLATILITY MODELS: A SURVEY (2002). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (14) RePEc:cvs:starer:02-02 Wavelets in Economics and Finance: Past and Future (2002). C.V. Starr Center for Applied Economics, New York University / Working Papers (15) RePEc:dgr:eureir:2002295 Bayes estimates of Markov trends in possibly cointegrated series (2002). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (16) RePEc:ecb:ecbwps:20020125 Duration: volume and volatility impact of trades. (2002). European Central Bank / Working Paper Series (17) RePEc:ecj:econjl:v:112:y:2002:i:478:p:c97-c116 Patents, Real Options and Firm Performance (2002). Economic Journal (18) RePEc:eeg:euroeg:16 The Euro-Dollar exchange rate: Is it fundamental'DONE' (2002). European Economy Group / European Economy Group Working Papers (19) RePEc:fir:econom:wp2002_20 Labor-Cost Effects on Relative Prices between Regions of a Monetary Union: Implications for the EMU (2002). Universita' degli Studi di Firenze, Dipartimento di Statistica G. Parenti / Econometrics Working Papers Archive (20) RePEc:fpr:tmddps:102 HIV/AIDS and labor markets in Tanzania (2002). International Food Policy Research Institute (IFPRI) / Working papers (21) RePEc:ham:qmwops:20203 An information-theoretic extension to structural VAR modelling (2002). Hamburg University, Department of Economics / Quantitative Macroeconomics Working Papers (22) RePEc:iae:iaewps:wp2002n24 Estimation of Labour Supply Models for Four Separate Groups in the Australian Population (2002). Melbourne Institute of Applied Economic and Social Research, The University of Melbourne / Melbourne Institute Working Paper Series (23) RePEc:ihs:ihsesp:121 Decision Maps for Bivariate Time Series with Potential Thrshold Cointegration (2002). Institute for Advanced Studies / Economics Series (24) RePEc:iza:izadps:dp444 Benefit Entitlement and the Labor Market: Evidence from a Large-Scale Policy Change (2002). Institute for the Study of Labor (IZA) / IZA Discussion Papers (25) RePEc:jae:japmet:v:17:y:2002:i:5:p:425-446 New frontiers for arch models (2002). Journal of Applied Econometrics (26) RePEc:jae:japmet:v:17:y:2002:i:5:p:479-508 A theoretical comparison between integrated and realized volatility (2002). Journal of Applied Econometrics (27) RePEc:jae:japmet:v:17:y:2002:i:5:p:509-534 Maximum likelihood estimation of STAR and STAR-GARCH models: theory and Monte Carlo evidence (2002). Journal of Applied Econometrics (28) RePEc:msh:ebswps:2002-17 A Class of Nonlinear Stochastic Volatility Models and Its Implications on Pricing Currency Options (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (29) RePEc:msh:ebswps:2002-9 Statistical Inference on Changes in Income Inequality in Australia (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (30) RePEc:mtl:montde:2002-17 Testing Mean-Variance Efficiency in CAPM with Possibly Non-Gaussian Errors : An Exact Simulation-Based Approach (2002). Universite de Montreal, Departement de sciences economiques / Cahiers de recherche (31) RePEc:mtl:montde:2002-21 Correcting the Errors : A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). Universite de Montreal, Departement de sciences economiques / Cahiers de recherche (32) RePEc:mtl:montec:17-2002 Testing Mean-Variance Efficiency in CAPM with Possibly Non-Gaussian Errors : An Exact Simulation-Based Approach (2002). Centre interuniversitaire de recherche en économie quantitative, CIREQ / Cahiers de recherche (33) RePEc:mtl:montec:18-2002 Testing for a Unit Root in Panels with Dynamic Factors (2002). Centre interuniversitaire de recherche en économie quantitative, CIREQ / Cahiers de recherche (34) RePEc:mtl:montec:21-2002 Correcting the Errors : A Note on Volatility Forecast Evaluation Based on High-Frequency Data and Realized Volatilities (2002). Centre interuniversitaire de recherche en économie quantitative, CIREQ / Cahiers de recherche (35) RePEc:roc:rocher:495 Pairwise Comparison Estimation of Censored Transformation Models (2002). University of Rochester - Center for Economic Research (RCER) / RCER Working Papers (36) RePEc:taf:emetrv:v:21:y:2002:i:4:p:419-429 FAST DOUBLE BOOTSTRAP TESTS OF NONNESTED LINEAR REGRESSION MODELS (2002). Econometric Reviews (37) RePEc:tud:ddpiec:115 Residual Log-Periodogram Inference for Long-Run Relationships (2002). Institut für Volkswirtschaftslehre (Department of Economics), Technische Universität Darmstadt (Darmstadt University of Technology) / Darmstadt Disc (38) RePEc:ube:dpvwib:dp0210 A Comparison of Johansens, Bierens and the Subspace Algorithm Method for Cointegration Analysis (2002). Universitat Bern, Volkswirtschaftliches Institut / Diskussionsschriften (39) RePEc:una:unccee:wp0902 Multivariate Tests of Fractionally Integrated Hypotheses (2002). School of Economics and Business Administration, University of Navarra / Faculty Working Papers (40) RePEc:wdi:papers:2002-498 Understanding Czech Long-Term Unemployment (2002). William Davidson Institute at the University of Michigan Stephen M. Ross Business School / William Davidson Institute Working Papers Series (41) RePEc:wop:pennin:02-27 Parametric and Nonparametric Volatility Measurement (2002). Wharton School Center for Financial Institutions, University of Pennsylvania / Center for Financial Institutions Working Papers (42) RePEc:wpa:wuwpem:0203005 An information-theoretic extension to structural VAR modelling (2002). EconWPA / Econometrics (43) RePEc:wrk:warwec:654 TESTING FOR COINTEGRATION RANK USING BAYES FACTORS (2002). University of Warwick, Department of Economics / The Warwick Economics Research Paper Series (TWERPS) (44) RePEc:xrs:sfbmaa:02-35 Bracketing effects in categorized survey questions and the measurement of economic quantities (2002). Sonderforschungsbereich 504, University of Mannheim / Sonderforschungsbereich 504 Publications Latest citations received in: 2001 (1) RePEc:aah:aarhec:2001-4 Semiparametric Analysis of Stationary Fractional Cointegration and the Implied-Realized Volatility Relation in High-Frequency Options Data (2001). Department of Economics, University of Aarhus / Department of Economics, Working Papers (2) RePEc:bro:econwp:2001-06 An Unbiased and Powerful Test for Superior Predictive Ability (2001). Brown University, Department of Economics / Working Papers (3) RePEc:cir:cirwor:2001s-70 An Eigenfunction Approach for Volatility Modeling (2001). CIRANO / CIRANO Working Papers (4) RePEc:cpr:ceprdp:2999 UK Inflation in the 1970s and 1980s: The Role of Output Gap Mismeasurement (2001). C.E.P.R. Discussion Papers / CEPR Discussion Papers (5) RePEc:cte:wsrepe:ws010704 OUTLIERS AND CONDITIONAL AUTOREGRESSIVE HETEROSCEDASTICITY IN TIME SERIES (2001). Universidad Carlos III, Departamento de Estadística y Econometría / Statistics and Econometrics Working Papers (6) RePEc:dgr:eureir:2001230 Are statistical reporting agencies getting it right? Data rationality and business cycle asymmetry (2001). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (7) RePEc:dgr:eureri:2001111 Methodological Advances in Dea (2001). Erasmus Research Institute of Management (ERIM), RSM Erasmus University / Research Paper (8) RePEc:dgr:kubcen:200137 On the harm that pretesting does (2001). Tilburg University, Center for Economic Research / Discussion Paper (9) RePEc:fip:fedawp:2001-24 Minimum-variance kernels, economic risk premia, and tests of multi-beta models (2001). Federal Reserve Bank of Atlanta / Working Paper (10) RePEc:fip:fedawp:2001-26 The price of inflation and foreign exchange risk in international equity markets (2001). Federal Reserve Bank of Atlanta / Working Paper (11) RePEc:fip:fedcwp:0106 Maximum likelihood in the frequency domain: the importance of time-to-plan (2001). Federal Reserve Bank of Cleveland / Working Paper (12) RePEc:fip:fedgfe:2001-28 Jump-diffusion term structure and Ito conditional moment generator (2001). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (13) RePEc:fip:fedgfe:2001-49 Estimating stochastic volatility diffusion using conditional moments of integrated volatility (2001). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (14) RePEc:fip:fedgif:710 Testing optimality in job search models (2001). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (15) RePEc:fip:fedhwp:wp-01-15 Recovering risk aversion from options (2001). Federal Reserve Bank of Chicago / Working Paper Series (16) RePEc:fip:fedkrw:rwp01-14 Evaluating long-horizon forecasts (2001). Federal Reserve Bank of Kansas City / Research Working Paper (17) RePEc:gen:geneem:2001.02 Robust Inference Based on Quasi-likelihoods for Genralized Linear Models and Longitudinal Data (2001). Département d'Econométrie, Université de Genève / Cahiers du Département d'Econométrie (18) RePEc:hhs:gunwpe:0054 Stochastic Production and Heterogeneous Risk Preferences: Commercial Fishers Gear Choices (2001). Göteborg University, Department of Economics / Working Papers in Economics (19) RePEc:iza:izadps:dp400 The Predictive Value of Subjective Labour Supply Data: A Dynamic Panel Data Model with Measurement Error (2001). Institute for the Study of Labor (IZA) / IZA Discussion Papers (20) RePEc:jae:japmet:v:16:y:2001:i:5:p:563-576 Model uncertainty in cross-country growth regressions (2001). Journal of Applied Econometrics (21) RePEc:lsu:lsuwpp:2001-11 Maximum Entropy Estimation in Economic Models with Linear Inequality Restrictions (2001). Department of Economics, Louisiana State University / Departmental Working Papers (22) RePEc:lsu:lsuwpp:2006-01 Initial Conditions, European Colonialism and Africas Growth (2001). Department of Economics, Louisiana State University / Departmental Working Papers (23) RePEc:nbr:nberwo:8636 The Curse of Non-Investment Grade Countries (2001). National Bureau of Economic Research, Inc / NBER Working Papers (24) RePEc:wpa:wuwpem:0110002 Model uncertainty in cross-country growth regressions (2001). EconWPA / Econometrics (25) RePEc:wpa:wuwpem:9903003 Model uncertainty in cross-country growth regressions (2001). EconWPA / Econometrics (26) RePEc:wpa:wuwpur:0110002 Spatial Analysis of Regional Income Inequality (2001). EconWPA / Urban/Regional Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |