|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

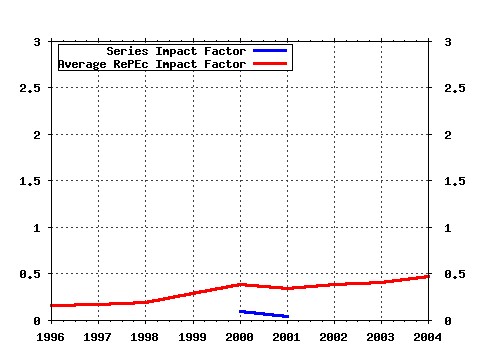

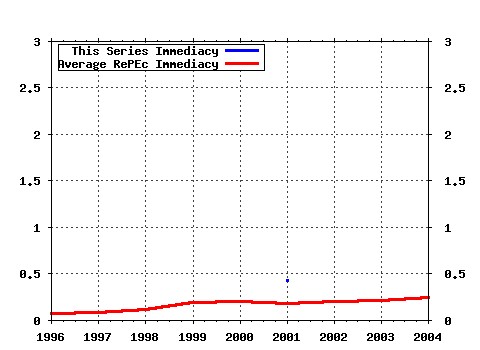

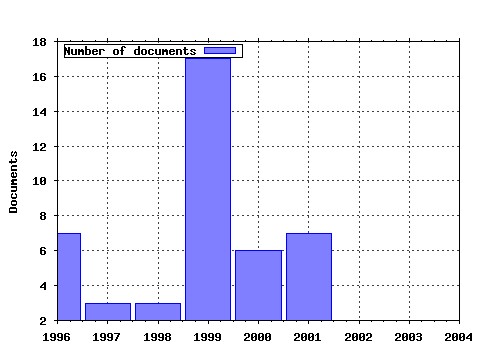

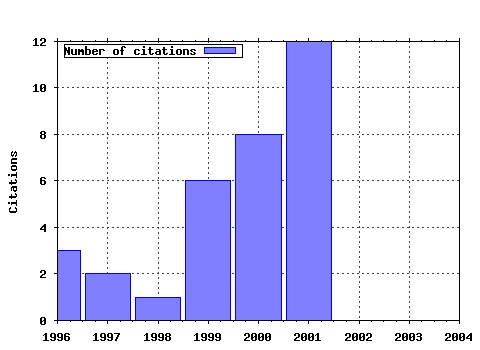

Banque de France - Direction Generale des Etudes / Banque de France - Direction Generale des Etudes Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:fth:banfra:15 Derivative Asset Pricing With Transaction Costs. (1991). (2) RePEc:fth:banfra:82 Conditional Dependency of Financial Series: An Application of Copulas. (2001). (3) RePEc:fth:banfra:16 European Integration and the Demand for Broad Money. (1991). (4) RePEc:fth:banfra:31 Politique monetaire et concurrence bancaire. (1995). (5) RePEc:fth:banfra:60 Fiscal Policy in the Transition to Monetary Union: a Structural VAR Model. (1999). (6) RePEc:fth:banfra:74 Leading Indicators of Currency Crises in Emerging Economies. (2000). (7) RePEc:fth:banfra:48 La relation entre le taux des credits et le cout des ressources bancaires. Modelisation et estimation sur donnees individuelles de banques. (1997). (8) RePEc:fth:banfra:76 Evaluating Monetary Policy Rules in Estimated Forward-Looking Models: A Comparison of US and German Monetary Policies. (2000). (9) RePEc:fth:banfra:79 Entropy Densities: with an Application to Autoregressive Conditional Skewness and Kurtosis. (2001). (10) RePEc:fth:banfra:36 Les strategies de Stop Loss : Theorie et application au contrat notionnel du MATIF. (1996). (11) RePEc:fth:banfra:83 Assessing GMM Estimates of the Federal Reserve Reaction Function. (2001). (12) RePEc:fth:banfra:12 Consumption and Portfolio Decisions with Labor Income and Borrowing Constraints. (1990). (13) RePEc:fth:banfra:34 Is There a Premium for Currencies Correlated with Volatility? Some Evidence from Risk Reversals. (1996). (14) RePEc:fth:banfra:73 Does Correlation between Stock Returns Really Increase during Turbulent Period?. (2000). (15) RePEc:fth:banfra:30 Competition among Financial Intermediaries and the Risk of Contagious Failures. (1995). (16) RePEc:fth:banfra:64 Le partage de la valeur ajoutee en France et en Allemagne. (1999). (17) RePEc:fth:banfra:21 Factor Analysis of the Term Structure: A Probabilistic Approach. (1992). (18) RePEc:fth:banfra:53 Long-Run Causality, with an Application to International Links Between Long-Term Interest Rates (1998). (19) RePEc:fth:banfra:77 Conditional Volatility, Skewness, and Kurtosis: Existence and Persistence. (2000). (20) RePEc:fth:banfra:67 La pente des taux contient-elle de linformation sur lactivite economique future?. (1999). (21) RePEc:fth:banfra:25 Spatial Multiproduct Oligopoly. (1994). (22) RePEc:fth:banfra:81 Pitfalls in Investment Euler Equations. (2001). (23) RePEc:fth:banfra:78 Modele a anticipations rationnelles de la conjoncture simulee : MARCOS. (2000). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 Latest citations received in: 2001 (1) RePEc:cdl:ucsdec:2001-17 Estimation of Copula Models for Time Series of Possibly Different Lengths (2001). Department of Economics, UC San Diego / University of California at San Diego, Economics Working Paper Series (2) RePEc:cpr:ceprdp:2762 New Extreme-Value Dependence Measures and Finance Applications (2001). C.E.P.R. Discussion Papers / CEPR Discussion Papers (3) RePEc:ebg:heccah:0719 New Extreme-Value Dependance Measures and Finance Applications (2001). Groupe HEC / Les Cahiers de Recherche Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |