|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

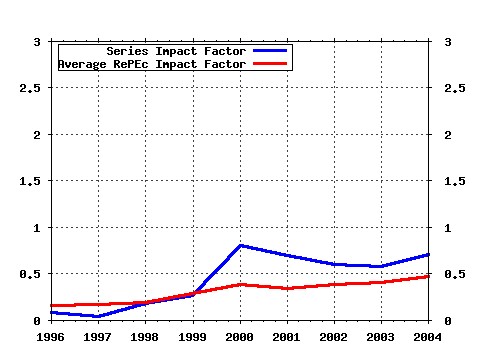

Economics Group, Nuffield College, University of Oxford / Economics Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:nuf:econwp:104 Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. (1995). (2) RePEc:nuf:econwp:0517 Stochastic Volatility (2005). (3) RePEc:nuf:econwp:1999-w12 Auction Theory: a Guide to the Literature. (1999). (4) RePEc:nuf:econwp:0121 GMM Estimation of Empirical Growth Models (2001). (5) RePEc:nuf:econwp:9614 Initial conditions and moment restrictions in dynamic panel data

model (1996). (6) RePEc:nuf:econwp:9604 An omnibus test for univariate and multivariate normalit (1996). (7) RePEc:nuf:econwp:126 Unique Equilibrium in a Model of Self-Fulfilling Currency Attacks. (1996). (8) RePEc:nuf:econwp:0213 Econometric Analysis of Realised Covariation: High Frequency Covariance, Regression and Correlation in Financial Economics (2002). (9) RePEc:nuf:econwp:146 Likelihood INference for Discretely Observed Non-linear Diffusions (1998). (10) RePEc:nuf:econwp:0116 How accurate is the asymptotic approximation to the distribution of realised volatility? (2001). (11) RePEc:nuf:econwp:049 Auctions: Theory and Practice (2004). (12) RePEc:nuf:econwp:9713 Filtering via simulation: auxiliary particle filters (1997). (13) RePEc:nuf:econwp:1999-w3 Innovation and Market Value. (1999). (14) RePEc:nuf:econwp:0603 Designing realised kernels to measure the ex-post variation of equity prices

in the presence of noise (2006). (15) RePEc:nuf:econwp:143 Firm-Level Investment in France and the United States: An Exploration of What We Have Learned in Twenty Years (1998). (16) RePEc:nuf:econwp:0417 We Ran One Regression (2004). (17) RePEc:nuf:econwp:0428 Regular and Modified Kernel-Based Estimators of Integrated Variance:

The Case with Independent Noise (2004). (18) RePEc:nuf:econwp:1999-w11 The Tobacco Deal. (1999). (19) RePEc:nuf:econwp:125 Booms and Busts in the UK Housing Market. (1996). (20) RePEc:nuf:econwp:0113 Inferring Repeated Game Strategies From Actions: Evidence From Trust Game Experiments (2001). (21) RePEc:nuf:econwp:0526 Management of a Capital Stock by Strotzs Naive Planner (2006). (22) RePEc:nuf:econwp:0224 Power Variation and Time Change (2002). (23) RePEc:nuf:econwp:0316 Wage and Price Phillips Curves

An empirical analysis of destabilizing wage-price spirals (2003). (24) RePEc:nuf:econwp:0504 Adjustment Costs and the Identification of Cobb Douglas Production Functions (2005). (25) RePEc:nuf:econwp:048 Capital Accumulation and Growth: A New Look at the Empirical Evidence (2004). (26) RePEc:nuf:econwp:141 Aggregation and Model Construction for Volatility Models (1998). (27) RePEc:nuf:econwp:0011 Bartlett correction of the unit root test in autoregressive models (1995). (28) RePEc:nuf:econwp:0509 Limited Asset Markets Participation, Monetary Policy and (Inverted) Keynesian Logic (2005). (29) RePEc:nuf:econwp:0216 Unemployment, Labour Market Institutions and Shocks (2002). (30) RePEc:nuf:econwp:1999-w20 Income Inequality and Macroeconomic Volatility: an Empirical Investigation. (1999). (31) RePEc:nuf:econwp:0102 Firm Level Investment and R&D in France and the United States: A Comparison (2001). (32) RePEc:nuf:econwp:0211 Economic Forecasting: Some Lessons from Recent Research (2001). (33) RePEc:nuf:econwp:2000-w11 Does Competition Solve the Hold-Up Problem?. (2000). (34) RePEc:nuf:econwp:0320 Multimodality in the GARCH Regression Model (2003). (35) RePEc:nuf:econwp:0008 Generalized linear autoregressions (1995). (36) RePEc:nuf:econwp:0217 Testing the Assumptions Behind the Use of Importance Sampling (2002). (37) RePEc:nuf:econwp:0321 Econometrics of testing for jumps in financial economics using bipower variation (2003). (38) RePEc:nuf:econwp:0204 The Biggest Auction Ever: the Sale of the British 3G Telecom Licenses (2001). (39) RePEc:nuf:econwp:0129 Institutions and Wage Determination: a Multi-Country Approach (2001). (40) RePEc:nuf:econwp:115 Pathological Outcomes of Observational Learning. (1996). (41) RePEc:nuf:econwp:0209 Pooling of Forecasts (2001). (42) RePEc:nuf:econwp:0118 Realised power variation and stochastic volatility models (2001). (43) RePEc:nuf:econwp:0318 Power and bipower variation with stochastic volatility and jumps (2003). (44) RePEc:nuf:econwp:149 A Theory of the Onset of Currency Attacks. (1998). (45) RePEc:nuf:econwp:0005 An evaluation of forecasting using leading indicators (1994). (46) RePEc:nuf:econwp:2000-w14 Optimizing Information in the Herd: Guinea Pigs, Profit and Welfare. (2000). (47) RePEc:nuf:econwp:0020 Analytic convergence rates and parameterisation issues for the Gibbs

sampler applied to state space models (1996). (48) RePEc:nuf:econwp:0310 Identifying, Estimating and Testing Restricted Cointegrated Systems: An Overview (2003). (49) RePEc:nuf:econwp:0201 Dynamics of trade-by-trade price movements: decomposition and models (2002). (50) RePEc:nuf:econwp:0101 Integrated OU Processes (2001). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 (1) RePEc:ads:wpaper:0044 The Unity of Auction Theory: Paul Milgroms Masterclass (2004). Institute for Advanced Study, School of Social Science / Economics Working Papers (2) RePEc:fip:fedgfe:2004-56 Dynamic estimation of volatility risk premia and investor risk aversion from option-implied and realized volatilities (2004). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (3) RePEc:iza:izadps:dp1441 Normative Evaluation of Tax Policies: From Households to Individuals (2004). Institute for the Study of Labor (IZA) / IZA Discussion Papers (4) RePEc:nuf:econwp:0430 Multipower Variation and Stochastic Volatility (2004). Economics Group, Nuffield College, University of Oxford / Economics Papers (5) RePEc:oxf:wpaper:210 `Weak` trends for inference and forecasting in finite samples (2004). University of Oxford, Department of Economics / Economics Series Working Papers (6) RePEc:oxf:wpaper:212 A Comparison of Multi-step GDP Forecasts for South Africa (2004). University of Oxford, Department of Economics / Economics Series Working Papers (7) RePEc:sbs:wpsefe:2004fe22 Multipower Variation and Stochastic Volatility (2004). Oxford Financial Research Centre / OFRC Working Papers Series Latest citations received in: 2003 (1) RePEc:cfs:cfswop:wp200335 Some Like it Smooth, and Some Like it Rough: Untangling Continuous and Jump Components in Measuring, Modeling, and Forecasting Asset Return Volatility (2003). Center for Financial Studies / CFS Working Paper Series (2) RePEc:fip:feddcl:0203 The openness-inflation puzzle revisited (2003). Federal Reserve Bank of Dallas / Center for Latin America Working Papers (3) RePEc:nuf:econwp:0308 Step-by-Step Evolution with State-Dependent Mutations (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (4) RePEc:nuf:econwp:0315 General-to-Specific Model Selection Procedures for Structural Vector Autoregressions (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (5) RePEc:nuf:econwp:0317 Sub-sample Model Selection Procedures in Gets Modelling (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (6) RePEc:nuf:econwp:0318 Power and bipower variation with stochastic volatility and jumps (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (7) RePEc:nuf:econwp:0319 Power variation & stochastic volatility: a review and some new results (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (8) RePEc:nuf:econwp:0321 Econometrics of testing for jumps in financial economics using bipower variation (2003). Economics Group, Nuffield College, University of Oxford / Economics Papers (9) RePEc:uts:wpaper:124 Keynes-Metzler-Goodwin Model Building: The Closed Economy (2003). School of Finance and Economics, University of Technology, Sydney / Working Paper Series (10) RePEc:uts:wpaper:129 The Structure of Keynesian Macrodynamics: A Framework for Future Research (2003). School of Finance and Economics, University of Technology, Sydney / Working Paper Series Latest citations received in: 2002 (1) RePEc:cir:cirwor:2002s-93 ARMA Representation of Integrated and Realized Variances (2002). CIRANO / CIRANO Working Papers (2) RePEc:cpr:ceprdp:3215 How (Not) to Run Auctions: The European 3G Telecom Auctions (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (3) RePEc:dgr:uvatin:20020113 Time Series Models with a Common Stochastic Variance for Analysing Economic Time Series (2002). Tinbergen Institute / Tinbergen Institute Discussion Papers (4) RePEc:jae:japmet:v:17:y:2002:i:5:p:479-508 A theoretical comparison between integrated and realized volatility (2002). Journal of Applied Econometrics (5) RePEc:nuf:econwp:0221 Measuring and forecasting financial variability using realised variance with and without a model (2002). Economics Group, Nuffield College, University of Oxford / Economics Papers (6) RePEc:nuf:econwp:0224 Power Variation and Time Change (2002). Economics Group, Nuffield College, University of Oxford / Economics Papers (7) RePEc:taf:emetrv:v:21:y:2002:i:4:p:397-417 LOG-PERIODOGRAM ESTIMATION OF LONG MEMORY VOLATILITY DEPENDENCIES WITH CONDITIONALLY HEAVY TAILED RETURNS (2002). Econometric Reviews (8) RePEc:uts:rpaper:76 A Score Test for Discreteness in GARCH Models (2002). Quantitative Finance Research Centre, University of Technology, Sydney / Research Paper Series (9) RePEc:wpa:wuwppe:0211004 On the Significance of the Absolute Margin (2002). EconWPA / Public Economics Latest citations received in: 2001 (1) RePEc:bdi:wptemi:td_431_01 Firm investment and monetary transmission in the euro area (2001). Bank of Italy, Economic Research Department / Temi di discussione (Economic working papers) (2) RePEc:cir:cirwor:2001s-71 A Theoretical Comparison Between Integrated andRealized Volatilities / A Theoretical Comparison Between Integrated and Realized Volatilities (2001). CIRANO / CIRANO Working Papers (3) RePEc:nuf:econwp:0104 Econometric analysis of realised volatility and its use in estimating stochastic volatility models (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (4) RePEc:nuf:econwp:0106 Normal modified stable processes (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (5) RePEc:nuf:econwp:0108 Higher order variation and stochastic volatility models (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (6) RePEc:nuf:econwp:0118 Realised power variation and stochastic volatility models (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (7) RePEc:nuf:econwp:0120 Estimating quadratic variation using realised volatility (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (8) RePEc:nuf:econwp:0125 Some recent developments in stochastic volatility modelling (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (9) RePEc:nuf:econwp:0209 Pooling of Forecasts (2001). Economics Group, Nuffield College, University of Oxford / Economics Papers (10) RePEc:oxf:wpaper:072 Normal Modified Stable Processes (2001). University of Oxford, Department of Economics / Economics Series Working Papers (11) RePEc:sce:scecf1:38 Internet Auctions with Artificial Adaptive Agents (2001). Society for Computational Economics / Computing in Economics and Finance 2001 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |