|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

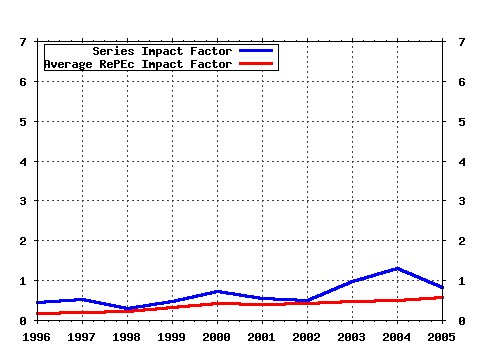

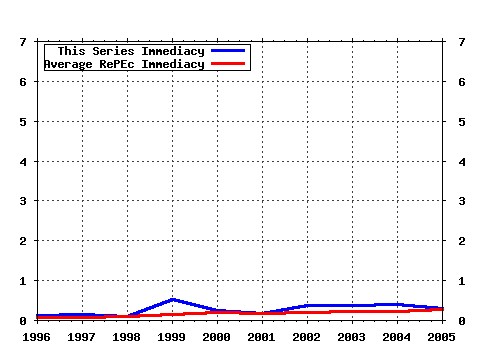

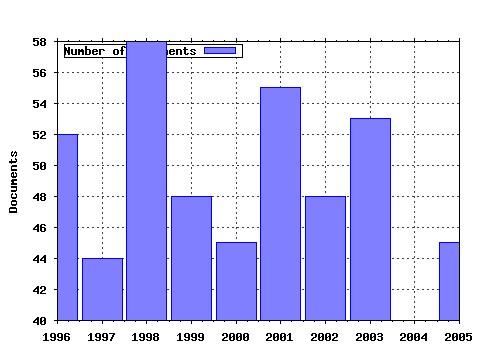

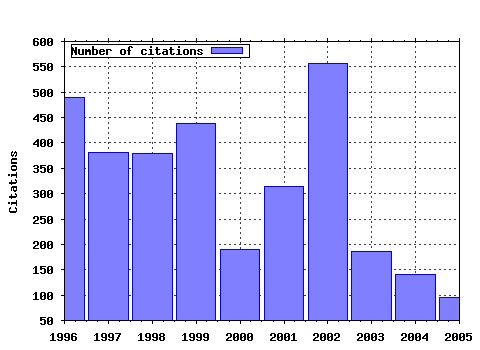

Journal of Business and Economic Statistics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:bes:jnlbes:v:13:y:1995:i:3:p:253-63 Comparing Predictive Accuracy. (1995). (2) RePEc:bes:jnlbes:v:10:y:1992:i:3:p:251-70 Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. (1992). (3) RePEc:bes:jnlbes:v:20:y:2002:i:4:p:518-29 A Survey of Weak Instruments and Weak Identification in Generalized Method of Moments. (2002). (4) RePEc:bes:jnlbes:v:3:y:1985:i:4:p:370-79 Estimation and Inference in Two-Step Econometric Models. (1985). (5) RePEc:bes:jnlbes:v:8:y:1990:i:2:p:153-62 Testing for a Unit Root in a Time Series with a Changing Mean. (1990). (6) RePEc:bes:jnlbes:v:13:y:1995:i:2:p:151-61 Natural and Quasi-experiments in Economics. (1995). (7) RePEc:bes:jnlbes:v:12:y:1994:i:4:p:371-89 Bayesian Analysis of Stochastic Volatility Models. (1994). (8) RePEc:bes:jnlbes:v:7:y:1989:i:2:p:147-59 Tests for Unit Roots: A Monte Carlo Investigation. (1989). (9) RePEc:bes:jnlbes:v:10:y:1992:i:3:p:271-87 Recursive and Sequential Tests of the Unit-Root and Trend-Break Hypotheses: Theory and International Evidence. (1992). (10) RePEc:bes:jnlbes:v:11:y:1993:i:4:p:369-80 Testing for Common Features. (1993). (11) RePEc:bes:jnlbes:v:20:y:2002:i:2:p:147-62 Macroeconomic Forecasting Using Diffusion Indexes. (2002). (12) RePEc:bes:jnlbes:v:17:y:1999:i:1:p:74-90 Earnings and Employment Effects of Continuous Off-the-Job Training in East Germany after Unification. (1999). (13) RePEc:bes:jnlbes:v:15:y:1997:i:3:p:345-53 When Do Long-Run Identifying Restrictions Give Reliable Results? (1997). (14) RePEc:bes:jnlbes:v:14:y:1996:i:1:p:11-30 Evidence on Structural Instability in Macroeconomic Time Series Relations. (1996). (15) RePEc:bes:jnlbes:v:10:y:1992:i:3:p:301-20 Nonstationarity and Level Shifts with an Application to Purchasing Power Parity. (1992). (16) RePEc:bes:jnlbes:v:14:y:1996:i:3:p:262-80 Finite-Sample Properties of Some Alternative GMM Estimators. (1996). (17) RePEc:bes:jnlbes:v:7:y:1989:i:3:p:297-305 The Message in Daily Exchange Rates: A Conditional-Variance Tale. (1989). (18) RePEc:bes:jnlbes:v:11:y:1993:i:4:p:393-95 Testing for Common Features: Reply. (1993). (19) RePEc:bes:jnlbes:v:12:y:1994:i:3:p:361-68 Estimating Potential Output as a Latent Variable. (1994). (20) RePEc:bes:jnlbes:v:8:y:1990:i:2:p:225-34 Persistence in Variance, Structural Change, and the GARCH Model. (1990). (21) RePEc:bes:jnlbes:v:2:y:1984:i:4:p:367-74 Production Frontiers and Panel Data. (1984). (22) RePEc:bes:jnlbes:v:8:y:1990:i:3:p:265-79 Permanent Income, Current Income, and Consumption. (1990). (23) RePEc:bes:jnlbes:v:13:y:1995:i:1:p:27-35 Estimation of Common Long-Memory Components in Cointegrated Systems. (1995). (24) RePEc:bes:jnlbes:v:20:y:2002:i:2:p:163-82 Regime Switches in Interest Rates. (2002). (25) RePEc:bes:jnlbes:v:14:y:1996:i:3:p:353-66 Small-Sample Bias in GMM Estimation of Covariance Structures. (1996). (26) RePEc:bes:jnlbes:v:3:y:1985:i:3:p:216-27 Trends and Cycles in Macroeconomic Time Series. (1985). (27) RePEc:bes:jnlbes:v:17:y:1999:i:1:p:22-35 Humps and Bumps in Lifetime Consumption. (1999). (28) RePEc:bes:jnlbes:v:20:y:2002:i:1:p:45-59 Tests for Parameter Instability in Regressions with I(1) Processes. (2002). (29) RePEc:bes:jnlbes:v:5:y:1987:i:4:p:437-42 Vector Autoregressions and Reality. (1987). (30) RePEc:bes:jnlbes:v:3:y:1985:i:1:p:14-22 Business Location Decisions in the United States: Estimates of the Effects of Unionization, Taxes, and Other Characteristics of States. (1985). (31) RePEc:bes:jnlbes:v:12:y:1994:i:3:p:299-308 Business-Cycle Phases and Their Transitional Dynamics. (1994). (32) RePEc:bes:jnlbes:v:12:y:1994:i:4:p:461-70 Testing for a Unit Root in Time Series with Pretest Data-Based Model Selection. (1994). (33) RePEc:bes:jnlbes:v:16:y:1998:i:3:p:304-11 Unit-Root Tests and Asymmetric Adjustment with an Example Using the Term Structure of Interest Rates. (1998). (34) RePEc:bes:jnlbes:v:16:y:1998:i:2:p:254-59 Tests for Forecast Encompassing. (1998). (35) RePEc:bes:jnlbes:v:3:y:1985:i:3:p:254-83 Estimating Gross Labor-Force Flows. (1985). (36) RePEc:bes:jnlbes:v:10:y:1992:i:4:p:561-65 A Simple Nonparametric Test of Predictive Performance. (1992). (37) RePEc:bes:jnlbes:v:16:y:1998:i:4:p:388-99 Asymptotic Inference on Cointegrating Rank in Partial Systems. (1998). (38) RePEc:bes:jnlbes:v:10:y:1992:i:3:p:237-50 Searching for a Break in GNP. (1992). (39) RePEc:bes:jnlbes:v:12:y:1994:i:2:p:187-204 Approximately Median-Unbiased Estimation of Autoregressive Models. (1994). (40) RePEc:bes:jnlbes:v:12:y:1994:i:3:p:269-77 Inventories and the Three Phases of the Business Cycle. (1994). (41) RePEc:bes:jnlbes:v:11:y:1993:i:1:p:103-12 A Fractional Cointegration Analysis of Purchasing Power Parity. (1993). (42) RePEc:bes:jnlbes:v:11:y:1993:i:1:p:1-15 Bayes Inference via Gibbs Sampling of Autoregressive Time Series Subject to Markov Mean and Variance Shifts. (1993). (43) RePEc:bes:jnlbes:v:17:y:1999:i:1:p:36-49 Symmetrically Normalized Instrumental-Variable Estimation Using Panel Data. (1999). (44) RePEc:bes:jnlbes:v:10:y:1992:i:2:p:229-35 Inequality Constraints in the Univariate GARCH Model. (1992). (45) RePEc:bes:jnlbes:v:13:y:1995:i:4:p:409-17 Sustainability of the Deficit Process with Structural Shifts. (1995). (46) RePEc:bes:jnlbes:v:15:y:1997:i:3:p:300-309 Reconciling the Old and New Census Bureau Education Questions: Recommendations for Researchers. (1997). (47) RePEc:bes:jnlbes:v:9:y:1991:i:4:p:345-59 Semiparametric ARCH Models. (1991). (48) RePEc:bes:jnlbes:v:8:y:1990:i:1:p:31-34 Solving the Stochastic Growth Model by Parameterizing Expectations. (1990). (49) RePEc:bes:jnlbes:v:13:y:1995:i:2:p:225-35 Split-Sample Instrumental Variables Estimates of the Return to Schooling. (1995). (50) RePEc:bes:jnlbes:v:10:y:1992:i:2:p:193-200 A Note on Identification in the Multinomial Probit Model. (1992). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 (1) RePEc:acb:camaaa:2005-07 SOME ECONOMETRIC ANALYSIS OF CONSTRUCTED BINARY TIME SERIES (2005). Australian National University, Centre for Applied Macroeconomic Analysis / CAMA Working Papers (2) RePEc:ces:ceswps:_1465 Heterogeneity within Communities: A Stochastic Model with Tenure Choice (2005). CESifo GmbH / CESifo Working Paper Series (3) RePEc:cpr:ceprdp:5361 Forecast Combinations (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (4) RePEc:emo:wp2003:0502 Higher Power Tests for Bilateral Failure of PPP after 1973 (2005). Department of Economics, Emory University (Atlanta) / Emory Economics (5) RePEc:emo:wp2003:0503 Residuals Bases Tests for the Null of No Cointegration: an Analytical Comparison (2005). Department of Economics, Emory University (Atlanta) / Emory Economics (6) RePEc:fip:fedawp:2005-02 Testing the significance of calendar effects (2005). Federal Reserve Bank of Atlanta / Working Paper (7) RePEc:fip:fedlwp:2005-057 Kalman filtering with truncated normal state variables for Bayesian estimation of macroeconomic models (2005). Federal Reserve Bank of St. Louis / Working Papers (8) RePEc:hhs:bofitp:2005_009 A ten-year retrospection of the behavior of Russian stock returns (2005). Bank of Finland, Institute for Economies in Transition / BOFIT Discussion Papers (9) RePEc:iae:iaewps:wp2005n14 Is There a Unit Root in East-Asian Short-Term Interest Rates? (2005). Melbourne Institute of Applied Economic and Social Research, The University of Melbourne / Melbourne Institute Working Paper Series (10) RePEc:nsr:niesrd:261 Quantitative inference from qualitative business survey panel data: a microeconometric approach (2005). National Institute of Economic and Social Research / NIESR Discussion Papers (11) RePEc:sca:scaewp:0515 Determinants of Job Turnover Intentions: Evidence from Singapore (2005). National University of Singapore, Department of Economics, SCAPE / SCAPE Policy Research Working Paper Series (12) RePEc:wpa:wuwpma:0510016 What Happens After A Technology Shock? A Bayesian Perspective (2005). EconWPA / Macroeconomics (13) RePEc:zur:iewwpx:259 Formalized Data Snooping Based on Generalized Error Rates (2005). Institute for Empirical Research in Economics - IEW / IEW - Working Papers Latest citations received in: 2004 (1) RePEc:cam:camdae:0433 âForecasting Time Series Subject to Multiple Structural Breaksâ (2004). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (2) RePEc:ces:ceswps:_1237 Forecasting Time Series Subject to Multiple Structural Breaks (2004). CESifo GmbH / CESifo Working Paper Series (3) RePEc:cpr:ceprdp:4636 Forecasting Time Series Subject to Multiple Structural Breaks (2004). C.E.P.R. Discussion Papers / CEPR Discussion Papers (4) RePEc:dgr:eureri:30001977 Evaluating Portfolio Value-At-Risk Using Semi-Parametric GARCH Models (2004). Erasmus Research Institute of Management (ERIM), RSM Erasmus University / Research Paper (5) RePEc:dgr:uvatin:20040015 Inference for Adaptive Time Series Models: Stochastic Volatility and Conditionally Gaussian State Space form (2004). Tinbergen Institute / Tinbergen Institute Discussion Papers (6) RePEc:dnb:dnbwpp:022 A Copula-Based Autoregressive Conditional Dependence Model of International Stock Markets (2004). Netherlands Central Bank, Research Department / DNB Working Papers (7) RePEc:ecm:latm04:132 The Use and Abuse of Taylor Rules: How precisely can we estimate them? (2004). Econometric Society / Econometric Society 2004 Latin American Meetings (8) RePEc:fip:fedgfe:2004-52 Macroeconomic volatility, predictability and uncertainty in the Great Moderation: evidence from the survey of professional forecasters (2004). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (9) RePEc:hhs:hastef:0557 Evaluating models of autoregressive conditional duration (2004). Stockholm School of Economics / Working Paper Series in Economics and Finance (10) RePEc:hst:hstdps:d04-43 An Extension of the Markov-Switching Model with Time-Varying Transition Probabilities: Bull-Bear Analysis of the Japanese Stock Market (2004). Institute of Economic Research, Hitotsubashi University / Hi-Stat Discussion Paper Series (11) RePEc:iea:carech:0414 Evaluating Portfolio Value-at-Risk using Semi-Parametric GARCH Models (2004). HEC Montréal, Institut d'économie appliquée / Cahiers de recherche (12) RePEc:iza:izadps:dp1196 Forecasting Time Series Subject to Multiple Structural Breaks (2004). Institute for the Study of Labor (IZA) / IZA Discussion Papers (13) RePEc:jae:japmet:v:19:y:2004:i:3:p:339-354 Why were changes in the federal funds rate smaller in the 1990s? (2004). Journal of Applied Econometrics (14) RePEc:kud:kuieca:2004_04 True versus spurious state dependence in firm performance: the case of West German exports (2004). University of Copenhagen. Institute of Economics. Centre for Applied Microeconometrics / CAM Working Papers (15) RePEc:nuf:econwp:042 Inference for Adaptive Time Series Models: Stochastic Volatility and Conditionally Gaussian State Space Form (2004). Economics Group, Nuffield College, University of Oxford / Economics Papers (16) RePEc:xrs:sfbmaa:04-23 The Relationship Between Risk Attitudes and Heuristics in Search Tasks: A Laboratory Experiment (2004). Sonderforschungsbereich 504, University of Mannheim / Sonderforschungsbereich 504 Publications Latest citations received in: 2003 (1) RePEc:anp:en2003:e75 Business Cycle in the Industrial Production of Brazilian States (2003). ANPEC - Associação Nacional dos Centros de Pósgraduação em Economia [Brazilian Association of Graduate Programs in Economics] / Anais do XXXI Enc (2) RePEc:cdl:ucsdec:2003-11 A Consistent Characteristic-Fuction-Based Test for Conditional Independence (2003). Department of Economics, UC San Diego / University of California at San Diego, Economics Working Paper Series (3) RePEc:cir:cirwor:2003s-33 Exact skewness-kurtosis tests for multivariate normality and goodness-of-fit in multivariate regressions with application to asset pricing models (2003). CIRANO / CIRANO Working Papers (4) RePEc:dgr:eureir:2003320 Modeling category-level purchase timing with Brand-level marketing (2003). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (5) RePEc:dgr:eureir:2003326 Analytical quasi maximum likelihood inference in multivariate volatility models (2003). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (6) RePEc:fgv:epgrbe:4596 The NAIRU, Unemployment and the Rate of Inflation in Brazil (2003). Revista Brasileira de Economia (7) RePEc:gue:guelph:2003-7 Estimates of Semiparametric Equivalence Scales (2003). University of Guelph, Department of Economics / Working Papers (8) RePEc:hhs:rbnkwp:0150 Bayes Estimators of the Cointegration Space (2003). Sveriges Riksbank (Central Bank of Sweden) / Working Paper Series (9) RePEc:ibm:ibmecp:wpe_37 Structural Break Threshold VARs for Predicting US Recessions using the Spread (2003). Ibmec Working Paper, Ibmec São Paulo / Ibmec Working Papers (10) RePEc:ivi:wpasad:2003-33 VOLATILITY AND VAR FORECASTING FOR THE IBEX-35 STOCK-RETURN INDEX USING FIGARCH-TYPE PROCESSES AND DIFFERENT EVALUATION CRITERIA (2003). Instituto Valenciano de Investigaciones Económicas, S.A. (Ivie) / Working Papers. Serie AD (11) RePEc:ivi:wpasad:2003-35 PREFERENCE SHOCKS FROM AGGREGATION: TIME SERIES DATA EVIDENCE (2003). Instituto Valenciano de Investigaciones Económicas, S.A. (Ivie) / Working Papers. Serie AD (12) RePEc:iza:izadps:dp873 The Impact of Office Machinery and Computer Capital on the Demand for Heterogeneous Labour (2003). Institute for the Study of Labor (IZA) / IZA Discussion Papers (13) RePEc:man:cgbcrp:36 Testing for Volatility Changes in US Macroeconomic Time Series (2003). The School of Economic Studies, The Univeristy of Manchester / Centre for Growth and Business Cycle Research Discussion Paper Series (14) RePEc:man:sespap:0331 The Business Cycle in a Financially Deregulated Context: Theory and Evidence (2003). School of Economics, The University of Manchester / The School of Economics Discussion Paper Series (15) RePEc:mtl:montde:2003-09 Exact Skewness-Kurtosis Tests for Multivariate Normality and Goodness-of-fit in Multivariate Regressions with Application to Asset Pricing Models (2003). Universite de Montreal, Departement de sciences economiques / Cahiers de recherche (16) RePEc:mtl:montec:07-2003 Exact Skewness-Kurtosis Tests for Multivariate Normality and Goodness-of-Fit in Multivariate Regressions with Application to Asset Pricing Models (2003). Centre interuniversitaire de recherche en économie quantitative, CIREQ / Cahiers de recherche (17) RePEc:ore:uoecwp:2003-38 Superfund Taint and Neighborhood Change: Ethnicity, Age Distributions, and Household Structure (2003). University of Oregon Economics Department / University of Oregon Economics Department Working Papers (18) RePEc:rut:rutres:200309 Forecasting economic and financial time-series with non-linear models (2003). Rutgers University, Department of Economics / Departmental Working Papers (19) RePEc:zbw:zewdip:1018 Publicly Funded R&D Collaborations and Patent Outcome in Germany (2003). ZEW - Zentrum für Europäische Wirtschaftsforschung / Center for European Economic Research / ZEW Discussion Papers (20) RePEc:zbw:zewdip:1019 Extent and Evolution of the Productivity Gap in Eastern Germany (2003). ZEW - Zentrum für Europäische Wirtschaftsforschung / Center for European Economic Research / ZEW Discussion Papers Latest citations received in: 2002 (1) RePEc:bar:bedcje:200279 Level shifts in a panel data based unit root test. An application to the rate of unemployment (2002). Universitat de Barcelona. Espai de Recerca en Economia / Working Papers in Economics (2) RePEc:bro:econwp:2002-26 Specification Testing and Semiparametric Estimation of Regime Switching Models: An Examination of the US Short Term Interest Rate (2002). Brown University, Department of Economics / Working Papers (3) RePEc:cpr:ceprdp:3312 Instability and Non-Linearity in the EMU (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (4) RePEc:cpr:ceprdp:3332 Uncertainty and Consumer Durables Adjustment (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (5) RePEc:cpr:ceprdp:3529 Forecasting EMU Macroeconomic Variables (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (6) RePEc:cpr:ceprdp:3632 Income Variance Dynamics and Heterogeneity (2002). C.E.P.R. Discussion Papers / CEPR Discussion Papers (7) RePEc:del:abcdef:2002-15 Money, Inflation and output in Romania, 1992-2000. (2002). DELTA (Ecole normale supérieure) / DELTA Working Papers (8) RePEc:dgr:umamet:2002060 European Financial Market Integration: Evidence on the Emergence of a Single Eurozone Retail Banking Market (2002). Maastricht : METEOR, Maastricht Research School of Economics of Technology and Organization / Research Memoranda (9) RePEc:fip:fedbwp:02-3 Estimating the Euler equation for output (2002). Federal Reserve Bank of Boston / Working Papers (10) RePEc:hhb:aarfin:2002_013 Regime Switching in the Yield Curve (2002). Aarhus School of Business, Department of Finance / Working Papers (11) RePEc:lev:wrkpap:358 Threshold Effects in the U.S. Budget Deficit (2002). Levy Economics Institute, The / Economics Working Paper Archive (12) RePEc:mlb:wpaper:862 Assessing Instrumental Variable Relevance:An Alternative Measure and Some Exact Finite Sample Theory (2002). The University of Melbourne / Department of Economics - Working Papers Series (13) RePEc:msh:ebswps:2002-17 A Class of Nonlinear Stochastic Volatility Models and Its Implications on Pricing Currency Options (2002). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (14) RePEc:qld:uq2004:307 Output Adjustment in Developing Countries: a Structural Var Approach (2002). School of Economics, University of Queensland, Australia / Working Papers Series (15) RePEc:taf:eurjfi:v:8:y:2002:i:4:p:402-421 Forecasting inflation in the European Monetary Union: A disaggregated approach by countries and by sectors (2002). European Journal of Finance (16) RePEc:taf:jitecd:v:11:y:2002:i:1:p:77-98 Capital controls, capital flows and external crises: evidence from India (2002). Journal of International Trade & Economic Development (17) RePEc:wop:humbsf:2002-12 Money and Prices: An I(2) Analysis for the Euro Area (2002). Humboldt Universitaet Berlin / Sonderforschungsbereich 373 (18) RePEc:wop:pennin:02-27 Parametric and Nonparametric Volatility Measurement (2002). Wharton School Center for Financial Institutions, University of Pennsylvania / Center for Financial Institutions Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |