|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

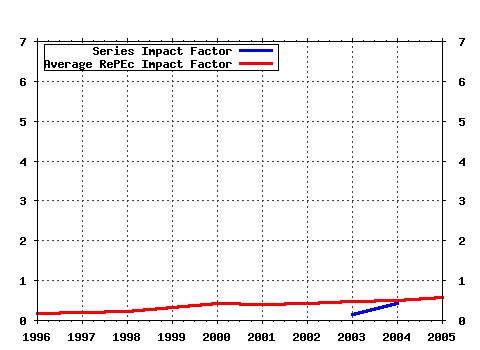

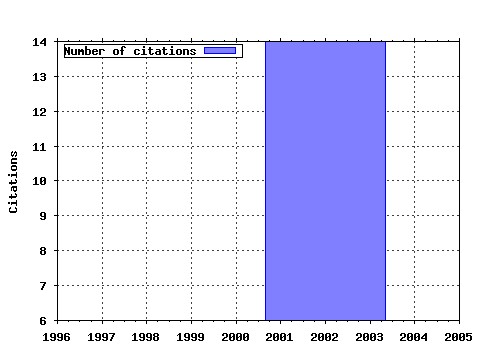

Quantitative Finance Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:taf:quantf:v:2:y:2002:i:6:p:459-467 Consistent pricing and hedging for a modified constant elasticity of variance model (2002). (2) RePEc:taf:quantf:v:2:y:2002:i:6:p:432-442 Pricing of perpetual Bermudan options (2002). (3) RePEc:taf:quantf:v:5:y:2005:i:5:p:489-501 Empirical estimation of tail dependence using copulas: application to Asian markets (2005). (4) RePEc:taf:quantf:v:2:y:2002:i:6:p:415-431 A theory of non-Gaussian option pricing (2002). (5) RePEc:taf:quantf:v:6:y:2006:i:6:p:449-449 The modified Weibull distribution for asset returns (2006). (6) RePEc:taf:quantf:v:6:y:2006:i:2:p:147-158 A new technique for calibrating stochastic volatility models: the Malliavin gradient method (2006). (7) RePEc:taf:quantf:v:5:y:2005:i:6:p:513-517 Statistical properties of demand fluctuation in the financial market (2005). (8) RePEc:taf:quantf:v:6:y:2006:i:6:p:513-536 Fast strong approximation Monte Carlo schemes for stochastic volatility models (2006). (9) RePEc:taf:quantf:v:6:y:2006:i:3:p:197-206 Local volatility function models under a benchmark approach (2006). (10) RePEc:taf:quantf:v:5:y:2005:i:6:p:531-542 Valuation of volatility derivatives as an inverse problem (2005). (11) RePEc:taf:quantf:v:7:y:2007:i:1:p:63-74 The geometry of crashes. A measure of the dynamics of stock market crises (2007). (12) RePEc:taf:quantf:v:2:y:2002:i:6:p:443-453 Probability distribution of returns in the Heston model with stochastic volatility* (2002). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 (1) RePEc:hal:papers:halshs-00179343_v1 How can we define the concept of long memory ? An econometric survey, (2005). HAL, CCSd/CNRS / Pre- and Post-Print documents (2) RePEc:taf:quantf:v:5:y:2005:i:6:p:519-521 Two phase behaviour and the distribution of volume (2005). Quantitative Finance Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |