|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

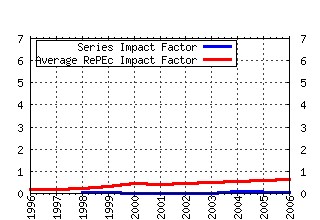

The International Journal of Accounting Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:accoun:v:35:y:2000:i:4:p:495-519 Impact of Culture, Market Forces, and Legal System on Financial Disclosures (2000). (2) RePEc:eee:accoun:v:38:y:2003:i:2:p:173-194 A multinational test of determinants of corporate disclosure (2003). (3) RePEc:eee:accoun:v:34:y:1999:i:1:p:121-131 Firm Characteristics of Swiss Companies that Utilize International Accounting Standards (1999). (4) RePEc:eee:accoun:v:31:y:1996:i:4:p:405-418 International harmonization of reporting required by stock markets (1996). (5) RePEc:eee:accoun:v:37:y:2002:i:1:p:95-111 The changing nature of financial disclosure in Japan (2002). (6) RePEc:eee:accoun:v:31:y:1996:i:2:p:213-237 An investigation into the influence of cultural factors in the international lobbying of the International Accounting Standards Committee: The case of E32, Comparability of Financial Statements (1996). (7) RePEc:eee:accoun:v:34:y:1999:i:1:p:11-48 Acceptance and Observance of International Accounting Standards: An Empirical Study of Companies Claiming to Comply with IASs (1999). (8) RePEc:eee:accoun:v:33:y:1998:i:5:p:529-567 Accounting diversity and firm valuation (1998). (9) RePEc:eee:accoun:v:34:y:1999:i:4:p:557-570 The use of International Accounting Standards terminology, a survey of IAS compliance disclosure (1999). (10) RePEc:eee:accoun:v:31:y:1996:i:3:p:293-331 Environmental disclosures in annual reports: An international perspective (1996). (11) RePEc:eee:accoun:v:38:y:2003:i:2:p:117-143 How it all began: the rise of listing requirements on the London, Berlin, Paris, and New York stock exchanges (2003). (12) RePEc:eee:accoun:v:31:y:1996:i:1:p:55-66 A methodological note on cross-cultural accounting ethics research (1996). (13) RePEc:eee:accoun:v:32:y:1997:i:1:p:1-22 Cash flow statements: An international comparison of regulatory positions (1997). (14) RePEc:eee:accoun:v:31:y:1996:i:3:p:333-346 Environmental performance and reporting: Perceptions of managers and accounting professionals in Hong Kong (1996). (15) RePEc:eee:accoun:v:34:y:1999:i:4:p:491-515 Communists Among Us in a Market Economy: Accountancy in the Peoples Republic of China (1999). (16) RePEc:eee:accoun:v:39:y:2004:i:1:p:71-92 An international investigation of associations between societal variables and the amount of disclosure on information technology and communication problems: The case of Y2K (2004). (17) RePEc:eee:accoun:v:31:y:1996:i:3:p:269-279 International accounting harmonization and the major developed stock market countries: An empirical study (1996). (18) RePEc:eee:accoun:v:37:y:2002:i:2:p:247-265 Ownership structure and corporate voluntary disclosure in Hong Kong and Singapore (2002). (19) RePEc:eee:accoun:v:32:y:1997:i:3:p:301-319 Accuracy of forecast information disclosed in the IPO prospectuses of Hong Kong companies (1997). (20) RePEc:eee:accoun:v:35:y:2000:i:4:p:559-577 Auditing Standards in China--A Comparative Analysis with Relevant International Standards and Guidelines (2000). (21) RePEc:eee:accoun:v:40:y:2005:i:2:p:151-172 The association between ISO 9000 certification and financial performance (2005). (22) RePEc:eee:accoun:v:34:y:1999:i:3:p:349-373 Corporate disclosures made by Chinese listed companies (1999). (23) RePEc:eee:accoun:v:32:y:1997:i:2:p:203-235 International accounting research: An analysis of thirty-two years from the international journal of accounting (1997). (24) RePEc:eee:accoun:v:38:y:2003:i:4:p:431-455 Pricing and supplier concentration in the private client segment of the audit market: Market power or competition? (2003). (25) RePEc:eee:accoun:v:34:y:1999:i:2:p:209-238 Voluntary environmental and social accounting disclosure practices in the Asia-Pacific region: an international empirical test of political economy theory (1999). (26) RePEc:eee:accoun:v:36:y:2001:i:3:p:311-327 Accounting and management controls in the classical Chinese novel: A Dream of the Red Mansions (2001). (27) RePEc:eee:accoun:v:42:y:2007:i:2:p:143-147 Discussion of Attribute differences between U.S. GAAP and IFRS earnings: An exploratory study (2007). (28) RePEc:eee:accoun:v:32:y:1997:i:1:p:99-117 International accounting education: Insights from academicians and practitioners (1997). (29) RePEc:eee:accoun:v:35:y:2000:i:3:p:331-353 Corporate Ownership and Governance in Russia (2000). (30) RePEc:eee:accoun:v:36:y:2001:i:1:p:91-113 An empirical examination of corporate myopic behavior: a comparison of Japanese and U.S. companies (2001). (31) RePEc:eee:accoun:v:41:y:2006:i:3:p:290-292 Board composition, regulatory regime, and voluntary disclosure (2006). (32) RePEc:eee:accoun:v:35:y:2000:i:1:p:27-63 Assessing the Acceptability of International Accounting Standards in the US: An Empirical Study of the Materiality of US GAAP Reconciliations by Non-US Companies Complying with IASC Standards (2000). (33) RePEc:eee:accoun:v:37:y:2002:i:3:p:301-325 Ownership structure and earnings informativeness: Evidence from Korea (2002). (34) RePEc:eee:accoun:v:33:y:1998:i:2:p:211-234 Corporate financial disclosure in emerging markets: Does economic development matter? (1998). (35) RePEc:eee:accoun:v:36:y:2001:i:1:p:33-45 Agency effects and escalation of commitment: do small national culture differences matter? (2001). (36) RePEc:eee:accoun:v:40:y:2005:i:4:p:399-422 Corporate mandatory disclosure practices in Bangladesh (2005). (37) RePEc:eee:accoun:v:37:y:2002:i:2:p:183-213 Global expectations and their association with corporate social disclosure practices in Australia, Singapore, and South Korea (2002). (38) RePEc:eee:accoun:v:32:y:1997:i:3:p:247-278 Cultural and economic influences on current accounting standards in the Peoples Republic of China (1997). (39) RePEc:eee:accoun:v:35:y:2000:i:4:p:539-557 On the Myth of Anglo-Saxon Financial Accounting (2000). (40) RePEc:eee:accoun:v:34:y:1999:i:2:p:239-248 An empirical investigation of multinational firms compliance with International Accounting Standards (1999). (41) RePEc:eee:accoun:v:36:y:2001:i:4:p:391-406 The nature of information in accruals and cash flows in an emerging capital market: The case of China (2001). (42) RePEc:eee:accoun:v:32:y:1997:i:2:p:139-153 Problems of accounting reform in the Peoples Republic of China (1997). (43) RePEc:eee:accoun:v:35:y:2000:i:4:p:471-493 The Impact of Adopting International Accounting Standards on the Harmonization of Accounting Practices (2000). (44) RePEc:eee:accoun:v:31:y:1996:i:1:p:95-120 A comparative study of cultural influences on financial reporting in the U.S. and The Netherlands (1996). (45) RePEc:eee:accoun:v:36:y:2001:i:2:p:147-167 Accounting for brands in France and Germany compared with IAS 38 (intangible assets): An illustration of the difficulty of international harmonization (2001). (46) RePEc:eee:accoun:v:42:y:2007:i:1:p:25-56 Accounting for financial instruments: An analysis of the determinants of disclosure in the Portuguese stock exchange (2007). (47) RePEc:eee:accoun:v:32:y:1997:i:1:p:23-44 Anglo-Saxon and German life-cycle costing (1997). (48) RePEc:eee:accoun:v:35:y:2000:i:2:p:173-187 The Future of Financial Reporting in Europe: Its Role in Corporate Governance (2000). (49) RePEc:eee:accoun:v:38:y:2003:i:1:p:1-22 Audit firm size, public ownership, and firms discretionary accruals management (2003). (50) RePEc:eee:accoun:v:36:y:2001:i:1:p:65-90 Improving activities and decreasing costs of logistics in hospitals: a comparison of U.S. and French hospitals (2001). Recent citations received in: | 2006 | 2005 | 2004 | 2003 Recent citations received in: 2006 Recent citations received in: 2005 Recent citations received in: 2004 (1) RePEc:por:fepwps:150 Accounting practices for financial instruments. How far are Portuguese companies from IAS? (2004). Universidade do Porto, Faculdade de Economia do Porto / FEP Working Papers Recent citations received in: 2003 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||