|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

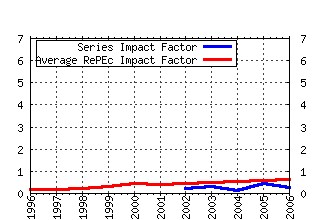

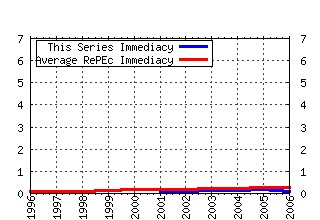

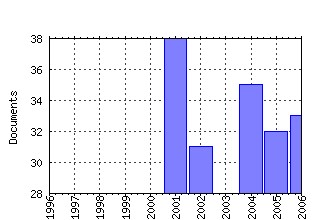

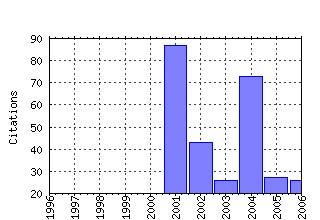

Journal of Forecasting Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:jof:jforec:v:23:y:2004:i:6:p:405-430 Combination forecasts of output growth in a seven-country data set (2004). (2) RePEc:jof:jforec:v:20:y:2001:i:3:p:161-79 Impulse Response Analysis in Vector Autoregressions with Unknown Lag Order. (2001). (3) RePEc:jof:jforec:v:23:y:2004:i:7:p:479-496 Finding good predictors for inflation: a Bayesian model averaging approach (2004). (4) RePEc:jof:jforec:v:20:y:2001:i:8:p:581-601 Forecasting with k-Factor Gegenbauer Processes: Theory and Applications. (2001). (5) RePEc:jof:jforec:v:21:y:2002:i:7:p:513-42 The Performance of Non-linear Exchange Rate Models: A Forecasting Comparison. (2002). (6) RePEc:jof:jforec:v:23:y:2004:i:3:p:173-196 Vector smooth transition regression models for US GDP and the composite index of leading indicators (2004). (7) RePEc:jof:jforec:v:20:y:2001:i:1:p:1-19 Testing in Unobserved Components Models. (2001). (8) RePEc:jof:jforec:v:25:y:2006:i:2:p:129-152 Autoregressive gamma processes (2006). (9) RePEc:jof:jforec:v:26:y:2007:i:4:p:271-302 Forecasting German GDP using alternative factor models based on large datasets (2007). (10) RePEc:jof:jforec:v:22:y:2003:i:1:p:1-22 Volatility forecasting for risk management (2003). (11) RePEc:jof:jforec:v:23:y:2004:i:8:p:541-557 Comparing the accuracy of density forecasts from competing models (2004). (12) RePEc:jof:jforec:v:20:y:2001:i:6:p:441-49 Creating High-Frequency National Accounts with State-Space Modelling: A Monte Carlo Experiment. (2001). (13) RePEc:jof:jforec:v:20:y:2001:i:2:p:87-109 Evaluating the Predictive Accuracy of Volatility Models. (2001). (14) RePEc:jof:jforec:v:23:y:2004:i:6:p:431-447 Quarterly real GDP estimates for China and ASEAN4 with a forecast evaluation (2004). (15) RePEc:jof:jforec:v:21:y:2002:i:3:p:181-92 Relationships between Australian Real Estate and Stock Market Prices--A Case of Market Inefficiency. (2002). (16) RePEc:jof:jforec:v:24:y:2005:i:3:p:189-201 Beating the random walk in Central and Eastern Europe (2005). (17) RePEc:jof:jforec:v:22:y:2003:i:5:p:359-375 On SETAR non-linearity and forecasting (2003). (18) RePEc:jof:jforec:v:23:y:2004:i:1:p:19-49 Medium-term forecasts of potential GDP and inflation using age structure information (2004). (19) RePEc:jof:jforec:v:20:y:2001:i:6:p:425-40 Choosing among Competing Econometric Forecasts: Regression-Based Forecast Combination Using Model Selection. (2001). (20) RePEc:jof:jforec:v:24:y:2005:i:2:p:77-103 Forecasting recessions using the yield curve (2005). (21) RePEc:jof:jforec:v:24:y:2005:i:1:p:17-37 Prediction intervals for exponential smoothing using two new classes of state space models (2005). (22) RePEc:jof:jforec:v:21:y:2002:i:7:p:473-500 A Threshold Stochastic Volatility Model. (2002). (23) RePEc:jof:jforec:v:21:y:2002:i:5:p:381-93 An Outlier Robust GARCH Model and Forecasting Volatility of Exchange Rate Returns. (2002). (24) RePEc:jof:jforec:v:20:y:2001:i:2:p:135-43 A Double-Threshold GARCH Model for the French Franc/Deutschmark Exchange Rate. (2001). (25) RePEc:jof:jforec:v:25:y:2006:i:3:p:209-221 The importance of interest rates for forecasting the exchange rate (2006). (26) RePEc:jof:jforec:v:21:y:2002:i:7:p:501-11 Forecasting Daily Foreign Exchange Rates Using Genetically Optimized Neural Networks. (2002). (27) RePEc:jof:jforec:v:21:y:2002:i:2:p:81-105 Testing for (Common) Stochastic Trends in the Presence of Structural Breaks. (2002). (28) RePEc:jof:jforec:v:24:y:2005:i:8:p:539-556 Forecasting and signal extraction with misspecified models (2005). (29) RePEc:jof:jforec:v:20:y:2001:i:1:p:21-35 Alternative Regime Switching Models for Forecasting Inflation. (2001). (30) RePEc:jof:jforec:v:20:y:2001:i:5:p:329-40 A Fractionally Integrated Exponential Model for UK Unemployment. (2001). (31) RePEc:jof:jforec:v:21:y:2002:i:8:p:543-58 Forecasting Trend Output in the Euro Area. (2002). (32) RePEc:jof:jforec:v:23:y:2004:i:2:p:115-139 Can out-of-sample forecast comparisons help prevent overfitting? (2004). (33) RePEc:jof:jforec:v:25:y:2006:i:2:p:101-128 Evaluating predictive performance of value-at-risk models in emerging markets: a reality check (2006). (34) RePEc:jof:jforec:v:25:y:2006:i:6:p:401-413 Are forecasters reluctant to revise their predictions? Some German evidence (2006). (35) RePEc:jof:jforec:v:23:y:2004:i:5:p:315-335 Long-run forecasting in multicointegrated systems (2004). (36) RePEc:jof:jforec:v:22:y:2003:i:4:p:337-358 Selection of Value-at-Risk models (2003). (37) RePEc:jof:jforec:v:23:y:2004:i:1:p:51-66 Forecasting football results and the efficiency of fixed-odds betting (2004). (38) RePEc:jof:jforec:v:20:y:2001:i:4:p:273-83 Identification of Asymmetric Prediction Intervals through Causal Forces. (2001). (39) RePEc:jof:jforec:v:22:y:2003:i:2-3:p:129-160 Identifying emerging generic technologies at the national level: the UK experience (2003). (40) RePEc:jof:jforec:v:25:y:2006:i:1:p:49-75 Building neural network models for time series: a statistical approach (2006). (41) RePEc:jof:jforec:v:20:y:2001:i:6:p:405-24 Forecasting UK Industrial Production over the Business Cycle. (2001). (42) RePEc:jof:jforec:v:22:y:2003:i:1:p:35-47 Modelling trends in central England temperatures (2003). (43) RePEc:jof:jforec:v:23:y:2004:i:4:p:275-296 Updating ARMA predictions for temporal aggregates (2004). (44) RePEc:jof:jforec:v:24:y:2005:i:7:p:523-537 The multi-chain Markov switching model (2005). (45) RePEc:jof:jforec:v:27:y:2008:i:1:p:41-51 Can forecasting performance be improved by considering the steady state? An application to Swedish inflation and interest rate (2008). (46) RePEc:jof:jforec:v:20:y:2001:i:4:p:285-95 Robust Evaluation of Fixed-Event Forecast Rationality. (2001). (47) RePEc:jof:jforec:v:21:y:2002:i:4:p:245-64 The Data Measurement Process for UK GNP: Stochastic Trends, Long Memory, and Unit Roots. (2002). (48) RePEc:jof:jforec:v:22:y:2003:i:4:p:299-315 Non-linear forecasts of stock returns (2003). (49) RePEc:jof:jforec:v:23:y:2004:i:8:p:586-601 A fractal forecasting model for financial time series (2004). (50) RePEc:jof:jforec:v:20:y:2001:i:3:p:203-29 Sensitivity of Univariate AR(1) Time-Series Forecasts Near the Unit Root. (2001). Recent citations received in: | 2006 | 2005 | 2004 | 2003 Recent citations received in: 2006 (1) RePEc:diw:diwvjh:75-2-2 Geschichte der quantitativen Konjunkturprognose-Evaluation in Deutschland (2006). Vierteljahrshefte zur Wirtschaftsforschung / Quarterly Journal of Economic Research (2) RePEc:dun:dpaper:191 Non-Stationary Inflation and the Markup: an Overview of the Research and some Implications for Policy (2006). University of Dundee, Economic Studies / Discussion Papers (3) RePEc:fgv:epgewp:630 Are price limits on futures markets that cool? Evidence from the Brazilian Mercantile and Futures Exchange (2006). Graduate School of Economics, Getulio Vargas Foundation (Brazil) / Economics Working Papers (Ensaios Economicos da EPGE) Recent citations received in: 2005 (1) RePEc:fau:wpaper:wp075 Real Equilibrium Exchange Rate Estimates: To What Extent Are They Applicable for Setting the Central Parity? (2005). Charles University Prague, Faculty of Social Sciences, Institute of Economic Studies / Working Papers IES (2) RePEc:fau:wpaper:wp076 Fiscal Policy in New EU Member States: Go East, Prudent Man! (2005). Charles University Prague, Faculty of Social Sciences, Institute of Economic Studies / Working Papers IES (3) RePEc:hhs:hastef:0598 Forecasting economic variables with nonlinear models (2005). Stockholm School of Economics / Working Paper Series in Economics and Finance (4) RePEc:sza:wpaper:wpapers13 The properties of cycles in South African financial variables and their relation to the business cycle (2005). Stellenbosch University, Department of Economics / Working Papers (5) RePEc:wpa:wuwpif:0509006 Real Equilibrium Exchange Rate Estimates: To What Extent Applicable for Setting the Central Parity? (2005). EconWPA / International Finance (6) RePEc:wpa:wuwpur:0501005 Borderplex Bridge and Air Econometric Forecast Accuracy (2005). EconWPA / Urban/Regional Recent citations received in: 2004 (1) RePEc:cam:camdae:0433 âForecasting Time Series Subject to Multiple Structural Breaksâ (2004). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (2) RePEc:fda:fdaddt:2004-22 Structural Breaks in Volatility: Evidence from the OECD Real Exchange Rates (2004). FEDEA / Working Papers (3) RePEc:fip:fedkrw:rwp04-10 Improving forecast accuracy by combining recursive and rolling forecasts (2004). Federal Reserve Bank of Kansas City / Research Working Paper (4) RePEc:hhs:ifswps:2004_007 Demographically based global income forecasts up to the year 2050 (2004). Institute for Futures Studies / Arbetsrapport (5) RePEc:hhs:uunewp:2004_013 Estimating the Relationship between Age Structure and GDP in the OECD Using Panel Cointegration Methods (2004). Uppsala University, Department of Economics / Working Paper Series Recent citations received in: 2003 (1) RePEc:dgr:eureir:2003315 Selecting a nonlinear time series model using weighted tests of equal forecast accuracy (2003). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (2) RePEc:dgr:eureir:2003321 Forecasting industrial production with linear, nonlinear and structural change models (2003). Erasmus University Rotterdam, Econometric Institute / Econometric Institute Report (3) RePEc:ham:qmwops:20305 Die Konstruktion und Schätzung eines Frühindikators für die Konjunkturentwicklung in der Freien und Hansestadt Hamburg (2003). Hamburg University, Department of Economics / Quantitative Macroeconomics Working Papers (4) RePEc:has:discpr:0313 Socio-Economic and Developmental Needs - Focus of Foresight Programmes (2003). Institute of Economics, Hungarian Academy of Sciences / IEHAS Discussion Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||