|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

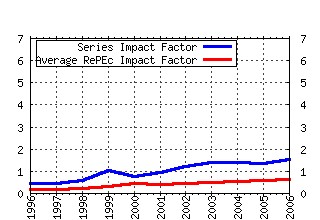

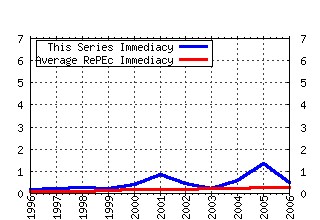

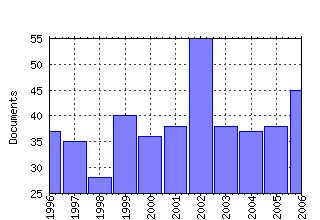

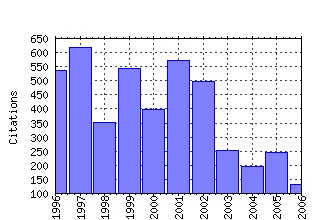

Review of Financial Studies Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:oup:rfinst:v:1:y:1988:i:3:p:195-228 The Dividend-Price Ratio and Expectations of Future Dividends and Discount Factors (1988). (2) RePEc:oup:rfinst:v:1:y:1988:i:1:p:41-66 Stock Market Prices do not Follow Random Walks: Evidence from a Simple Specification Test (1988). (3) RePEc:oup:rfinst:v:1:y:1988:i:1:p:3-40 A Theory of Intraday Patterns: Volume and Price Variability (1988). (4) RePEc:oup:rfinst:v:5:y:1992:i:3:p:357-86 Dividend Yields and Expected Stock Returns: Alternative Procedures for Inference and Measurement. (1992). (5) RePEc:oup:rfinst:v:6:y:1993:i:2:p:327-43 A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. (1993). (6) RePEc:oup:rfinst:v:3:y:1990:i:4:p:573-92 Pricing Interest-Rate-Derivative Securities. (1990). (7) RePEc:oup:rfinst:v:3:y:1990:i:1:p:5-33 Transmission of Volatility between Stock Markets. (1990). (8) RePEc:oup:rfinst:v:5:y:1992:i:2:p:153-80 Dynamic Equilibrium and the Real Exchange Rate in a Spatially Separated World. (1992). (9) RePEc:oup:rfinst:v:5:y:1992:i:2:p:199-242 Stock Prices and Volume. (1992). (10) RePEc:oup:rfinst:v:9:y:1996:i:1:p:69-107 Jumps and Stochastic Volatility: Exchange Rate Processes Implicit in Deutsche Mark Options. (1996). (11) RePEc:oup:rfinst:v:3:y:1990:i:2:p:281-307 Correlations in Price Changes and Volatility across International Stock Markets. (1990). (12) RePEc:oup:rfinst:v:12:y:1999:i:4:p:687-720 Modeling Term Structures of Defaultable Bonds. (1999). (13) RePEc:oup:rfinst:v:6:y:1993:i:3:p:527-66 The Risk and Predictability of International Equity Returns. (1993). (14) RePEc:oup:rfinst:v:13:y:2000:i:4:p:959-84 The Interaction between Product Market and Financing Strategy: The Role of Venture Capital. (2000). (15) RePEc:oup:rfinst:v:10:y:1997:i:2:p:481-523 A Markov Model for the Term Structure of Credit Risk Spreads. (1997). (16) RePEc:oup:rfinst:v:9:y:1996:i:2:p:385-426 Testing Continuous-Time Models of the Spot Interest Rate. (1996). (17) RePEc:oup:rfinst:v:14:y:2001:i:3:p:659-80 Familiarity Breeds Investment. (2001). (18) RePEc:oup:rfinst:v:6:y:1993:i:3:p:473-506 Differences of Opinion Make a Horse Race. (1993). (19) RePEc:oup:rfinst:v:8:y:1995:i:3:p:773-816 Predictable Risk and Returns in Emerging Markets. (1995). (20) RePEc:oup:rfinst:v:15:y:2002:i:4:p:1137-1187 International Asset Allocation With Regime Shifts (2002). (21) RePEc:oup:rfinst:v:14:y:2001:i:1:p:1-27 Learning to be Overconfident. (2001). (22) RePEc:oup:rfinst:v:10:y:1997:i:3:p:661-91 Trade Credit: Theories and Evidence. (1997). (23) RePEc:oup:rfinst:v:1:y:1988:i:4:p:427-445 On Jump Processes in the Foreign Exchange and Stock Markets (1988). (24) RePEc:oup:rfinst:v:5:y:1992:i:1:p:1-33 On the Estimation of Beta-Pricing Models. (1992). (25) RePEc:oup:rfinst:v:3:y:1990:i:2:p:175-205 When Are Contrarian Profits Due to Stock Market Overreaction? (1990). (26) RePEc:oup:rfinst:v:4:y:1991:i:4:p:727-52 Stock Price Distributions with Stochastic Volatility: An Analytic Approach. (1991). (27) RePEc:oup:rfinst:v:7:y:1994:i:4:p:631-51 Transactions, Volume, and Volatility. (1994). (28) RePEc:oup:rfinst:v:9:y:1996:i:1:p:141-61 Dynamic Nonmyopic Portfolio Behavior. (1996). (29) RePEc:oup:rfinst:v:2:y:1989:i:1:p:73-89 Intertemporally Dependent Preferences and the Volatility of Consumption and Wealth. (1989). (30) RePEc:oup:rfinst:v:7:y:1994:i:1:p:125-48 The Value of the Voting Right: A Study of the Milan Stock Exchange Experience. (1994). (31) RePEc:oup:rfinst:v:5:y:1992:i:4:p:531-52 A Theory of the Nominal Term Structure of Interest Rates. (1992). (32) RePEc:oup:rfinst:v:6:y:1993:i:3:p:659-81 The Informational Content of Implied Volatility. (1993). (33) RePEc:oup:rfinst:v:13:y:2000:i:1:p:1-42 Asymmetric Volatility and Risk in Equity Markets. (2000). (34) RePEc:oup:rfinst:v:12:y:1999:i:4:p:653-86 Conflict of Interest and the Credibility of Underwriter Analyst Recommendations. (1999). (35) RePEc:oup:rfinst:v:11:y:1998:i:4:p:817-44 Modeling Asymmetric Comovements of Asset Returns. (1998). (36) RePEc:oup:rfinst:v:11:y:1998:i:2:p:309-41 An Equilibrium Model with Restricted Stock Market Participation. (1998). (37) RePEc:oup:rfinst:v:9:y:1996:i:1:p:37-68 Design and Valuation of Debt Contracts. (1996). (38) RePEc:oup:rfinst:v:15:y:2002:i:1:p:243-288 Quadratic Term Structure Models: Theory and Evidence (2002). (39) RePEc:oup:rfinst:v:6:y:1993:i:4:p:733-64 Auctions of Divisible Goods: On the Rationale for the Treasury Experiment. (1993). (40) RePEc:oup:rfinst:v:13:y:2000:i:2:p:433-51 Recovering Risk Aversion from Option Prices and Realized Returns. (2000). (41) RePEc:oup:rfinst:v:15:y:2002:i:1:p:1-33 Testing Trade-Off and Pecking Order Predictions About Dividends and Debt (2002). (42) RePEc:oup:rfinst:v:3:y:1990:i:1:p:115-31 The Stock Market and Investment. (1990). (43) RePEc:oup:rfinst:v:12:y:1999:i:1:p:197-226 Estimating the Price of Default Risk. (1999). (44) RePEc:oup:rfinst:v:15:y:2002:i:2:p:413-444 Why Dont Issuers Get Upset About Leaving Money on the Table in IPOs? (2002). (45) RePEc:oup:rfinst:v:16:y:2003:i:3:p:717-763 A New Approach to Measuring Financial Contagion (2003). (46) RePEc:oup:rfinst:v:12:y:1999:i:3:p:579-607 Deposits and Relationship Lending. (1999). (47) RePEc:oup:rfinst:v:12:y:1999:i:5:p:975-1007 Stock Market Overreaction to Bad News in Good Times: A Rational Expectations Equilibrium Model. (1999). (48) RePEc:oup:rfinst:v:3:y:1990:i:3:p:431-67 Data-Snooping Biases in Tests of Financial Asset Pricing Models. (1990). (49) RePEc:oup:rfinst:v:6:y:1993:i:2:p:293-326 Forecasting Stock-Return Variance: Toward an Understanding of Stochastic Implied Volatilities. (1993). (50) RePEc:oup:rfinst:v:10:y:1997:i:1:p:205-36 Endogenous Communication among Lenders and Entrepreneurial Incentives. (1997). Recent citations received in: | 2006 | 2005 | 2004 | 2003 Recent citations received in: 2006 (1) RePEc:bca:bocawp:06-45 The Role of Debt and Equity Finance over the Business Cycle (2006). Bank of Canada / Working Papers (2) RePEc:bep:thecon:v:6:y:2006:i:1:p:1253-1253 Multiple Lending and Constrained Efficiency in the Credit Market (2006). Contributions to Theoretical Economics (3) RePEc:cdx:dpaper:2006-05 Uniform price auctions and fixed price offerings in IPOs: an experimental comparison (2006). The Centre for Decision Research and Experimental Economics, School of Economics, University of Nottingham / Discussion Papers (4) RePEc:cpr:ceprdp:5901 Information Acquisition and Portfolio Performance (2006). C.E.P.R. Discussion Papers / CEPR Discussion Papers (5) RePEc:cte:wbrepe:wb063310 CREDIT SPREADS: THEORY AND EVIDENCE ABOUT THE INFORMATION CONTENT OF STOCKS, BONDS AND CDSs (2006). Universidad Carlos III, Departamento de Economía de la Empresa / Business Economics Working Papers (6) RePEc:dgr:kubcen:200667 The impact of organizational structure and lending technology on banking competition (2006). Tilburg University, Center for Economic Research / Discussion Paper (7) RePEc:dgr:kubcen:200668 The impact of competition on bank orientation (2006). Tilburg University, Center for Economic Research / Discussion Paper (8) RePEc:ecb:ecbwps:20060706 What drives investorsâ behaviour in different FX market segments? A VAR-based return decomposition analysis (2006). European Central Bank / Working Paper Series (9) RePEc:fip:fedcwp:0616 Bank branch presence and access to credit in low-to-moderate income neighborhoods (2006). Federal Reserve Bank of Cleveland / Working Paper (10) RePEc:fip:fedcwp:0617 Foreclosures: relationship lending in the consumer market and its aftermath (2006). Federal Reserve Bank of Cleveland / Working Paper (11) RePEc:fip:fedgif:886 Global asset prices and FOMC announcements (2006). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (12) RePEc:fip:fedlwp:2006-047 Does aggregate relative risk aversion change countercyclically over time? evidence from the stock market (2006). Federal Reserve Bank of St. Louis / Working Papers (13) RePEc:fra:franaf:165 Open-End Real Estate Funds in Germany - Genesis and Crisis (2006). Goethe University Frankfurt am Main / Working Paper Series: Finance and Accounting (14) RePEc:hit:hituec:a487 Endogenous Relationship Banking to Alleviate Excessive Screening Transaction Banking (2006). Institute of Economic Research, Hitotsubashi University / Discussion Paper Series (15) RePEc:hst:hstdps:d06-178 Subsampling-Based Tests of Stock-Return Predictability (2006). Institute of Economic Research, Hitotsubashi University / Hi-Stat Discussion Paper Series (16) RePEc:nbr:nberwo:12360 A Skeptical Appraisal of Asset-Pricing Tests (2006). National Bureau of Economic Research, Inc / NBER Working Papers (17) RePEc:nbr:nberwo:12365 Why Has CEO Pay Increased So Much? (2006). National Bureau of Economic Research, Inc / NBER Working Papers (18) RePEc:nbr:nberwo:12555 Financially Constrained Stock Returns (2006). National Bureau of Economic Research, Inc / NBER Working Papers (19) RePEc:nbr:nberwo:12766 Can Housing Collateral Explain Long-Run Swings in Asset Returns? (2006). National Bureau of Economic Research, Inc / NBER Working Papers (20) RePEc:nbr:nberwo:12781 Heterogeneous Expectations and Bond Markets (2006). National Bureau of Economic Research, Inc / NBER Working Papers (21) RePEc:pra:mprapa:247 Risk Premia, diverse belief and beauty contests (2006). University Library of Munich, Germany / MPRA Paper (22) RePEc:rut:rutres:200610 Highs and Lows: A Behavioral and Technical Analysis (2006). Rutgers University, Department of Economics / Departmental Working Papers (23) RePEc:sef:csefwp:167 Information Acquisition and Portfolio Performance (2006). Centre for Studies in Economics and Finance (CSEF), University of Salerno, Italy / CSEF Working Papers Recent citations received in: 2005 (1) RePEc:acb:camaaa:2005-25 THE US TREASURY MARKET IN AUGUST 1998: UNTANGLING THE EFFECTS OG HONG KONG AND RUSSIA WITH HIGH FREQUENCY DATA (2005). Australian National University, Centre for Applied Macroeconomic Analysis / CAMA Working Papers (2) RePEc:bos:macppr:wp2005-005 Capital Structure, Credit Risk, and Macroeconomic Conditions (2005). Department of Economics, Boston University / Boston University Working Papers Series in Macroeconomics (3) RePEc:bro:econwp:2005-06 Future Industrial Organization and Stock Returns versus the Decision to Issue IPOs (2005). Brown University, Department of Economics / Working Papers (4) RePEc:cfs:cfswop:wp200529 Awareness and Stock Market Participation (2005). Center for Financial Studies / CFS Working Paper Series (5) RePEc:cfs:cfswop:wp200533 The Volatility of Realized Volatility (2005). Center for Financial Studies / CFS Working Paper Series (6) RePEc:cla:levrem:172782000000000068 A Theory of Influence: The Strategic Value of Public Ignorance (2005). UCLA Department of Economics / Levine's Bibliography (7) RePEc:cpr:ceprdp:4870 Relational Delegation (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (8) RePEc:cpr:ceprdp:4907 A Theory of Influence: The Strategic Value of Public Ignorance (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (9) RePEc:cpr:ceprdp:5020 The Role of Risk Aversion and Intertemporal Substitution in Dynamic Consumption-Portfolio Choicewith Recursive Utility (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (10) RePEc:cpr:ceprdp:5041 Portfolio Selection with Parameter and Model Uncertainty: A Multi-Prior Approach (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (11) RePEc:cpr:ceprdp:5148 Portfolio Selection with Parameter and Model Uncertainty: A Multi-Prior Approach (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (12) RePEc:cpr:ceprdp:5352 Non-synchronous Trading and Testing for Market Integration in Central European Emerging Markets (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (13) RePEc:cte:wbrepe:wb057718 THE SPEED OF LIMIT ORDER EXECUTION IN THE SPANISH STOCK EXCHANGE (2005). Universidad Carlos III, Departamento de Economía de la Empresa / Business Economics Working Papers (14) RePEc:dgr:uvatin:20050002 Model-based Measurement of Actual Volatility in High-Frequency Data (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (15) RePEc:ecl:ohidic:2004-24 Institutional Investment Constraints and Stock Prices (2005). Ohio State University, Charles A. Dice Center for Research in Financial Economics / Working Paper Series (16) RePEc:fip:fedbwp:05-7 Borrowing costs and the demand for equity over the life cycle (2005). Federal Reserve Bank of Boston / Working Papers (17) RePEc:fip:fedgfe:2005-01 Precautionary savings motives and tax efficiency of household portfolios: an empirical analysis (2005). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (18) RePEc:fip:fedgfe:2005-48 Term structure estimation with survey data on interest rate forecasts (2005). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (19) RePEc:fip:fedgfe:2005-63 Explaining credit default swap spreads with the equity volatility and jump risks of individual firms (2005). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (20) RePEc:fip:fedhwp:wp-05-06 Price discovery in a market under stress: the U.S. Treasury market in fall 1998 (2005). Federal Reserve Bank of Chicago / Working Paper Series (21) RePEc:fip:fedlwp:2005-075 Small caps in international equity portfolios: the effects of variance risk (2005). Federal Reserve Bank of St. Louis / Working Papers (22) RePEc:fip:fednsr:207 The joint dynamics of liquidity, returns, and volatility across small and large firms (2005). Federal Reserve Bank of New York / Staff Reports (23) RePEc:fip:fednsr:216 Arbitrage pricing theory (2005). Federal Reserve Bank of New York / Staff Reports (24) RePEc:fip:fedpwp:05-7 The life-cycle effects of house price changes (2005). Federal Reserve Bank of Philadelphia / Working Papers (25) RePEc:gen:geneem:2005.02 Indirect Robust Estimation of the Short-term Interest Rate Process; (2005). Département d'Econométrie, Université de Genève / Cahiers du Département d'Econométrie (26) RePEc:hhs:cbsfin:2004_011 On a class of adjustable rate mortgage loans subject to a strict balance principle (2005). Copenhagen Business School, Department of Finance / Working Papers (27) RePEc:hhs:gunwpe:0178 The Dark Side of Wage Indexed Pensions (2005). Göteborg University, Department of Economics / Working Papers in Economics (28) RePEc:ivi:wpasec:2005-13 LA INFLUENCIA DEL PODER DE LA DIRECCION EN EL RIESGO Y EN EL VALOR DE LA EMPRESA: EVIDENCIA PARA EL MERCADO ESPAÑOL (2005). Instituto Valenciano de Investigaciones Económicas, S.A. (Ivie) / Working Papers. Serie EC (29) RePEc:iza:izadps:dp1454 Relational Delegation (2005). Institute for the Study of Labor (IZA) / IZA Discussion Papers (30) RePEc:kap:eurfin:v:9:y:2005:i:2:p:165-200 Optimal Liquidity Trading (2005). Review of Finance (31) RePEc:knz:cofedp:0504 Default risk sharing between banks and markets: the contribution of collateralized debt obligations (2005). Center of Finance and Econometrics, University of Konstanz / CoFE Discussion Paper (32) RePEc:nbr:nberte:0319 Edgeworth Expansions for Realized Volatility and Related Estimators (2005). National Bureau of Economic Research, Inc / NBER Technical Working Papers (33) RePEc:nbr:nberwo:11247 Portfolio Choice over the Life-Cycle in the Presence of Trickle Down Labor Income (2005). National Bureau of Economic Research, Inc / NBER Working Papers (34) RePEc:nbr:nberwo:11380 Ultra High Frequency Volatility Estimation with Dependent Microstructure Noise (2005). National Bureau of Economic Research, Inc / NBER Working Papers (35) RePEc:nbr:nberwo:11413 Liquidity and Expected Returns: Lessons From Emerging Markets (2005). National Bureau of Economic Research, Inc / NBER Working Papers (36) RePEc:nbr:nberwo:11426 Investor Competence, Trading Frequency, and Home Bias (2005). National Bureau of Economic Research, Inc / NBER Working Papers (37) RePEc:nbr:nberwo:11534 How Do House Prices Affect Consumption? Evidence From Micro Data (2005). National Bureau of Economic Research, Inc / NBER Working Papers (38) RePEc:nbr:nberwo:11685 The Risk-Adjusted Cost of Financial Distress (2005). National Bureau of Economic Research, Inc / NBER Working Papers (39) RePEc:nbr:nberwo:11741 Default Risk Sharing Between Banks and Markets: The Contribution of Collateralized Debt Obligations (2005). National Bureau of Economic Research, Inc / NBER Working Papers (40) RePEc:nuf:econwp:0505 Estimating quadratic variation when quoted prices jump by a constant increment (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (41) RePEc:oxf:wpaper:225 Security Design in the Real World: Why are Securitization Issues Tranched? (2005). University of Oxford, Department of Economics / Economics Series Working Papers (42) RePEc:pra:mprapa:11974 Empirical comparisons in short-term interest rate models using nonparametric methods (2005). University Library of Munich, Germany / MPRA Paper (43) RePEc:sbs:wpsefe:2005fe04 Why are Securitization Issues Tranched? (2005). Oxford Financial Research Centre / OFRC Working Papers Series (44) RePEc:sbs:wpsefe:2005fe05 Estimating quadratic variation when quoted prices jump by a constant increment (2005). Oxford Financial Research Centre / OFRC Working Papers Series (45) RePEc:sce:scecf5:391 A Malliavin-based Monte-Carlo Approach for Numerical Solution of Stochastic Control Problems: Experiences from Mertons Problem (2005). Society for Computational Economics / Computing in Economics and Finance 2005 (46) RePEc:sce:scecf5:421 Predatory Governance (2005). Society for Computational Economics / Computing in Economics and Finance 2005 (47) RePEc:scp:wpaper:05-9 A Theory of Influence: The Strategic Value of Public Ignorance (2005). Institute of Economic Policy Research (IEPR) / IEPR Working Papers (48) RePEc:siu:wpaper:08-2005 Comments on A Selective Overview of Nonparametric Methods in Financial Econometrics by Jianqing Fan (2005). Singapore Management University, School of Economics / Working Papers (49) RePEc:siu:wpaper:13-2005 Comment on Realized Variance and Market Microstructure Noise by Peter R. Hansen and Asger Lunde (2005). Singapore Management University, School of Economics / Working Papers (50) RePEc:trn:utwpce:0503 Expectations structure in asset pricing experiments (2005). Computable and Experimental Economics Laboratory, Department of Economics, University of Trento, Italia / CEEL Working Papers (51) RePEc:zbw:bubdp1:4224 Ultra high frequency volatility estimation with dependent microstructure noise (2005). Deutsche Bundesbank, Research Centre / Discussion Paper Series 1: Economic Studies Recent citations received in: 2004 (1) RePEc:bca:bocawp:04-17 International Cross-Listing and the Bonding Hypothesis (2004). Bank of Canada / Working Papers (2) RePEc:bep:eapadv:v:4:y:2004:i:1:p:1218-1218 What Do We Know About Cross-subsidization? Evidence from Merging Firms. (2004). Advances in Economic Analysis & Policy (3) RePEc:cir:cirwor:2004s-55 The Determinants of Credit Default Swap Premia (2004). CIRANO / CIRANO Working Papers (4) RePEc:cpr:ceprdp:4182 Awareness and Stock Market Participation (2004). C.E.P.R. Discussion Papers / CEPR Discussion Papers (5) RePEc:ecl:upafin:05-4 Are There Permanent Valuation Gains to Overseas Listing? Evidence from Market Sequencing and Selection (2004). University of Pennsylvania, Wharton School, Weiss Center / Working Papers (6) RePEc:fem:femwpa:2004.150 Quid Pro Quo in IPOs: Why Book-building is Dominating Auctions (2004). Fondazione Eni Enrico Mattei / Working Papers (7) RePEc:fip:feddcl:0304 Why do financial systems differ? History matters (2004). Federal Reserve Bank of Dallas / Center for Latin America Working Papers (8) RePEc:fip:fedgif:815 Look at me now: the role of cross-listing in attracting U.S. investors (2004). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (9) RePEc:fip:fednsr:187 Inference, arbitrage, and asset price volatility (2004). Federal Reserve Bank of New York / Staff Reports (10) RePEc:han:dpaper:dp-308 The Rise of Fund Managers in Foreign Exchange: Will Fundamentals Ultimately Dominate? (2004). Universität Hannover, Wirtschaftswissenschaftliche Fakultät / Diskussionspapiere der Wirtschaftswissenschaftlichen Fakultät der Universität Hanno (11) RePEc:hhs:sifrwp:0031 Dynamic Trading Strategies and Portfolio Choice (2004). Swedish Institute for Financial Research / SIFR Research Report Series (12) RePEc:hhs:sifrwp:0032 The Determinants of Credit Default Swap Premia (2004). Swedish Institute for Financial Research / SIFR Research Report Series (13) RePEc:hit:hitcei:2004-12 Behavioural Biases ofJapanese Institutional Investors; Fund management and Corporate Governance (2004). Institute of Economic Research, Hitotsubashi University / Working Paper Series (14) RePEc:nbr:nberwo:10224 Private Benefits and Cross-Listings in the United States (2004). National Bureau of Economic Research, Inc / NBER Working Papers (15) RePEc:nbr:nberwo:10225 World Markets for Raising New Capital (2004). National Bureau of Economic Research, Inc / NBER Working Papers (16) RePEc:nbr:nberwo:10820 Dynamic Trading Strategies and Portfolio Choice (2004). National Bureau of Economic Research, Inc / NBER Working Papers (17) RePEc:nbr:nberwo:10937 Patterns of Comovement: The Role of Information Technology in the U.S. Economy (2004). National Bureau of Economic Research, Inc / NBER Working Papers (18) RePEc:nbr:nberwo:11004 Do Liquidation Values Affect Financial Contracts? Evidence from Commercial Loan Contracts and Zoning Regulation (2004). National Bureau of Economic Research, Inc / NBER Working Papers (19) RePEc:nbr:nberwo:11006 Bank Mergers and Crime: The Real and Social Effects of Credit Market Competition (2004). National Bureau of Economic Research, Inc / NBER Working Papers (20) RePEc:rif:dpaper:950 Mandatory Auditor Choice and Small Finance: Evidence from Finland (2004). The Research Institute of the Finnish Economy / Discussion Papers (21) RePEc:sef:csefwp:125 The Distribution of Gains from Access to Stocks (2004). Centre for Studies in Economics and Finance (CSEF), University of Salerno, Italy / CSEF Working Papers (22) RePEc:wpa:wuwpfi:0407014 Investment, Hedging, and Consumption Smoothing (2004). EconWPA / Finance Recent citations received in: 2003 (1) RePEc:cpr:ceprdp:4091 Does Anonymity Matter in Electronic Limit Order Markets? (2003). C.E.P.R. Discussion Papers / CEPR Discussion Papers (2) RePEc:eap:articl:v:33:y:2003:i:2:p:293-306 Taxing International Financial Institutions (2003). Economic Analysis and Policy (EAP) (3) RePEc:ebg:heccah:0784 Does anonymity matter in electronic limit order markets ? (2003). Groupe HEC / Les Cahiers de Recherche (4) RePEc:ecb:ecbwps:20030297 Measurement of contagion in banksâ equity prices. (2003). European Central Bank / Working Paper Series (5) RePEc:ibm:finlab:flwp_49 Evaluating an Alternative Risk Preference in Affine Term Structure Models (2003). Finance Lab, Ibmec São Paulo / Finance Lab Working Papers (6) RePEc:imf:imfwpa:03/84 Unanticipated Shocks and Systemic Influences: The Impact of Contagion in Global Equity Markets in 1998 (2003). International Monetary Fund / IMF Working Papers (7) RePEc:nbr:nberwo:9674 Diversification and the Taxation of Capital Gains and Losses (2003). National Bureau of Economic Research, Inc / NBER Working Papers (8) RePEc:nbr:nberwo:9995 Appearing and Disappearing Dividends: The Link to Catering Incentives (2003). National Bureau of Economic Research, Inc / NBER Working Papers (9) RePEc:wbk:wbrwps:3103 Ownership structure and initial public offerings (2003). The World Bank / Policy Research Working Paper Series Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||