|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

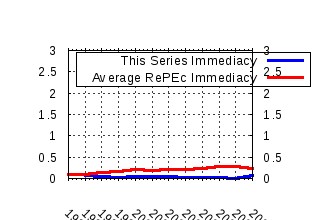

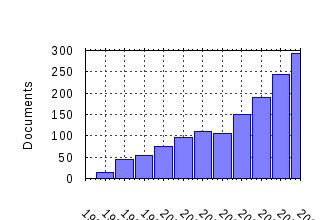

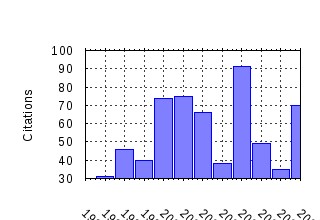

arXiv.org / Quantitative Finance Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:arx:papers:cond-mat/9804100 Universal features in the growth dynamics of complex organizations (1998). (2) RePEc:arx:papers:cond-mat/0106520 Significance of log-periodic precursors to financial crashes (2001). (3) RePEc:arx:papers:cond-mat/9907161 Scaling of the distribution of price fluctuations of individual

companies (1999). (4) RePEc:arx:papers:0708.2090 The Product Space Conditions the Development of Nations (2007). (5) RePEc:arx:papers:cond-mat/9705087 Scaling in stock market data: stable laws and beyond (1997). (6) RePEc:arx:papers:cond-mat/0311053 The long memory of the efficient market (2004). (7) RePEc:arx:papers:physics/0512005 The Growth of Business Firms: Theoretical Framework and Empirical

Evidence (2005). (8) RePEc:arx:papers:cond-mat/9905305 Scaling of the distribution of fluctuations of financial market indices (1999). (9) RePEc:arx:papers:cond-mat/9702082 Scaling behavior in economics: I. Empirical results for company growth (1997). (10) RePEc:arx:papers:cond-mat/0008113 Statistical Properties of Share Volume Traded in Financial Markets (2000). (11) RePEc:arx:papers:cond-mat/0401300 Networks of equities in financial markets (2004). (12) RePEc:arx:papers:cond-mat/0004263 The Nasdaq crash of April 2000: Yet another example of log-periodicity

in a speculative bubble ending in a crash (2000). (13) RePEc:arx:papers:cond-mat/0006454 Fractional calculus and continuous-time finance II: the waiting-time

distribution (2000). (14) RePEc:arx:papers:math/0405293 Optimal investment with random endowments in incomplete markets (2004). (15) RePEc:arx:papers:physics/0502066 Structure and Evolution of the World Trade Network (2005). (16) RePEc:arx:papers:cond-mat/0312703 What really causes large price changes? (2004). (17) RePEc:arx:papers:cond-mat/0202527 Volatility in Financial Markets: Stochastic Models and Empirical Results (2002). (18) RePEc:arx:papers:0708.1756 Optimal execution strategies in limit order books with general shape

functions (2007). (19) RePEc:arx:papers:cond-mat/0310061 Do Pareto-Zipf and Gibrat laws hold true? An analysis with European

Firms (2003). (20) RePEc:arx:papers:cond-mat/0401225 Exponential distribution of financial returns at mesoscopic time lags: a

new stylized fact (2004). (21) RePEc:arx:papers:cond-mat/9709118 A Prototype Model of Stock Exchange (1997). (22) RePEc:arx:papers:cond-mat/0104341 A Nonlinear Super-Exponential Rational Model of Speculative Financial

Bubbles (2002). (23) RePEc:arx:papers:cond-mat/0403051 Fitness-dependent topological properties of the World Trade Web (2004). (24) RePEc:arx:papers:cond-mat/9903369 The statistical properties of the volatility of price fluctuations (1999). (25) RePEc:arx:papers:cond-mat/0203046 Probability distribution of returns in the Heston model with stochastic

volatility (2002). (26) RePEc:arx:papers:cond-mat/0103544 Exponential and power-law probability distributions of wealth and income

in the United Kingdom and the United States (2001). (27) RePEc:arx:papers:cond-mat/0301543 Critical Market Crashes (2003). (28) RePEc:arx:papers:cond-mat/0104295 On the coherence of Expected Shortfall (2002). (29) RePEc:arx:papers:cond-mat/0106114 Analyzing and modelling 1+1d markets (2001). (30) RePEc:arx:papers:cond-mat/0004256 Statistical mechanics of money: How saving propensity affects its

distribution (2000). (31) RePEc:arx:papers:cond-mat/0012419 The price dynamics of common trading strategies (2000). (32) RePEc:arx:papers:cond-mat/0106657 Quantifying Stock Price Response to Demand Fluctuations (2001). (33) RePEc:arx:papers:cond-mat/0208514 Theoretical Analysis and Simulations of the Generalized Lotka-Volterra

Model (2002). (34) RePEc:arx:papers:cond-mat/0002438 Symmetry alteration of ensemble return distribution in crash and rally

days of financial markets (2000). (35) RePEc:arx:papers:cond-mat/0209065 The US 2000-2002 Market Descent: How Much Longer and Deeper? (2002). (36) RePEc:arx:papers:cond-mat/9909265 Modeling Market Mechanism with Minority Game (1999). (37) RePEc:arx:papers:cond-mat/9702085 Scaling behavior in economics: II. Modeling of company growth (1997). (38) RePEc:arx:papers:cond-mat/9901035 Critical Crashes (1999). (39) RePEc:arx:papers:nlin/0108022 Forecasting Portfolio Risk in Normal and Stressed Markets (2001). (40) RePEc:arx:papers:0706.0474 Stability of utility-maximization in incomplete markets (2007). (41) RePEc:arx:papers:physics/0701140 Agent-based Models of Financial Markets (2007). (42) RePEc:arx:papers:cond-mat/0209475 A theory for Fluctuations in Stock Prices and Valuation of their Options (2002). (43) RePEc:arx:papers:cond-mat/0102423 Power Laws of Wealth, Market Order Volumes and Market Returns (2001). (44) RePEc:arx:papers:cond-mat/9901268 Financial ``Anti-Bubbles: Log-Periodicity in Gold and Nikkei collapses (1999). (45) RePEc:arx:papers:cond-mat/0108033 Measuring Anti-Correlations in the Nordic Electricity Spot Market by

Wavelets (2003). (46) RePEc:arx:papers:cond-mat/9801240 Optimal Investment Strategy for Risky Assets (1998). (47) RePEc:arx:papers:0811.2125 GDP growth rate and population (2008). (48) RePEc:arx:papers:cond-mat/0102305 From Rational Bubbles to Crashes (2001). (49) RePEc:arx:papers:cond-mat/0001353 Thermometers of Speculative Frenzy (2000). (50) RePEc:arx:papers:cond-mat/9801209 Rational Decisions, Random Matrices and Spin Glasses (1998). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:aah:create:2007-43 Microstructure Noise in the Continuous Case: The Pre-Averaging Approach - JLMPV-9 (2007). School of Economics and Management, University of Aarhus / CREATES Research Papers (2) RePEc:ams:ndfwpp:07-14 Asset Prices, Traders Behavior, and Market Design (2007). Universiteit van Amsterdam, Center for Nonlinear Dynamics in Economics and Finance / CeNDEF Working Papers (3) RePEc:arx:papers:0709.3005 Feedback and efficiency in limit order markets (2007). arXiv.org / Quantitative Finance Papers (4) RePEc:arx:papers:0710.0459 Statistical properties of agent-based market area model (2007). arXiv.org / Quantitative Finance Papers (5) RePEc:arx:papers:0710.2402 Intraday pattern in bid-ask spreads and its power-law relaxation for Chinese A-share stocks (2007). arXiv.org / Quantitative Finance Papers (6) RePEc:arx:papers:0710.5497 Multifractality in the Random Parameters Model (2007). arXiv.org / Quantitative Finance Papers (7) RePEc:arx:papers:0711.1595 Likelihood-based inference for correlated diffusions (2007). arXiv.org / Quantitative Finance Papers (8) RePEc:arx:papers:0712.1275 Continuous-time trading and emergence of randomness (2007). arXiv.org / Quantitative Finance Papers (9) RePEc:arx:papers:0712.1483 Continuous-time trading and emergence of volatility (2007). arXiv.org / Quantitative Finance Papers (10) RePEc:pra:mprapa:2128 Fokker-Planck and Chapman-Kolmogorov equations for Ito processes with finite memory (2007). University Library of Munich, Germany / MPRA Paper (11) RePEc:pra:mprapa:2256 Martingales, Detrending Data, and the Efficient Market Hypothesis (2007). University Library of Munich, Germany / MPRA Paper (12) RePEc:pra:mprapa:5075 Optimal Portfolio Liquidation for CARA Investors (2007). University Library of Munich, Germany / MPRA Paper (13) RePEc:pra:mprapa:5303 Martingales, the efficient market hypothesis, and spurious stylized facts (2007). University Library of Munich, Germany / MPRA Paper (14) RePEc:pra:mprapa:5548 Liquidation in the Face of Adversity: Stealth Vs. Sunshine Trading, Predatory Trading Vs. Liquidity Provision (2007). University Library of Munich, Germany / MPRA Paper (15) RePEc:pra:mprapa:5811 Ito Processes with Finitely Many States of Memory (2007). University Library of Munich, Germany / MPRA Paper (16) RePEc:pra:mprapa:5813 Empirically Based Modeling in the Social Sciences and Spurious Stylized Facts (2007). University Library of Munich, Germany / MPRA Paper (17) RePEc:pra:mprapa:5996 International Trade Patterns over the Last Four Decades: How does Portugal Compare with other Cohesion Countries? (2007). University Library of Munich, Germany / MPRA Paper (18) RePEc:spr:jeicoo:v:2:y:2007:i:2:p:111-124 Patterns of dominant flows in the world trade web (2007). Journal of Economic Interaction and Coordination (19) RePEc:ssa:lemwps:2007/25 Using Complex Network Analysis to Assess the Evolution of International Economic Integration: The cases of East Asia and Latin America (2007). Laboratory of Economics and Management (LEM), Sant'Anna School of Advanced Studies, Pisa, Italy / LEM Papers Series Recent citations received in: 2006 (1) RePEc:arx:papers:math/0612649 General Duality for Perpetual American Options (2006). arXiv.org / Quantitative Finance Papers (2) RePEc:arx:papers:physics/0508156 Size matters: some stylized facts of the stock market revisited (2006). arXiv.org / Quantitative Finance Papers (3) RePEc:pra:mprapa:73 The Distribution of Model Averaging Estimators and an Impossibility Result Regarding Its Estimation (2006). University Library of Munich, Germany / MPRA Paper Recent citations received in: 2005 (1) RePEc:arx:papers:physics/0504197 The Rich Are Different!: Pareto Law from asymmetric interactions in asset exchange models (2005). arXiv.org / Quantitative Finance Papers (2) RePEc:arx:papers:physics/0507136 Ideal-Gas Like Markets: Effect of Savings (2005). arXiv.org / Quantitative Finance Papers (3) RePEc:taf:quantf:v:5:y:2005:i:6:p:519-521 Two phase behaviour and the distribution of volume (2005). Quantitative Finance (4) RePEc:wpa:wuwpfi:0506015 Using Hermite Expansions for Fast and Arbitrarily Accurate Computation of the Expected Loss of a Loan Portfolio Tranche in the Gaussian Factor Model (2005). EconWPA / Finance (5) RePEc:wpa:wuwpri:0507004 Fast Computation of the Economic Capital, the Value at Risk and the Greeks of a Loan Portfolio in the Gaussian Factor Model (2005). EconWPA / Risk and Insurance Recent citations received in: 2004 (1) RePEc:arx:papers:cond-mat/0408013 Stock Price Clustering and Discreteness: The Compass Rose and Predictability (2004). arXiv.org / Quantitative Finance Papers (2) RePEc:pra:mprapa:2240 What Economists can learn from physics and finance (2004). University Library of Munich, Germany / MPRA Paper (3) RePEc:sfi:sfiwpa:500063 Random walks, liquidity molasses and critical response in financial markets (2004). Science & Finance, Capital Fund Management / Science & Finance (CFM) working paper archive Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||