|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

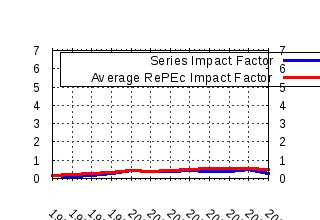

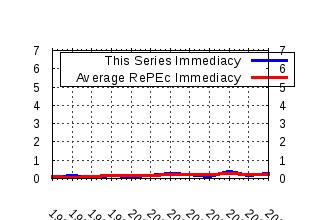

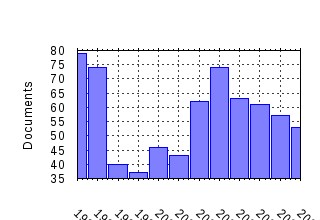

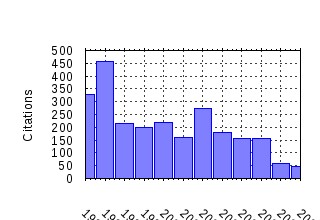

Econometric Theory Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:cup:etheor:v:11:y:1995:i:01:p:122-150_00 Multivariate Simultaneous Generalized ARCH (1995). (2) RePEc:cup:etheor:v:13:y:1997:i:05:p:747-754_00 Econometric Analysis of Panel Data (1997). (3) RePEc:cup:etheor:v:12:y:1996:i:04:p:657-681_00 Which Moments to Match? (1996). (4) RePEc:cup:etheor:v:12:y:1996:i:4:p:657-81 Which Moments to Match? (). (5) RePEc:cup:etheor:v:11:y:1995:i:1:p:122-50 Multivariate Simultaneous Generalized ARCH. (). (6) RePEc:cup:etheor:v:12:y:1996:i:03:p:409-431_00 Markov Chain Monte Carlo Simulation Methods in Econometrics (1996). (7) RePEc:cup:etheor:v:13:y:1997:i:03:p:315-352_00 Estimating Multiple Breaks One at a Time (1997). (8) RePEc:cup:etheor:v:19:y:2003:i:02:p:280-310_19 ASYMPTOTIC THEORY FOR A VECTOR ARMA-GARCH MODEL (2003). (9) RePEc:cup:etheor:v:7:y:1991:i:01:p:1-21_00 Asymptotically Efficient Estimation of Cointegration Regressions (1991). (10) RePEc:cup:etheor:v:20:y:2004:i:03:p:597-625_20 PANEL COINTEGRATION: ASYMPTOTIC AND FINITE SAMPLE PROPERTIES OF POOLED TIME SERIES TESTS WITH AN APPLICATION TO THE PPP HYPOTHESIS (2004). (11) RePEc:cup:etheor:v:13:y:1997:i:06:p:808-817_00 Optimal Prediction Under Asymmetric Loss (1997). (12) RePEc:cup:etheor:v:12:y:1996:i:3:p:409-31 Markov Chain Monte Carlo Simulation Methods in Econometrics. (). (13) RePEc:cup:etheor:v:13:y:1997:i:3:p:315-52 Estimating Multiple Breaks One at a Time. (). (14) RePEc:cup:etheor:v:11:y:1995:i:05:p:1131-1147_00 Inference in Models with Nearly Integrated Regressors (1995). (15) RePEc:cup:etheor:v:10:y:1994:i:01:p:29-52_00 Asymptotic Theory for the Garch(1,1) Quasi-Maximum Likelihood Estimator (1994). (16) RePEc:cup:etheor:v:13:y:1997:i:6:p:808-17 Optimal Prediction under Asymmetric Loss. (). (17) RePEc:cup:etheor:v:10:y:1994:i:01:p:91-115_00 A Residual-Based Test of the Null of Cointegration Against the Alternative of No Cointegration (1994). (18) RePEc:cup:etheor:v:11:y:1995:i:5:p:1131-47 Inference in Models with Nearly Integrated Regressors. (). (19) RePEc:cup:etheor:v:18:y:2002:i:01:p:17-39_18 MIXING AND MOMENT PROPERTIES OF VARIOUS GARCH AND STOCHASTIC VOLATILITY MODELS (2002). (20) RePEc:cup:etheor:v:15:y:1999:i:04:p:549-582_15 THE NONSTATIONARY FRACTIONAL UNIT ROOT (1999). (21) RePEc:cup:etheor:v:7:y:1991:i:1:p:1-21 Asymptotically Efficient Estimation of Cointegration Regressions. (). (22) RePEc:cup:etheor:v:11:y:1995:i:05:p:1148-1171_00 Rethinking the Univariate Approach to Unit Root Testing: Using Covariates to Increase Power (1995). (23) RePEc:cup:etheor:v:10:y:1994:i:1:p:95-115 A Residual-Based Test of the Null of Cointegration against the Alternative of No Cointegration. (). (24) RePEc:cup:etheor:v:14:y:1998:i:01:p:70-86_14 STRONG CONSISTENCY OF ESTIMATORS FOR MULTIVARIATE ARCH MODELS (1998). (25) RePEc:cup:etheor:v:15:y:1999:i:03:p:269-298_15 ASYMPTOTICS FOR NONLINEAR TRANSFORMATIONS OF INTEGRATED TIME SERIES (1999). (26) RePEc:cup:etheor:v:17:y:2001:i:04:p:686-710_17 ON THE LOG PERIODOGRAM REGRESSION ESTIMATOR OF THE MEMORY PARAMETER IN LONG MEMORY STOCHASTIC VOLATILITY MODELS (2001). (27) RePEc:cup:etheor:v:18:y:2002:i:03:p:722-729_18 NECESSARY AND SUFFICIENT MOMENT CONDITIONS FOR THE GARCH(r,s) AND ASYMMETRIC POWER GARCH(r,s) MODELS (2002). (28) RePEc:cup:etheor:v:17:y:2001:i:06:p:1113-1141_17 THE GENERALIZED DYNAMIC FACTOR MODEL: REPRESENTATION THEORY (2001). (29) RePEc:cup:etheor:v:11:y:1995:i:03:p:530-536_00 Causality in the Long Run (1995). (30) RePEc:cup:etheor:v:9:y:1993:i:02:p:222-240_00 Testing Identifiability and Specification in Instrumental Variable Models (1993). (31) RePEc:cup:etheor:v:11:y:1995:i:5:p:1148-71 Rethinking the Univariate Approach to Unit Root Testing: Using Covariates to Increase Power. (). (32) RePEc:cup:etheor:v:14:y:1998:i:06:p:783-793_14 A NOTE ON THE CONVERGENCE OF NONPARAMETRIC DEA ESTIMATORS FOR PRODUCTION EFFICIENCY SCORES (1998). (33) RePEc:cup:etheor:v:15:y:1999:i:03:p:361-376_15 THE SIZE DISTORTION OF BOOTSTRAP TESTS (1999). (34) RePEc:cup:etheor:v:11:y:1995:i:03:p:560-586_00 Nonparametric Kernel Estimation for Semiparametric Models (1995). (35) RePEc:cup:etheor:v:13:y:1997:i:06:p:818-848_00 Wald-Type Tests for Detecting Breaks in the Trend Function of a Dynamic Time Series (1997). (36) RePEc:cup:etheor:v:14:y:1998:i:03:p:295-325_14 CONSISTENT SPECIFICATION TESTING WITH NUISANCE PARAMETERS PRESENT ONLY UNDER THE ALTERNATIVE (1998). (37) RePEc:cup:etheor:v:8:y:1992:i:4:p:489-500 Convergence to Stochastic Integrals for Dependent Heterogeneous Processes. (). (38) RePEc:cup:etheor:v:21:y:2005:i:01:p:232-261_05 AUTOMATED INFERENCE AND LEARNING IN MODELING FINANCIAL VOLATILITY (2005). (39) RePEc:cup:etheor:v:10:y:1994:i:05:p:849-866_00 Testing for Second-Order Stochastic Dominance of Two Distributions (1994). (40) RePEc:cup:etheor:v:17:y:2001:i:02:p:451-470_17 ASYMPTOTIC PROPERTIES OF WEIGHTED M-ESTIMATORS FOR STANDARD STRATIFIED SAMPLES (2001). (41) RePEc:cup:etheor:v:11:y:1995:i:05:p:984-1014_00 Testing for Cointegration When Some of the Cointegrating Vectors are Prespecified (1995). (42) RePEc:cup:etheor:v:8:y:1992:i:1:p:1-27 Estimation and Testing of Cointegrated Systems by an Autoregressive Approximation. (). (43) RePEc:cup:etheor:v:20:y:2004:i:05:p:813-843_20 INSTRUMENTAL VARIABLE ESTIMATION OF A THRESHOLD MODEL (2004). (44) RePEc:cup:etheor:v:16:y:2000:i:02:p:176-199_16 TESTS OF COMMON STOCHASTIC TRENDS (2000). (45) RePEc:cup:etheor:v:11:y:1995:i:02:p:359-368_00 An LM Test for a Unit Root in the Presence of a Structural Change (1995). (46) RePEc:cup:etheor:v:19:y:2003:i:02:p:254-279_19 MULTISTEP PREDICTION IN AUTOREGRESSIVE PROCESSES (2003). (47) RePEc:cup:etheor:v:14:y:1998:i:02:p:222-259_14 TESTS FOR STRUCTURAL CHANGE IN COINTEGRATED SYSTEMS (1998). (48) RePEc:cup:etheor:v:10:y:1994:i:02:p:1-21_00 Kernel Estimation of Partial Means and a General Variance Estimator (1994). (49) RePEc:cup:etheor:v:10:y:1994:i:3-4:p:774-808_00 Posterior Odds Testing for a Unit Root with Data-Based Model Selection (1994). (50) RePEc:cup:etheor:v:11:y:1995:i:3:p:530-36 Causality in the Long Run. (). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:aah:aarhec:2007-16 A Statistical Programme Assignment Model (2007). Department of Economics, University of Aarhus / Department of Economics, Working Papers (2) RePEc:cmf:wpaper:wp2007_0713 ON THE EFFICIENCY AND CONSISTENCY OF LIKELIHOOD ESTIMATION IN MULTIVARIATE CONDITIONALLY HETEROSKEDASTIC DYNAMIC REGRESSION MODELS (2007). CEMFI / Working Papers (3) RePEc:ctl:louvec:2007033 Theory and inference for a Markov switching GARCH model (2007). Université catholique de Louvain, Département des Sciences Economiques / Université catholique de Louvain, Département des Sciences Economiques Workin (4) RePEc:cwl:cwldpp:1595 Transition Modeling and Econometric Convergence Tests (2007). Cowles Foundation, Yale University / Cowles Foundation Discussion Papers (5) RePEc:hhs:osloec:2007_010 Long-term Outcomes of Vocational Rehabilitation Programs: Labor Market Transitions and Job Durations for Immigrants (2007). Oslo University, Department of Economics / Memorandum (6) RePEc:hhs:osloec:2007_013 Unemployment Insurance in Welfare States: Soft Constraints and Mild Sanctions (2007). Oslo University, Department of Economics / Memorandum (7) RePEc:iea:carech:0709 Theory and inference for a Markov switching Garch model. (2007). HEC Montréal, Institut d'économie appliquée / Cahiers de recherche (8) RePEc:inu:caeprp:2007019 Detecting Misspecifications in Autoregressive Conditional Duration Models (2007). Center for Applied Economics and Policy Research, Economics Department, Indiana University Bloomington / Caepr Working Papers (9) RePEc:iza:izadps:dp2877 Unemployment Insurance in Welfare States: Soft Constraints and Mild Sanctions (2007). Institute for the Study of Labor (IZA) / IZA Discussion Papers (10) RePEc:iza:izadps:dp3165 A Statistical Programme Assignment Model (2007). Institute for the Study of Labor (IZA) / IZA Discussion Papers (11) RePEc:lvl:lacicr:0733 Theory and Inference for a Markov-Switching GARCH Model (2007). (12) RePEc:pra:mprapa:11980 Specification testing in discretized diffusion models: Theory and practice (2007). University Library of Munich, Germany / MPRA Paper (13) RePEc:pra:mprapa:2744 A Gravity approach to evaluate the significance of trade liberalization in vertically-related goods in the presence of non-tariff barriers (2007). University Library of Munich, Germany / MPRA Paper Recent citations received in: 2006 (1) RePEc:cor:louvco:2006042 Deciding between GARCH and stochastic volatility via strong decision rules (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (2) RePEc:cor:louvco:2006068 A GARCH (1,1) estimator with (almost) no moment conditions on the error term (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (3) RePEc:cor:louvco:2006071 Asymptotic theory for a factor GARCH model (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (4) RePEc:cwl:cwldpp:1594 Asymptotic Theory for Local Time Density Estimation and Nonparametric Cointegrating Regression (2006). Cowles Foundation, Yale University / Cowles Foundation Discussion Papers (5) RePEc:dgr:uvatin:20060078 The Asymptotic and Finite Sample Distributions of OLS and Simple IV in Simultaneous Equations (2006). Tinbergen Institute / Tinbergen Institute Discussion Papers (6) RePEc:hum:wpaper:sfb649dp2006-012 Bootstrapping Systems Cointegration Tests with a Prior Adjustment for Deterministic Terms (2006). Sonderforschungsbereich 649, Humboldt University, Berlin, Germany / SFB 649 Discussion Papers (7) RePEc:msh:ebswps:2006-20 Tests for Over-identifying Restrictions in Partially Identified Linear Structural Equations (2006). Monash University, Department of Econometrics and Business Statistics / Monash Econometrics and Business Statistics Working Papers (8) RePEc:qed:wpaper:1029 Determining the Cointegrating Rank in Nonstationary Fractional Systems by the Exact Local Whittle Approach (2006). Queen's University, Department of Economics / Working Papers (9) RePEc:qed:wpaper:1101 Simple (but effective) tests of long memory versus structural breaks (2006). Queen's University, Department of Economics / Working Papers Recent citations received in: 2005 (1) RePEc:ags:aaea05:19558 In Search of the Bank Lending Channel: Causality Analysis for the Transmission Mechanism of U.S. Monetary Policy (2005). American Agricultural Economics Association (New Name 2008: Agricultural and Applied Economics Association) / 2005 Annual meeting, July 24-27, Provide (2) RePEc:bfr:banfra:122 Break in the Mean and Persistence of Inflation: a Sectoral Analysis of French CPI. (2005). Banque de France / Documents de Travail (3) RePEc:bri:uobdis:05/580 What determines financial development? (2005). Department of Economics, University of Bristol, UK / Bristol Economics Discussion Papers (4) RePEc:cfr:cefirw:w0069 Optimal Instruments in Time Series: A Survey (2005). Center for Economic and Financial Research / CEFIR Working Papers (5) RePEc:cpr:ceprdp:5279 Model Averaging and Value-at-Risk Based Evaluation of Large Multi-Asset Volatility Models for Risk Management (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (6) RePEc:ecb:ecbwps:20050463 Break in the mean and persistence of inflation - a sectoral analysis of French CPI (2005). European Central Bank / Working Paper Series (7) RePEc:eui:euiwps:eco2005/09 Autoregressive Approximations of Multiple Frequency I(1) Processes (2005). European University Institute / Economics Working Papers (8) RePEc:han:dpaper:dp-327 Empirical likelihood confidence intervals for the mean of a long-range dependent process (2005). Universität Hannover, Wirtschaftswissenschaftliche Fakultät / Diskussionspapiere der Wirtschaftswissenschaftlichen Fakultät der Universität Hanno (9) RePEc:hhs:rbnkwp:0189 Bayesian Inference of General Linear Restrictions on the Cointegration Space (2005). Sveriges Riksbank (Central Bank of Sweden) / Working Paper Series (10) RePEc:ifs:cemmap:13/05 Weak instruments and empirical likelihood: a discussion of the papers by DWK Andrews and JH Stock and Y Kitamura (2005). Centre for Microdata Methods and Practice, Institute for Fiscal Studies / CeMMAP working papers (11) RePEc:ifs:cemmap:18/05 GMM with many weak moment conditions (2005). Centre for Microdata Methods and Practice, Institute for Fiscal Studies / CeMMAP working papers (12) RePEc:ihs:ihsesp:174 Autoregressive Approximations of Multiple Frequency I(1) Processes (2005). Institute for Advanced Studies / Economics Series (13) RePEc:mlb:wpaper:949 Computing the Distributions of Economic Models Via Simulation (2005). The University of Melbourne / Department of Economics - Working Papers Series (14) RePEc:scp:wpaper:05-33 Why Panel Data? (2005). Institute of Economic Policy Research (IEPR) / IEPR Working Papers (15) RePEc:taf:applec:v:37:y:2005:i:20:p:2335-2347 Testing mean reversion in target-zone exchange rates (2005). Applied Economics (16) RePEc:tcb:wpaper:0501 A Dynamic Model of Central Bank Intervention (2005). Research and Monetary Policy Department, Central Bank of the Republic of Turkey / Working Papers (17) RePEc:ubi:deawps:11 Managing Value-at-Risk in Daily Tourist Tax Revenues for the Maldives (2005). Universitat de les Illes Balears, Departament d'EconomÃa Aplicada / DEA Working Papers (18) RePEc:ubi:deawps:12 Asymmetric Multivariate Stochastic Volatility (2005). Universitat de les Illes Balears, Departament d'EconomÃa Aplicada / DEA Working Papers (19) RePEc:ubi:deawps:14 Measuring the Volatility in U.S. Treasury Benchmarks and Debt Instruments (2005). Universitat de les Illes Balears, Departament d'EconomÃa Aplicada / DEA Working Papers (20) RePEc:wpa:wuwpem:0503014 Powerful and Serial Correlation Robust Tests of the Economic Convergence Hypothesis (2005). EconWPA / Econometrics (21) RePEc:wpa:wuwpem:0510005 What Happens to Japan if China Catches Cold? - A causal analysis of the Chinese growth and the Japanese growth (2005). EconWPA / Econometrics (22) RePEc:wpa:wuwpif:0503006 Are Exchange Rates Really Random Walks? Some Evidence Robust to Parameter Instability (2005). EconWPA / International Finance Recent citations received in: 2004 (1) RePEc:cwl:cwldpp:1453 Smoothed Empirical Likelihood Methods for Quantile Regression Models (2004). Cowles Foundation, Yale University / Cowles Foundation Discussion Papers (2) RePEc:cwl:cwldpp:1473 Regression Asymptotics Using Martingale Convergence Methods (2004). Cowles Foundation, Yale University / Cowles Foundation Discussion Papers (3) RePEc:ecm:feam04:512 Bagging Binary Predictors for Time Series (2004). Econometric Society / Econometric Society 2004 Far Eastern Meetings (4) RePEc:ecm:feam04:749 Testing for Nonlinear Adjustment in Smooth Transition Vector Error Correction Models (2004). Econometric Society / Econometric Society 2004 Far Eastern Meetings (5) RePEc:eui:euiwps:eco2004/29 Efficient Tests of the Seasonal Unit Root Hypothesis (2004). European University Institute / Economics Working Papers (6) RePEc:ila:anaeco:v:19:y:2004:i:2:p:41-83 Real exchange rates in the long and short run: a panel co-integration approach (2004). Revista de Analisis Economico (7) RePEc:lsu:lsuwpp:2004-03 International Medical R&D Spillovers (2004). Department of Economics, Louisiana State University / Departmental Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||