|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

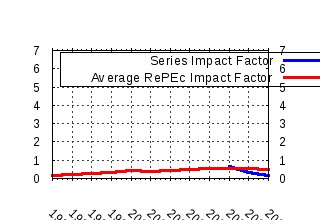

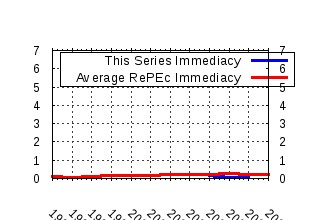

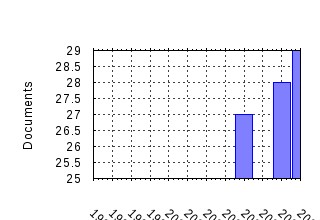

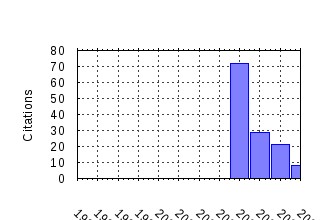

Finance Research Letters Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:finlet:v:1:y:2004:i:1:p:11-23 Asymmetric information, bank lending and implicit contracts: the winners curse (2004). (2) RePEc:eee:finlet:v:1:y:2004:i:1:p:24-34 Limited stock market participation and the equity premium (2004). (3) RePEc:eee:finlet:v:1:y:2004:i:2:p:85-89 Maximizing the expected net future value as an alternative strategy to gamma discounting (2004). (4) RePEc:eee:finlet:v:1:y:2004:i:1:p:56-73 On more robust estimation of skewness and kurtosis (2004). (5) RePEc:eee:finlet:v:1:y:2004:i:4:p:215-225 Reported and secret interventions in the foreign exchange markets (2004). (6) RePEc:eee:finlet:v:2:y:2005:i:4:p:185-194 The long-run equity risk premium (2005). (7) RePEc:eee:finlet:v:3:y:2006:i:3:p:212-233 The interaction between technical currency trading and exchange rate fluctuations (2006). (8) RePEc:eee:finlet:v:2:y:2005:i:1:p:1-14 tays as good as cay (2005). (9) RePEc:eee:finlet:v:2:y:2005:i:1:p:15-22 tays as good as cay: Reply (2005). (10) RePEc:eee:finlet:v:2:y:2005:i:4:p:210-226 Solving models with external habit (2005). (11) RePEc:eee:finlet:v:3:y:2006:i:2:p:154-162 Explosive bubbles in the cointegrated VAR model (2006). (12) RePEc:eee:finlet:v:5:y:2008:i:2:p:79-87 Option prices as probabilities (2008). (13) RePEc:eee:finlet:v:1:y:2004:i:4:p:226-235 Optimal investment with fixed financing costs (2004). (14) RePEc:eee:finlet:v:3:y:2006:i:2:p:114-132 Modeling dynamic conditional correlations in WTI oil forward and futures returns (2006). (15) RePEc:eee:finlet:v:1:y:2004:i:3:p:178-189 Institutional trading and stock returns (2004). (16) RePEc:eee:finlet:v:4:y:2007:i:3:p:137-145 Optimality of the RiskMetrics VaR model (2007). (17) RePEc:eee:finlet:v:4:y:2007:i:1:p:2-9 Pitfalls in static superhedging of barrier options (2007). (18) RePEc:eee:finlet:v:1:y:2004:i:1:p:47-55 The effect of market conditions on capital structure adjustment (2004). (19) RePEc:eee:finlet:v:2:y:2005:i:4:p:260-269 The price-dividend relationship in inflationary and deflationary regimes (2005). (20) RePEc:eee:finlet:v:2:y:2005:i:2:p:75-88 Another look at the relationship between cross-market correlation and volatility (2005). (21) RePEc:eee:finlet:v:2:y:2005:i:4:p:227-233 Financial forecasts in the presence of asymmetric loss aversion, skewness and excess kurtosis (2005). (22) RePEc:eee:finlet:v:3:y:2006:i:2:p:96-101 Asset trading volume in infinite-horizon economies with dynamically complete markets and heterogeneous agents: Comment (2006). (23) RePEc:eee:finlet:v:3:y:2006:i:4:p:277-289 Quadratic term structure models in discrete time (2006). (24) RePEc:eee:finlet:v:5:y:2008:i:1:p:11-20 Modeling loan commitments (2008). (25) RePEc:eee:finlet:v:2:y:2005:i:3:p:131-151 Proxy-quality thresholds: Theory and applications (2005). (26) RePEc:eee:finlet:v:6:y:2009:i:2:p:56-72 The diversification cost of large, concentrated equity stakes. How big is it? Is it justified? (2009). (27) RePEc:eee:finlet:v:3:y:2006:i:1:p:23-39 On the sequencing of projects, reputation building, and relationship finance (2006). (28) RePEc:eee:finlet:v:2:y:2005:i:3:p:107-124 Industry momentum and common factors (2005). (29) RePEc:eee:finlet:v:3:y:2006:i:3:p:194-206 Expanding the frontier one asset at a time (2006). (30) RePEc:eee:finlet:v:5:y:2008:i:3:p:172-182 Option pricing in a Garch model with tempered stable innovations (2008). (31) RePEc:eee:finlet:v:1:y:2004:i:3:p:143-153 On the consequences of state dependent preferences for the pricing of financial assets (2004). (32) RePEc:eee:finlet:v:2:y:2005:i:4:p:248-259 Cointegration analysis of the Fed model (2005). (33) RePEc:eee:finlet:v:4:y:2007:i:2:p:82-91 Rare events and annuity market participation (2007). (34) RePEc:eee:finlet:v:2:y:2005:i:2:p:67-74 The generalized asymmetric dynamic covariance model (2005). (35) RePEc:eee:finlet:v:3:y:2006:i:3:p:165-172 Modeling default risk: A new structural approach (2006). (36) RePEc:eee:finlet:v:5:y:2008:i:2:p:88-95 Positivity constraints on the conditional variances in the family of conditional correlation GARCH models (2008). (37) RePEc:eee:finlet:v:5:y:2008:i:1:p:59-67 On measuring concentration in banking systems (2008). (38) RePEc:eee:finlet:v:2:y:2005:i:3:p:165-172 A theory of loan syndication (2005). (39) RePEc:eee:finlet:v:3:y:2006:i:4:p:235-243 Exchange rates and order flow in the long run (2006). (40) RePEc:eee:finlet:v:3:y:2006:i:2:p:102-105 Reply to Asset trading volume in infinite-horizon economies with dynamically complete markets and heterogeneous agents: Comment (2006). (41) RePEc:eee:finlet:v:4:y:2007:i:4:p:203-216 Why inexperienced investors do not learn: They do not know their past portfolio performance (2007). (42) repec:eee:finlet:v:1:y:2004:i:1:p:2-10 (). (43) RePEc:eee:finlet:v:2:y:2005:i:3:p:125-130 A note on sufficient conditions for no arbitrage (2005). (44) RePEc:eee:finlet:v:3:y:2006:i:3:p:207-211 A note on a barrier exchange option: The worlds simplest option formula? (2006). (45) RePEc:eee:finlet:v:5:y:2008:i:4:p:191-203 Time-series predictability in the disaster model (2008). (46) RePEc:eee:finlet:v:1:y:2004:i:3:p:171-177 Myopic loss aversion and the equity premium puzzle reconsidered (2004). (47) RePEc:eee:finlet:v:4:y:2007:i:2:p:95-103 The impact of keeping up with the Joneses behavior on asset prices and portfolio choice (2007). (48) RePEc:eee:finlet:v:3:y:2006:i:3:p:181-193 Disentangling risk aversion and intertemporal substitution through a reference level (2006). (49) RePEc:eee:finlet:v:5:y:2008:i:3:p:162-171 On the qualitative effect of volatility and duration on prices of Asian options (2008). (50) RePEc:eee:finlet:v:1:y:2004:i:2:p:90-99 How do stock prices respond to fundamental shocks? (2004). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 Recent citations received in: 2006 (1) RePEc:han:dpaper:dp-352 The Obstinate Passion of Foreign Exchange Professionals: Technical Analysis (2006). Universität Hannover, Wirtschaftswissenschaftliche Fakultät / Diskussionspapiere der Wirtschaftswissenschaftlichen Fakultät der Universität Hanno (2) RePEc:wrk:warwec:769 The Obstinate Passion of Foreign Exchange Professionals : Technical Analysis (2006). University of Warwick, Department of Economics / The Warwick Economics Research Paper Series (TWERPS) (3) RePEc:yor:yorken:06/12 Equity Valuation Under Stochastic Interest Rates (2006). Department of Economics, University of York / Discussion Papers Recent citations received in: 2005 (1) RePEc:bog:wpaper:30 The European Union GDP Forecast Rationality under Asymmetric Preferences (2005). Special Studies Division, Economic Research Department, Bank of Greece / Working Papers Recent citations received in: 2004 (1) RePEc:cte:wsrepe:ws046315 STOCHASTIC VOLATILITY MODELS AND THE TAYLOR EFFECT (2004). Universidad Carlos III, Departamento de EstadÃstica y EconometrÃa / Statistics and Econometrics Working Papers (2) RePEc:dnb:dnbwpp:016 Does market timing drive capital structures? A panel data study for Dutch firms (2004). Netherlands Central Bank, Research Department / DNB Working Papers (3) RePEc:hhs:hastef:0563 Stylized Facts of Financial Time Series and Three Popular Models of Volatility (2004). Stockholm School of Economics / Working Paper Series in Economics and Finance (4) RePEc:xrs:sfbmaa:04-15 Multiple-bank lending: diversification and free-riding in monitoring (2004). Sonderforschungsbereich 504, University of Mannheim / Sonderforschungsbereich 504 Publications Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||