|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

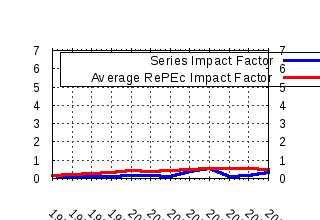

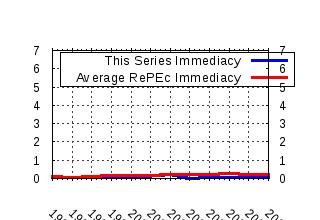

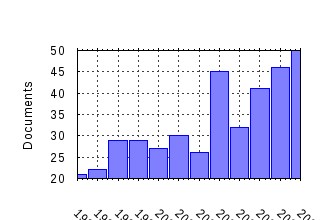

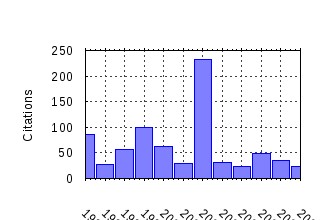

Computational Economics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:kap:compec:v:20:y:2002:i:1-2:p:1-20 Solving Linear Rational Expectations Models. (2002). (2) RePEc:kap:compec:v:9:y:1996:i:2:p:83-127 Computing Solutions for Large General Equilibrium Models Using GEMPACK. (1996). (3) RePEc:kap:compec:v:20:y:2002:i:1-2:p:87-116 Production, Growth and Business Cycles: Technical Appendix. (2002). (4) RePEc:kap:compec:v:14:y:1999:i:1-2:p:1-46 Applied General Equilibrium Modeling with MPSGE as a GAMS Subsystem: An Overview of the Modeling Framework and Syntax. (1999). (5) RePEc:kap:compec:v:15:y:2000:i:3:p:227-249 Decomposing Simulation Results with Respect to Exogenous Shocks (2000). (6) RePEc:kap:compec:v:19:y:2002:i:1:p:95-132 Heterogeneous Beliefs, Risk and Learning in a Simple Asset Pricing Model. (2002). (7) RePEc:kap:compec:v:20:y:2002:i:1-2:p:21-55 Solving Dynamic Equilibrium Models by a Method of Undetermined Coefficients. (2002). (8) RePEc:kap:compec:v:13:y:1999:i:1:p:41-60 Using Genetic Algorithms to Model the Evolution of Heterogeneous Beliefs. (1999). (9) RePEc:kap:compec:v:26:y:2005:i:1:p:19-49 Estimation of Agent-Based Models: The Case of an Asymmetric Herding Model (2005). (10) RePEc:kap:compec:v:20:y:2002:i:1-2:p:57-86 System Reduction and Solution Algorithms for Singular Linear Difference Systems under Rational Expectations. (2002). (11) RePEc:kap:compec:v:8:y:1995:i:3:p:205-31 Self-Organization of Markets: An Example of a Computational Approach. (1995). (12) RePEc:kap:compec:v:27:y:2006:i:1:p:3-34 An Evolutionary Model of Endogenous Business Cycles (2006). (13) RePEc:kap:compec:v:17:y:2001:i:2-3:p:125-39 A Higher-Order Taylor Expansion Approach to Simulation of Stochastic Forward-Looking Models with an Application to a Nonlinear Phillips Curve Model. (2001). (14) RePEc:kap:compec:v:11:y:1998:i:1-2:p:21-40 Moving Endpoints and the Internal Consistency of Agents Ex Ante Forecasts. (1998). (15) RePEc:kap:compec:v:10:y:1997:i:1:p:67-87 On Incentives and Updating in Agent Based Models. (1997). (16) RePEc:kap:compec:v:22:y:2003:i:2:p:255-272 Traders Long-Run Wealth in an Artificial Financial Market (2003). (17) RePEc:kap:compec:v:26:y:2005:i:2:p:107-128 User-Friendly Parallel Computations with Econometric Examples (2005). (18) RePEc:kap:compec:v:13:y:1999:i:2:p:147-62 The Effect of (Mis-Specified) GARCH Filters on the Finite Sample Distribution of the BDS Test. (1999). (19) RePEc:kap:compec:v:16:y:2000:i:1/2:p:105-136 A Computational Approach to Finding Causal Economic Laws (2000). (20) RePEc:kap:compec:v:23:y:2004:i:3:p:271-288 Spectral Analysis as a Tool for Financial Policy: An Analysis of the Short-End of the British Term Structure (2004). (21) RePEc:kap:compec:v:8:y:1995:i:3:p:233-53 Modular Technical Change and Genetic Algorithms. (1995). (22) RePEc:kap:compec:v:8:y:1995:i:3:p:181-203 Coordination via Genetic Learning. (1995). (23) RePEc:kap:compec:v:14:y:1999:i:3:p:263-67 Should Macroeconomic Policy Makers Consider Parameter Covariances? (1999). (24) RePEc:kap:compec:v:25:y:2005:i:4:p:343-379 Solving Finite Mixture Models: Efficient Computation in Economics Under Serial and Parallel Execution (2005). (25) RePEc:kap:compec:v:11:y:1998:i:1-2:p:53-70 Modelling Federal Reserve Discount Policy. (1998). (26) RePEc:kap:compec:v:19:y:2002:i:2:p:145-78 Maximum Likelihood Estimation Using Parallel Computing: An Introduction to MPI. (2002). (27) RePEc:kap:compec:v:12:y:1998:i:1:p:79-95 Implementing the Double Bootstrap. (1998). (28) RePEc:kap:compec:v:18:y:2001:i:1:p:9-24 Learning to Be Thoughtless: Social Norms and Individual Computation. (2001). (29) RePEc:kap:compec:v:26:y:2005:i:3:p:1-29 Discrete Working Time Choice in an Applied General Equilibrium Model (2005). (30) RePEc:kap:compec:v:11:y:1998:i:1-2:p:71-87 Numerical Strategies for Solving the Nonlinear Rational Expectations Commodity Market Model. (1998). (31) RePEc:kap:compec:v:10:y:1997:i:3:p:251-66 Constrained Maximum Likelihood. (1997). (32) RePEc:kap:compec:v:15:y:2000:i:3:p:173-199 Collinearity and Two-Step Estimation of Sample Selection Models: Problems, Origins, and Remedies (2000). (33) RePEc:kap:compec:v:18:y:2001:i:2:p:159-72 Climate Coalitions in an Integrated Assessment Model. (2001). (34) RePEc:kap:compec:v:15:y:2000:i:1-2:p:59-78 A Test for Strong Hysteresis. (2000). (35) RePEc:kap:compec:v:22:y:2003:i:1:p:65-74 Seasonal Misspecification in the Context of Fractionally Integrated Univariate Time Series (2003). (36) RePEc:kap:compec:v:26:y:2005:i:1:p:65-89 Detecting Business Cycle Asymmetries Using Artificial Neural Networks and Time Series Models (2005). (37) RePEc:kap:compec:v:30:y:2007:i:3:p:291-327 Dynamic Testing of Wholesale Power Market Designs: An Open-Source Agent-Based Framework (2007). (38) RePEc:kap:compec:v:16:y:2000:i:1/2:p:149-171 Explaining the Persistence of Commodity Prices (2000). (39) RePEc:kap:compec:v:10:y:1997:i:4:p:317-35 Hybrid Classifiers for Financial Multicriteria Decision Making: The Case of Bankruptcy Prediction. (1997). (40) RePEc:kap:compec:v:27:y:2006:i:2:p:207-228 An Application of Extreme Value Theory for Measuring Financial Risk (2006). (41) RePEc:kap:compec:v:19:y:2002:i:2:p:197-225 Rational Error Correction. (2002). (42) RePEc:kap:compec:v:14:y:1999:i:3:p:219-35 Static, Dynamic, and Hybrid Neural Networks in Forecasting Inflation. (1999). (43) RePEc:kap:compec:v:28:y:2006:i:4:p:355-370 Robust Evolutionary Algorithm Design for Socio-economic Simulation (2006). (44) RePEc:kap:compec:v:12:y:1998:i:3:p:223-41 ASPEN: A Microsimulation Model of the Economy. (1998). (45) RePEc:kap:compec:v:12:y:1998:i:2:p:97-114 Bubbles and Market Crashes. (1998). (46) RePEc:kap:compec:v:14:y:1999:i:1-2:p:151-81 Programming Languages in Economics. (1999). (47) RePEc:kap:compec:v:30:y:2007:i:2:p:153-169 Multidimensional Spline Interpolation: Theory and Applications (2007). (48) RePEc:kap:compec:v:11:y:1998:i:3:p:245-63 A Comparison of the Performance of Flexible Functional Forms for Use in Applied General Equilibrium Modelling. (1998). (49) RePEc:kap:compec:v:21:y:2003:i:3:p:257-276 Is it Possible to Study Chaotic and ARCH Behaviour Jointly? Application of a Noisy Mackeyââ¬âGlass Equation with Heteroskedastic Errors to the Paris Stock Exchange Returns Series (2003). (50) RePEc:kap:compec:v:8:y:1995:i:3:p:159-79 A Distributed Parallel Genetic Algorithm for Solving Optimal Growth Models. (1995). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:isu:genres:12776 An Agent-Based Computational Laboratory for Wholesale Power Market Design (2007). Iowa State University, Department of Economics / Staff General Research Papers (2) RePEc:kap:compec:v:30:y:2007:i:3:p:195-226 A Critical Guide to Empirical Validation of Agent-Based Models in Economics: Methodologies, Procedures, and Open Problems (2007). Computational Economics (3) RePEc:mdl:mdlpap:0707 Endogenous Participation in Charity Auctions (2007). Middlebury College, Department of Economics / Middlebury College Working Paper Series Recent citations received in: 2006 (1) RePEc:kap:compec:v:28:y:2006:i:4:p:333-354 Revisiting Individual Evolutionary Learning in the Cobweb Model ââ¬â An Illustration of the Virtual Spite-Effect (2006). Computational Economics (2) RePEc:kap:compec:v:28:y:2006:i:4:p:355-370 Robust Evolutionary Algorithm Design for Socio-economic Simulation (2006). Computational Economics Recent citations received in: 2005 (1) RePEc:ams:ndfwpp:05-12 Behavioral Heterogeneity in Stock Prices (2005). Universiteit van Amsterdam, Center for Nonlinear Dynamics in Economics and Finance / CeNDEF Working Papers (2) RePEc:fce:doctra:0505 A model of the stochastic convergence between business cycles (2005). Observatoire Francais des Conjonctures Economiques (OFCE) / Documents de Travail de l'OFCE Recent citations received in: 2004 (1) RePEc:cte:wbrepe:wb046023 AN INTERIOR POINT ALGORITHM FOR COMPUTING EQUILIBRIA IN ECONOMIES WITH INCOMPLETE ASSET MARKETS (2004). Universidad Carlos III, Departamento de EconomÃa de la Empresa / Business Economics Working Papers (2) RePEc:kap:compec:v:24:y:2004:i:3:p:209-221 Robust Control: A Note on the Timing of Model Uncertainty (2004). Computational Economics Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||