|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

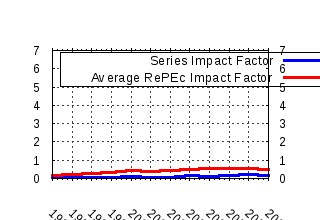

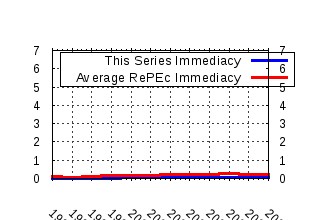

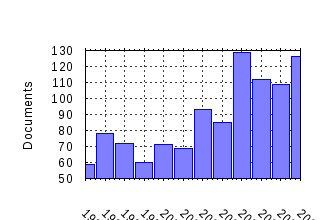

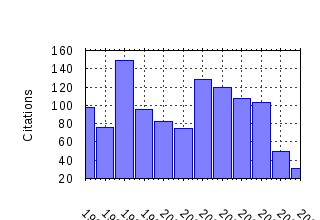

Applied Financial Economics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:taf:apfiec:v:6:y:1996:i:6:p:463-75 The Stable Paretian Hypothesis and the Frequency of Large Returns: An Examination of Major German Stocks. (1996). (2) RePEc:taf:apfiec:v:8:y:1998:i:6:p:607-14 Linkages between the US and European Equity Markets: Further Evidence from Cointegration Tests. (1998). (3) RePEc:taf:apfiec:v:15:y:2005:i:5:p:315-326 Can mergers in Europe help banks hedge against macroeconomic risk? (2005). (4) RePEc:taf:apfiec:v:8:y:1998:i:6:p:689-96 Efficiency of Multinational Banks: An Empirical Investigation. (1998). (5) RePEc:taf:apfiec:v:4:y:1994:i:2:p:121-32 Investment Decisions and the Role of Debt, Liquid Assets and Cash Flow: Evidence from Panel Data. (1994). (6) RePEc:taf:apfiec:v:5:y:1995:i:4:p:257-64 The Effect of Financial Liberalization on the Efficiency of Turkish Commercial Banks. (1995). (7) RePEc:taf:apfiec:v:15:y:2005:i:14:p:1007-1017 Does patenting increase the probability of being acquired? Evidence from cross-border and domestic acquisitions (2005). (8) RePEc:taf:apfiec:v:6:y:1996:i:4:p:367-75 Economies of Scale and Scope in European Banking. (1996). (9) RePEc:taf:apfiec:v:9:y:1999:i:5:p:501-11 Short-Term and Long-Term Price Linkages between the Equity Markets of Australia and Its Major Trading Partners. (1999). (10) RePEc:taf:apfiec:v:13:y:2003:i:7:p:477-486 Stock market integration and financial crises: the case of Asia (2003). (11) RePEc:taf:apfiec:v:10:y:2000:i:2:p:177-84 Long Memory in the Greek Stock Market. (2000). (12) RePEc:taf:apfiec:v:11:y:2001:i:1:p:1-8 Nonparametric Cointegration Analysis of Real Exchange Rates. (2001). (13) RePEc:taf:apfiec:v:8:y:1998:i:3:p:245-56 Volatility Spillovers across Equity Markets: European Evidence. (1998). (14) RePEc:taf:apfiec:v:12:y:2002:i:12:p:895-911 Credit Risk and Efficiency in the European Banking System: A Three-Stage Analysis. (2002). (15) RePEc:taf:apfiec:v:7:y:1997:i:2:p:177-91 Regime Switching in Stock Market Returns. (1997). (16) RePEc:taf:apfiec:v:16:y:2006:i:1-2:p:1-17 Real exchange rates and Purchasing Power Parity: mean-reversion in economic thought (2006). (17) RePEc:taf:apfiec:v:12:y:2002:i:7:p:475-84 African Stock Markets: Multiple Variance Ratio Tests of Random Walks. (2002). (18) RePEc:taf:apfiec:v:9:y:1999:i:1:p:73-85 Macroeconomic Determinants of Long-Term Stock Market Comovements among Major EMS Countries. (1999). (19) RePEc:taf:apfiec:v:13:y:2003:i:2:p:113-122 Technical analysis in foreign exchange markets: evidence from the EMS (2003). (20) RePEc:taf:apfiec:v:8:y:1998:i:6:p:577-87 Modelling Real Exchange Rate Behaviour: A Cross-Country Study. (1998). (21) RePEc:taf:apfiec:v:13:y:2003:i:7:p:525-535 Monetary policy rules and regime shifts (2003). (22) RePEc:taf:apfiec:v:2:y:1992:i:4:p:191-98 The Form of Time Variation of Systematic Risk: Some Australian Evidence. (1992). (23) RePEc:taf:apfiec:v:6:y:1996:i:4:p:307-17 Testing for Non-linearity in Daily Sterling Exchange Rates. (1996). (24) RePEc:taf:apfiec:v:15:y:2005:i:15:p:1041-1051 Financial development and economic growth in the Middle East (2005). (25) RePEc:taf:apfiec:v:12:y:2002:i:12:p:851-61 Testing for Cointegration between International Stock Prices. (2002). (26) RePEc:taf:apfiec:v:8:y:1998:i:4:p:401-07 Continuous-Time Short Term Interest Rate Models. (1998). (27) RePEc:taf:apfiec:v:3:y:1993:i:3:p:255-66 The Causality between Official and Parallel Exchange Rates in Developing Countries. (1993). (28) RePEc:taf:apfiec:v:4:y:1994:i:1:p:33-39 Some International Evidence Regarding the Stochastic Memory of Stock Returns. (1994). (29) RePEc:taf:apfiec:v:3:y:1993:i:2:p:119-26 Stochastic Behaviour of the Athens Stock Exchange. (1993). (30) RePEc:taf:apfiec:v:6:y:1996:i:3:p:293-300 Does It Matter How Seigniorage Is Measured. (1996). (31) RePEc:taf:apfiec:v:9:y:1999:i:1:p:1-9 Short- and Long-Term links among European and US Stock Markets. (1999). (32) RePEc:taf:apfiec:v:12:y:2002:i:11:p:791-98 Evaluating the Hedging Performance of the Constant-Correlation GARCH Model. (2002). (33) RePEc:taf:apfiec:v:12:y:2002:i:1:p:19-24 The Determinants of Corporate Debt Maturity: Evidence from UK Firms. (2002). (34) RePEc:taf:apfiec:v:15:y:2005:i:8:p:519-530 Can the Balassa-Samuelson theory explain long-run real exchange rate movements in OECD countries? (2005). (35) RePEc:taf:apfiec:v:2:y:1992:i:1:p:43-47 The International Transmission of Stock Market Fluctuation between the Developed Markets and the Asian-Pacific Markets. (1992). (36) RePEc:taf:apfiec:v:9:y:1999:i:4:p:385-95 The Information Content of the German Term Structure Regarding Inflation. (1999). (37) RePEc:taf:apfiec:v:8:y:1998:i:2:p:191-200 Market Structure and Performance in Spanish Banking Using a Direct Measure of Efficiency. (1998). (38) RePEc:taf:apfiec:v:8:y:1998:i:2:p:167-74 Stock Market Prices, Causality and Efficiency: Evidence from the Athens Stock Exchange. (1998). (39) RePEc:taf:apfiec:v:11:y:2001:i:5:p:557-71 Efficiency and Productivity Change in UK Banking. (2001). (40) RePEc:taf:apfiec:v:8:y:1998:i:2:p:145-53 Modelling the Asymmetry of Stock Market Volatility. (1998). (41) RePEc:taf:apfiec:v:5:y:1995:i:1:p:11-18 Long Run Behaviour of Pacific-Basin Stock Prices. (1995). (42) RePEc:taf:apfiec:v:7:y:1997:i:1:p:59-74 A Comparative Analysis of the Propagation of Stock Market Fluctuations in Alternative Models of Dynamic Causal Linkages. (1997). (43) RePEc:taf:apfiec:v:4:y:1994:i:4:p:265-78 A Cointegration Analysis of Danish Zero-Coupon Bond Yields. (1994). (44) RePEc:taf:apfiec:v:4:y:1994:i:3:p:193-205 A Revenue-Restricted Cost Study of 100 Large Banks. (1994). (45) RePEc:taf:apfiec:v:13:y:2003:i:7:p:543-551 How rewarding is technical analysis? Evidence from Singapore stock market (2003). (46) RePEc:taf:apfiec:v:14:y:2004:i:17:p:1253-1268 International portfolio diversification to Central European stock markets (2004). (47) RePEc:taf:apfiec:v:4:y:1994:i:1:p:1-10 International Diversification among the Capital Markets of the EEC. (1994). (48) RePEc:taf:apfiec:v:2:y:1992:i:3:p:145-59 Dynamics of the Composition of Household Asset Portfolios and the Life Cycle. (1992). (49) RePEc:taf:apfiec:v:12:y:2002:i:10:p:725-29 Long Memory in Stock Returns: Some International Evidence. (2002). (50) RePEc:taf:apfiec:v:5:y:1995:i:1:p:33-42 The Long-Run Gains from International Equity Diversification: Australian Evidence from Cointegration Tests. (1995). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:col:000094:004246 Pronósticos directos de la inflación colombiana (2007). TITULARIZADORA COLOMBIANA / INFORMES (2) RePEc:col:000094:004247 Pronósticos directos de la inflación colombiana (2007). TITULARIZADORA COLOMBIANA / INFORMES (3) RePEc:crt:wpaper:0701 Backtesting VaR Models: An Expected Shortfall Approach (2007). University of Crete, Department of Economics / Working Papers (4) RePEc:pra:mprapa:5319 Forecasting volatility: Evidence from the Macedonian stock exchange (2007). University Library of Munich, Germany / MPRA Paper (5) RePEc:taf:apfelt:v:3:y:2007:i:1:p:31-37 Simulated evidence on the distribution of the standardized one-step-ahead prediction errors in ARCH processes (2007). Applied Financial Economics Letters (6) RePEc:ven:wpaper:2007_17 Dynamic Risk Exposure in Hedge Funds (2007). University of Venice Ca' Foscari, Department of Economics / Working Papers Recent citations received in: 2006 (1) RePEc:crt:wpaper:0615 The Components of the Bid-Ask Spread: The case of the Athens Stock Exchange (2006). University of Crete, Department of Economics / Working Papers (2) RePEc:ega:wpaper:200607 Technology and Customer Value Dynamics in Banking Industry: Measuring Symbiotic Influence in Growth and Performance (2006). Tecnológico de Monterrey, Campus Ciudad de México / Marketing Working Papers (3) RePEc:hhs:iuiwop:0668 Producer Prices in the Transition to a Common Currency (2006). The Research Institute of Industrial Economics / IUI Working Paper Series (4) RePEc:ijf:ijfiec:v:11:y:2006:i:4:p:355-370 The out-of-sample forecasts of nonlinear long-memory models of the real exchange rate (2006). International Journal of Finance & Economics (5) RePEc:kap:ecopln:v:39:y:2006:i:1:p:105-124 Consolidation and Competition in Emerging Market: An Empirical Test for Malaysian Banking Industry (2006). Economics of Planning (6) RePEc:man:cgbcrp:77 Periodic Dynamic Conditional Correlations between Stock Markets in Europe and the US (2006). The School of Economic Studies, The Univeristy of Manchester / Centre for Growth and Business Cycle Research Discussion Paper Series (7) RePEc:taf:apfelt:v:2:y:2006:i:2:p:99-103 Market trader heterogeneity and high frequency volatility dynamics: further evidence from intra-day FTSE-100 futures data (2006). Applied Financial Economics Letters (8) RePEc:uwa:wpaper:06-29 A New Approach to Forecasting Exchange Rates (2006). The University of Western Australia, Department of Economics / Economics Discussion / Working Papers Recent citations received in: 2005 (1) RePEc:cnb:wpaper:2005/06 Deteriorating Cost Efficiency in Commercial Banks Signals an Increasing Risk of Failure (2005). Czech National Bank, Research Department / Working Papers (2) RePEc:dgr:kubcen:200560 Leveraged public to private transactions in the UK (2005). Tilburg University, Center for Economic Research / Discussion Paper (3) RePEc:dgr:kubtil:200515 Leveraged public to private transactions in the UK (2005). Tilburg University, Tilburg Law and Economic Center / Discussion Paper (4) RePEc:kap:openec:v:16:y:2005:i:2:p:107-133 A Sequential Test for Structural Breaks in the Causal Linkages Between the G7 Short-Term Interest Rates (2005). Open Economies Review (5) RePEc:ntd:wpaper:2005-08 El impacto de la liquidez corporativa sobre el valor de las decisiones financieras de la empresa (2005). Interuniversitary Doctorate Program New Trends on Business Administration, Universities of Valladolid, Burgos and Salamanca (Spain). Programa de Docto (6) RePEc:taf:apfelt:v:1:y:2005:i:6:p:343-347 An alternative method to test for contagion with an application to the Asian financial crisis (2005). Applied Financial Economics Letters (7) RePEc:taf:applec:v:37:y:2005:i:18:p:2161-2166 Are the Australian and New Zealand stock prices nonlinear with a unit root? (2005). Applied Economics (8) RePEc:wpa:wuwpfi:0504020 An Analysis of the Impacts of Non-Synchronous Trading On (2005). EconWPA / Finance Recent citations received in: 2004 (1) RePEc:ivi:wpasad:2004-45 SPURIOUS AND HIDDEN VOLATILITY (2004). Instituto Valenciano de Investigaciones Económicas, S.A. (Ivie) / Working Papers. Serie AD (2) RePEc:may:mayecw:n1411004 The effect of the Euro on country versus industry portfolio diversification (2004). Department of Economics, National University of Ireland - Maynooth / Economics Department Working Paper Series (3) RePEc:pra:mprapa:3532 Modelling extreme financial returns of global equity markets (2004). University Library of Munich, Germany / MPRA Paper (4) RePEc:rtv:ceisrp:52 Industry and Time Specific Deviations from Fundamental Values in a Random Coefficient Model (2004). Tor Vergata University, CEIS / Research Paper Series (5) RePEc:una:unccee:wp0408 Fundamentals and the origin of Fama-French factors (2004). School of Economics and Business Administration, University of Navarra / Faculty Working Papers (6) RePEc:wpa:wuwpfi:0406007 Efficiency of Islamic Banks: an Empirical Analysis of 18 Banks (2004). EconWPA / Finance (7) RePEc:wpa:wuwpfi:0408006 Performance of Indian commercial banks (1995-2002): an application of data envelopment analysis and Malmquist productivity index (2004). EconWPA / Finance Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||