|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

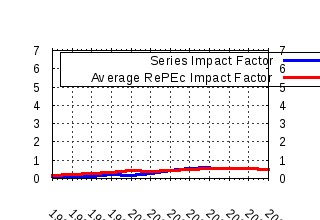

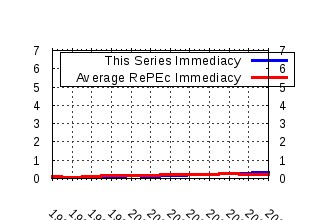

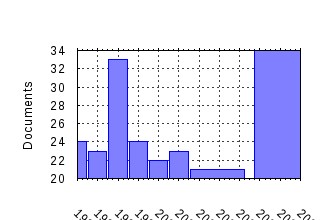

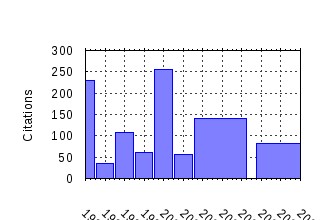

Econometric Reviews Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:taf:emetrv:v:11:y:1992:i:2:p:143-172 Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances (1992). (2) RePEc:taf:emetrv:v:3:y:1984:i:1:p:1-100 Forecasting and conditional projection using realistic prior distributions (1984). (3) RePEc:taf:emetrv:v:19:y:2000:i:3:p:321-340 GMM Estimation with persistent panel data: an application to production functions (2000). (4) RePEc:taf:emetrv:v:4:y:1985:i:2:p:289-328 Frontier production functions (1985). (5) RePEc:taf:emetrv:v:15:y:1996:i:3:p:197-235 A test for independence based on the correlation dimension (1996). (6) RePEc:taf:emetrv:v:5:y:1986:i:1:p:1-50 Modelling the persistence of conditional variances (1986). (7) RePEc:taf:emetrv:v:17:y:1998:i:1:p:57-84 A residual-based test of the null of cointegration in panel data (1998). (8) RePEc:taf:emetrv:v:15:y:1996:i:4:p:369-386 Making wald tests work for cointegrated VAR systems (1996). (9) RePEc:taf:emetrv:v:13:y:1994:i:2:p:205-229 The role of the constant and linear terms in cointegration analysis of nonstationary variables (1994). (10) RePEc:taf:emetrv:v:21:y:2002:i:1:p:1-47 SMOOTH TRANSITION AUTOREGRESSIVE MODELS - A SURVEY OF RECENT DEVELOPMENTS (2002). (11) RePEc:taf:emetrv:v:13:y:1994:i:1:p:1-91 Artificial neural networks: an econometric perspective (1994). (12) RePEc:taf:emetrv:v:26:y:2007:i:2-4:p:113-172 Bayesian Analysis of DSGE Models (2007). (13) RePEc:taf:emetrv:v:15:y:1996:i:2:p:115-158 Bootstrapping time series models (1996). (14) RePEc:taf:emetrv:v:2:y:1983:i:2:p:159-218 Diagnostic tests as residual analysis (1983). (15) RePEc:taf:emetrv:v:19:y:2000:i:3:p:263-286 Nonstationary panel data analysis: an overview of some recent developments (2000). (16) RePEc:taf:emetrv:v:11:y:1992:i:1:p:1-71 The econometrics of female labor supply and children (1992). (17) RePEc:taf:emetrv:v:21:y:2002:i:1:p:49-87 LONG-RUN STRUCTURAL MODELLING (2002). (18) RePEc:taf:emetrv:v:11:y:1992:i:3:p:265-306 Testing the lucas critique: A review (1992). (19) RePEc:taf:emetrv:v:15:y:1996:i:3:p:261-274 Nonparametric testing of closeness between two unknown distribution functions (1996). (20) RePEc:taf:emetrv:v:13:y:1994:i:2:p:259-285 Vector autoregression and causality: a theoretical overview and simulation study (1994). (21) RePEc:taf:emetrv:v:21:y:2002:i:4:p:431-447 ON THE ASYMPTOTICS OF ADF TESTS FOR UNIT ROOTS (2002). (22) RePEc:taf:emetrv:v:5:y:1986:i:1:p:51-56 Modeling The persistence Of Conditional Variances: A Comment (1986). (23) RePEc:taf:emetrv:v:17:y:1998:i:1:p:1-29 Confidence intervals for impulse responses under departures from normality (1998). (24) RePEc:taf:emetrv:v:19:y:2000:i:1:p:1-48 Recent developments in bootstrapping time series (2000). (25) RePEc:taf:emetrv:v:8:y:1989:i:2:p:151-186 Econometric tests of rationality and market efficiency (1989). (26) RePEc:taf:emetrv:v:20:y:2001:i:3:p:247-318 A REVIEW OF SYSTEMS COINTEGRATION TESTS (2001). (27) RePEc:taf:emetrv:v:8:y:1989:i:2:p:207-212 Econometric tests of rationality and market efficiency (1989). (28) RePEc:taf:emetrv:v:19:y:2000:i:1:p:55-68 Bootstrap tests: how many bootstraps? (2000). (29) RePEc:taf:emetrv:v:2:y:1983:i:1:p:85-110 Model specification tests against non-nested alternatives (1983). (30) RePEc:taf:emetrv:v:18:y:1999:i:1:p:1-73 Using simulation methods for bayesian econometric models: inference, development,and communication (1999). (31) RePEc:taf:emetrv:v:19:y:2000:i:3:p:287-320 Stochastic dominance amongst swedish income distributions (2000). (32) RePEc:taf:emetrv:v:10:y:1991:i:3:p:253-325 Basic structure of the asymptotic theory in dynamic nonlinear econometric models (1991). (33) RePEc:taf:emetrv:v:9:y:1990:i:2:p:123-184 Specification of household engel curves by nonparametric regression (1990). (34) RePEc:taf:emetrv:v:18:y:1999:i:3:p:287-330 An introduction to hypergeometric functions for economists (1999). (35) RePEc:taf:emetrv:v:19:y:2000:i:4:p:312-320 Estimation and decomposition of productivity change when production is not efficient: a paneldata approach (2000). (36) RePEc:taf:emetrv:v:4:y:1985:i:1:p:121-174 Benefits and limitations of panel data (1985). (37) RePEc:taf:emetrv:v:12:y:1993:i:2:p:183-216 An introduction to econometric applications of empirical process theory for dependent random variables (1993). (38) RePEc:taf:emetrv:v:12:y:1993:i:1:p:103-124 A comparison of some robust, adaptive, and partially adaptive estimators of regression models (1993). (39) RePEc:taf:emetrv:v:14:y:1995:i:1:p:101-116 Goodness-of-fit measures in binary choice models (1995). (40) RePEc:taf:emetrv:v:21:y:2002:i:3:p:309-336 A MONTE CARLO COMPARISON OF VARIOUS ASYMPTOTIC APPROXIMATIONS TO THE DISTRIBUTION OF INSTRUMENTAL VARIABLES ESTIMATORS (2002). (41) RePEc:taf:emetrv:v:12:y:1993:i:3:p:261-330 Modeling asset returns with alternative stable distributions (1993). (42) RePEc:taf:emetrv:v:3:y:1984:i:2:p:145-194 Adaptive estimation of non-linear regression models (1984). (43) RePEc:taf:emetrv:v:12:y:1993:i:1:p:1-32 Testing stationarity and trend stationarity against the unit root hypothesis (1993). (44) RePEc:taf:emetrv:v:26:y:2007:i:1:p:53-90 MIDAS Regressions: Further Results and New Directions (2007). (45) RePEc:taf:emetrv:v:15:y:1996:i:4:p:401-429 Testing for structural change in cointegrated regression models: some comparisons and generalizations (1996). (46) RePEc:taf:emetrv:v:24:y:2005:i:4:p:369-404 (). (47) RePEc:taf:emetrv:v:1:y:1982:i:2:p:151-190 On unification of the asymptotic theory of nonlinear econometric models (1982). (48) RePEc:taf:emetrv:v:21:y:2002:i:3:p:273-307 SEPARATION, WEAK EXOGENEITY, AND P-T DECOMPOSITION IN COINTEGRATED VAR SYSTEMS WITH COMMON FEATURES (2002). (49) RePEc:taf:emetrv:v:7:y:1988:i:1:p:65-95 Prediction theory for autoregressivemoving average processes (1988). (50) RePEc:taf:emetrv:v:12:y:1993:i:2:p:137-181 A compendium to information theory in economics and econometrics (1993). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:cpr:ceprdp:6373 Euro Area Inflation Persistence in an Estimated Nonlinear DSGE Model (2007). C.E.P.R. Discussion Papers / CEPR Discussion Papers (2) RePEc:ecl:harjfk:rwp07-057 Monetary and Fiscal Policies in a Sudden Stop: Is Tighter Brighter? (2007). Harvard University, John F. Kennedy School of Government / Working Paper Series (3) RePEc:hhs:oruesi:2007_013 Bayesian Forecast Combination for VAR Models (2007). Ãrebro University, Department of Business, Economics, Statistics and Informatics / Working Papers (4) RePEc:hhs:rbnkwp:0216 Bayesian forecast combination for VAR models (2007). Sveriges Riksbank (Central Bank of Sweden) / Working Paper Series (5) RePEc:ifs:ifsewp:07/16 Heterogeneity in consumer demands and the income effect: evidence from panel data (2007). Institute for Fiscal Studies / IFS Working Papers (6) RePEc:irv:wpaper:070805 Political Business Cycles in the New Keynesian Model (2007). University of California-Irvine, Department of Economics / Working Papers (7) RePEc:lvl:lacicr:0749 Mixed Exponential Power Asymmetric Conditional Heteroskedasticity (2007). (8) RePEc:nbr:nberwo:13099 Monetary Policy Analysis with Potentially Misspecified Models (2007). National Bureau of Economic Research, Inc / NBER Working Papers (9) RePEc:pra:mprapa:3419 The U.S. Dynamic Taylor Rule With Multiple Breaks, 1984-2001. (2007). University Library of Munich, Germany / MPRA Paper (10) RePEc:rpo:ripoec:v:97:y:2007:i:6:p:149-202 Classical and Bayesian Methods for the VAR Analysis: International Comparisons (2007). Rivista di Politica Economica (11) RePEc:zbw:bubdp1:5573 Reconsidering the role of monetary indicators for euro area inflation from a Bayesian perspective using group inclusion probabilities (2007). Deutsche Bundesbank, Research Centre / Discussion Paper Series 1: Economic Studies Recent citations received in: 2006 Recent citations received in: 2005 Recent citations received in: 2004 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||