|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

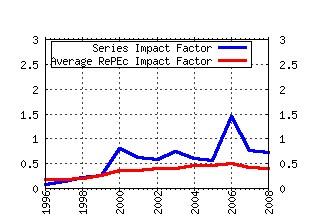

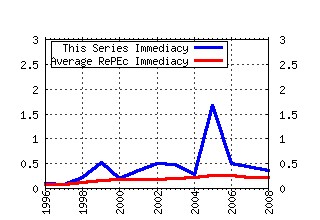

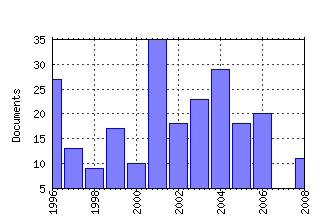

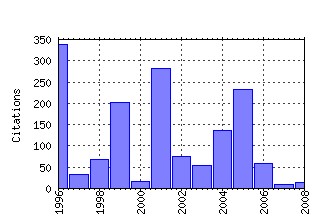

Economics Group, Nuffield College, University of Oxford / Economics Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:nuf:econwp:104 Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. (1995). (2) RePEc:nuf:econwp:0517 Stochastic Volatility (2005). (3) RePEc:nuf:econwp:9614 Initial conditions and moment restrictions in dynamic panel data

model (1996). (4) RePEc:nuf:econwp:0121 GMM Estimation of Empirical Growth Models (2001). (5) RePEc:nuf:econwp:1999-w12 Auction Theory: a Guide to the Literature. (1999). (6) RePEc:nuf:econwp:126 Unique Equilibrium in a Model of Self-Fulfilling Currency Attacks. (1996). (7) RePEc:nuf:econwp:9604 An omnibus test for univariate and multivariate normalit (1996). (8) RePEc:nuf:econwp:049 Auctions: Theory and Practice (2004). (9) RePEc:nuf:econwp:0104 Econometric analysis of realised volatility and its use in estimating stochastic volatility models (2001). (10) RePEc:nuf:econwp:1999-w3 Innovation and Market Value. (1999). (11) RePEc:nuf:econwp:0417 We Ran One Regression (2004). (12) RePEc:nuf:econwp:0116 How accurate is the asymptotic approximation to the distribution of realised volatility? (2001). (13) RePEc:nuf:econwp:146 Likelihood INference for Discretely Observed Non-linear Diffusions (1998). (14) RePEc:nuf:econwp:9713 Filtering via simulation: auxiliary particle filters (1997). (15) RePEc:nuf:econwp:143 Firm-Level Investment in France and the United States: An Exploration of What We Have Learned in Twenty Years (1998). (16) RePEc:nuf:econwp:0213 Econometric Analysis of Realised Covariation: High Frequency Covariance, Regression and Correlation in Financial Economics (2002). (17) RePEc:nuf:econwp:0118 Realised power variation and stochastic volatility models (2001). (18) RePEc:nuf:econwp:0603 Designing realised kernels to measure the ex-post variation of equity prices

in the presence of noise (2006). (19) RePEc:nuf:econwp:048 Capital Accumulation and Growth: A New Look at the Empirical Evidence (2004). (20) RePEc:nuf:econwp:125 Booms and Busts in the UK Housing Market. (1996). (21) RePEc:nuf:econwp:0526 Management of a Capital Stock by Strotzs Naive Planner (2006). (22) RePEc:nuf:econwp:1999-w11 The Tobacco Deal. (1999). (23) RePEc:nuf:econwp:0504 Adjustment Costs and the Identification of Cobb Douglas Production Functions (2005). (24) RePEc:nuf:econwp:0204 The Biggest Auction Ever: the Sale of the British 3G Telecom Licenses (2001). (25) RePEc:nuf:econwp:0507 Limit theorems for multipower variation in the presence of jumps (2006). (26) RePEc:nuf:econwp:1999-w20 Income Inequality and Macroeconomic Volatility: an Empirical Investigation. (1999). (27) RePEc:nuf:econwp:0509 Limited Asset Markets Participation, Monetary Policy and (Inverted) Keynesian Logic (2005). (28) RePEc:nuf:econwp:0320 Multimodality in the GARCH Regression Model (2003). (29) RePEc:nuf:econwp:0209 Pooling of Forecasts (2001). (30) RePEc:nuf:econwp:0102 Firm Level Investment and R&D in France and the United States: A Comparison (2001). (31) RePEc:nuf:econwp:0113 Inferring Repeated Game Strategies From Actions: Evidence From Trust Game Experiments (2001). (32) RePEc:nuf:econwp:0216 Unemployment, Labour Market Institutions and Shocks (2002). (33) RePEc:nuf:econwp:0005 An evaluation of forecasting using leading indicators (1994). (34) RePEc:nuf:econwp:141 Aggregation and Model Construction for Volatility Models (1998). (35) RePEc:nuf:econwp:0316 Wage and Price Phillips Curves

An empirical analysis of destabilizing wage-price spirals (2003). (36) RePEc:nuf:econwp:117 Bringing Income Distribution in from the Cold. (1996). (37) RePEc:nuf:econwp:0211 Economic Forecasting: Some Lessons from Recent Research (2001). (38) RePEc:nuf:econwp:9927 Multidimensional Inequality Measurement: a Proposal. (1999). (39) RePEc:nuf:econwp:115 Pathological Outcomes of Observational Learning. (1996). (40) RePEc:nuf:econwp:2000-w11 Does Competition Solve the Hold-Up Problem?. (2000). (41) RePEc:nuf:econwp:0011 Bartlett correction of the unit root test in autoregressive models (1995). (42) RePEc:nuf:econwp:0506 Limit theorems for bipower variation in financial econometrics (2006). (43) RePEc:nuf:econwp:0428 Regular and Modified Kernel-Based Estimators of Integrated Variance:

The Case with Independent Noise (2004). (44) RePEc:nuf:econwp:0516 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). (45) RePEc:nuf:econwp:0008 Generalized linear autoregressions (1995). (46) RePEc:nuf:econwp:0310 Identifying, Estimating and Testing Restricted Cointegrated Systems: An Overview (2003). (47) RePEc:nuf:econwp:0505 Estimating quadratic variation when quoted prices jump by a constant increment (2005). (48) RePEc:nuf:econwp:0217 Testing the Assumptions Behind the Use of Importance Sampling (2002). (49) RePEc:nuf:econwp:0110 Order determination in general vector autoregressions (2001). (50) RePEc:nuf:econwp:0522 Hurricanes: Intertemporal Trade and Capital Shocks (2005). Recent citations received in: | 2008 | 2007 | 2006 | 2005 Recent citations received in: 2008 (1) RePEc:fip:fedgif:943 Constructive data mining: modeling Argentine broad money demand (2008). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (2) RePEc:fip:fedgif:959 The fragility of sensitivity analysis: an encompassing perspective (2008). Board of Governors of the Federal Reserve System (U.S.) / International Finance Discussion Papers (3) RePEc:nbr:nberwo:14463 An Arbitrage-Free Generalized Nelson-Siegel Term Structure Model (2008). National Bureau of Economic Research, Inc / NBER Working Papers (4) RePEc:pra:mprapa:12260 Model and distribution uncertainty in multivariate GARCH estimation: a Monte Carlo analysis (2008). University Library of Munich, Germany / MPRA Paper Recent citations received in: 2007 Recent citations received in: 2006 (1) RePEc:cep:stiecm:/2006/509 Estimating Quadratic VariationConsistently in thePresence of Correlated MeasurementError (2006). Suntory and Toyota International Centres for Economics and Related Disciplines, LSE / STICERD - Econometrics Paper Series (2) RePEc:cor:louvco:2006080 Modelling financial high frequency data using point processes (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (3) RePEc:ctl:louvec:2006039 Modelling Financial High Frequency Data Using Point Processes (2006). Université catholique de Louvain, Département des Sciences Economiques / Université catholique de Louvain, Département des Sciences Economiques Workin (4) RePEc:nuf:econwp:0506 Limit theorems for bipower variation in financial econometrics (2006). Economics Group, Nuffield College, University of Oxford / Economics Papers (5) RePEc:nuf:econwp:0610 Subsampling realised kernels (2006). Economics Group, Nuffield College, University of Oxford / Economics Papers (6) RePEc:nuf:econwp:0612 High Dimensional Yield Curves: Models and Forecasting (2006). Economics Group, Nuffield College, University of Oxford / Economics Papers (7) RePEc:oxf:wpaper:278 Subsampling realised kernels (2006). University of Oxford, Department of Economics / Economics Series Working Papers (8) RePEc:oxf:wpaper:290 Open Economy Codependence: U.S. Monetary Policy and Interest Rate Pass-through (2006). University of Oxford, Department of Economics / Economics Series Working Papers (9) RePEc:rut:rutres:200620 Predictive Density Estimators for Daily Volatility Based on the Use of Realized Measures (2006). Rutgers University, Department of Economics / Departmental Working Papers (10) RePEc:stn:sotoec:0615 Open Economy Codependence: U.S. Monetary Policy and Interest Rate Pass-through (2006). Economics Division, School of Social Sciences, University of Southampton / Discussion Paper Series In Economics And Econometrics Recent citations received in: 2005 (1) RePEc:cpr:ceprdp:5212 Understanding the Effects of Government Spending on Consumption (2005). C.E.P.R. Discussion Papers / CEPR Discussion Papers (2) RePEc:cte:wsrepe:ws053605 BAYESIAN ESTIMATION OF THE GAUSSIAN MIXTURE GARCH MODEL (2005). Universidad Carlos III, Departamento de EstadÃstica y EconometrÃa / Statistics and Econometrics Working Papers (3) RePEc:cwl:cwldpp:1523 A Two-Stage Realized Volatility Approach to the Estimation for Diffusion Processes from Discrete Observations (2005). Cowles Foundation, Yale University / Cowles Foundation Discussion Papers (4) RePEc:dgr:uvatin:20050002 Model-based Measurement of Actual Volatility in High-Frequency Data (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (5) RePEc:dgr:uvatin:20050060 A Non-Gaussian Panel Time Series Model for Estimating and Decomposing Default Risk (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (6) RePEc:dgr:uvatin:20050092 Outlier Detection in GARCH Models (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (7) RePEc:dgr:uvatin:20050103 The Impact of Central Bank FX Interventions on Currency Components (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (8) RePEc:dgr:uvatin:20050117 On Importance Sampling for State Space Models (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (9) RePEc:dnb:dnbwpp:055 A Non-Gaussian Panel Time Series Model for Estimating and Decomposing Default Risk (2005). Netherlands Central Bank, Research Department / DNB Working Papers (10) RePEc:fip:fedgfe:2005-63 Explaining credit default swap spreads with the equity volatility and jump risks of individual firms (2005). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (11) RePEc:nbr:nberwo:11380 Ultra High Frequency Volatility Estimation with Dependent Microstructure Noise (2005). National Bureau of Economic Research, Inc / NBER Working Papers (12) RePEc:nbr:nberwo:11578 Understanding the Effects of Government Spending on Consumption (2005). National Bureau of Economic Research, Inc / NBER Working Papers (13) RePEc:nuf:econwp:0505 Estimating quadratic variation when quoted prices jump by a constant increment (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (14) RePEc:nuf:econwp:0516 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (15) RePEc:nuf:econwp:0517 Stochastic Volatility (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (16) RePEc:nuf:econwp:0524 Outlier Detection in GARCH Models (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (17) RePEc:oxf:wpaper:240 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). University of Oxford, Department of Economics / Economics Series Working Papers (18) RePEc:red:issued:v:8:y:2005:i:2:p:420-451 Changing Beliefs and the Term Structure of Interest Rates: Cross-Equation Restrictions with Drifting Parameters (2005). Review of Economic Dynamics (19) RePEc:taf:apfiec:v:15:y:2005:i:2:p:121-135 Stochastic volatility forecasting and risk management (2005). Applied Financial Economics (20) RePEc:taf:apmtfi:v:12:y:2005:i:1:p:53-85 Stochastic Modelling of Temperature Variations with a View Towards Weather Derivatives (2005). Applied Mathematical Finance (21) RePEc:taf:eurjfi:v:11:y:2005:i:1:p:33-57 Forecasting variance using stochastic volatility and GARCH (2005). European Journal of Finance (22) RePEc:ubi:deawps:12 Asymmetric Multivariate Stochastic Volatility (2005). Universitat de les Illes Balears, Departament d'EconomÃa Aplicada / DEA Working Papers (23) RePEc:upf:upfgen:911 Understanding the Effects of Government Spending on Consumption (2005). Department of Economics and Business, Universitat Pompeu Fabra / Economics Working Papers (24) RePEc:vcu:wpaper:0505 The smooth transition autoregressive target zone model with the Gaussian stochastic volatility and TGARCH error terms with applications (2005). VCU School of Business, Department of Economics / Working Papers (25) RePEc:wpa:wuwpem:0501003 The Variance Ratio Statistic at large Horizons (2005). EconWPA / Econometrics (26) RePEc:wpa:wuwpem:0508015 The smooth transition autoregressive target zone model with the Gaussian stochastic volatility and TGARCH error terms with applications (2005). EconWPA / Econometrics (27) RePEc:wpa:wuwpem:0509006 Can fear beat hope? A story of GARCH-in-Mean-Level effects for Emerging Market Country Risks (2005). EconWPA / Econometrics (28) RePEc:wpa:wuwpfi:0510029 Time-varying Beta Risk of Pan-European Industry Portfolios: A Comparison of Alternative Modeling Techniques (2005). EconWPA / Finance (29) RePEc:zbw:bubdp1:4224 Ultra high frequency volatility estimation with dependent microstructure noise (2005). Deutsche Bundesbank, Research Centre / Discussion Paper Series 1: Economic Studies (30) RePEc:zbw:cauewp:3829 The Introduction of the Euro and its Effects on Investment Decisions (2005). Christian-Albrechts-University of Kiel, Department of Economics / Economics working papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||