|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

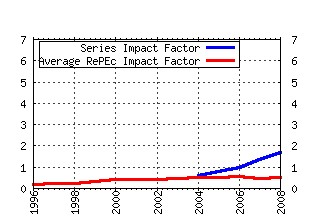

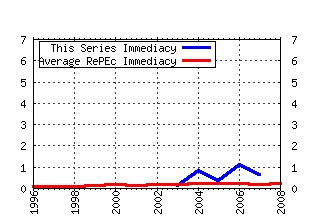

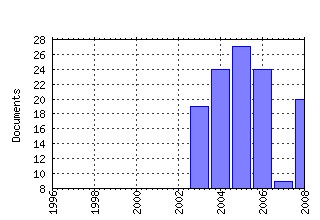

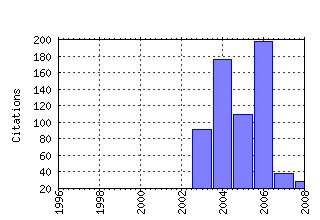

Journal of Financial Econometrics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:oup:jfinec:v:2:y:2004:i:1:p:1-37 Power and Bipower Variation with Stochastic Volatility and Jumps (2004). (2) RePEc:oup:jfinec:v:4:y:2006:i:4:p:537-572 Asymmetric Dynamics in the Correlations of Global Equity and Bond Returns (2006). (3) RePEc:oup:jfinec:v:4:y:2006:i:1:p:1-30 Econometrics of Testing for Jumps in Financial Economics Using Bipower Variation (2006). (4) RePEc:oup:jfinec:v:3:y:2005:i:4:p:456-499 The Relative Contribution of Jumps to Total Price Variance (2005). (5) RePEc:oup:jfinec:v:3:y:2005:i:4:p:525-554 A Realized Variance for the Whole Day Based on Intermittent High-Frequency Data (2005). (6) RePEc:oup:jfinec:v:4:y:2006:i:1:p:53-89 Value-at-Risk Prediction: A Comparison of Alternative Strategies (2006). (7) RePEc:oup:jfinec:v:2:y:2004:i:4:p:493-530 A New Approach to Markov-Switching GARCH Models (2004). (8) RePEc:oup:jfinec:v:5:y:2007:i:1:p:68-104 Integrated Covariance Estimation using High-frequency Data in the Presence of Noise (2007). (9) RePEc:oup:jfinec:v:2:y:2004:i:2:p:211-250 Mixed Normal Conditional Heteroskedasticity (2004). (10) RePEc:oup:jfinec:v:2:y:2004:i:1:p:130-168 On the Out-of-Sample Importance of Skewness and Asymmetric Dependence for Asset Allocation (2004). (11) RePEc:oup:jfinec:v:1:y:2003:i:1:p:26-54 Fourth Moment Structure of Multivariate GARCH Models (2003). (12) RePEc:oup:jfinec:v:2:y:2004:i:2:p:319-342 Persistence and Kurtosis in GARCH and Stochastic Volatility Models (2004). (13) RePEc:oup:jfinec:v:3:y:2005:i:4:p:555-577 Properties of Bias-Corrected Realized Variance Under Alternative Sampling Schemes (2005). (14) RePEc:oup:jfinec:v:1:y:2003:i:1:p:2-25 Dynamics of Trade-by-Trade Price Movements: Decomposition and Models (2003). (15) RePEc:oup:jfinec:v:4:y:2006:i:3:p:450-493 Stochastic Conditional Intensity Processes (2006). (16) RePEc:oup:jfinec:v:1:y:2003:i:2:p:159-188 Trades and Quotes: A Bivariate Point Process (2003). (17) RePEc:oup:jfinec:v:4:y:2006:i:3:p:353-384 Leverage and Volatility Feedback Effects in High-Frequency Data (2006). (18) RePEc:oup:jfinec:v:5:y:2007:i:1:p:31-67 Why Do Absolute Returns Predict Volatility So Well? (2007). (19) RePEc:oup:jfinec:v:7:y:2009:i:2:p:174-196 A Simple Approximate Long-Memory Model of Realized Volatility (2009). (20) RePEc:oup:jfinec:v:1:y:2003:i:1:p:96-125 Modeling the U.S. Short-Term Interest Rate by Mixture Autoregressive Processes (2003). (21) RePEc:oup:jfinec:v:3:y:2005:i:3:p:399-421 Autoregressive Conditional Kurtosis (2005). (22) RePEc:oup:jfinec:v:6:y:2008:i:3:p:326-360 Are There Structural Breaks in Realized Volatility? (2008). (23) RePEc:oup:jfinec:v:1:y:2003:i:2:p:272-289 The Robustness of the Conditional CAPM with Human Capital (2003). (24) RePEc:oup:jfinec:v:1:y:2003:i:3:p:445-470 The Local Whittle Estimator of Long-Memory Stochastic Volatility (2003). (25) RePEc:oup:jfinec:v:4:y:2006:i:3:p:413-449 Inequality Constraints in the Fractionally Integrated GARCH Model (2006). (26) RePEc:oup:jfinec:v:4:y:2006:i:2:p:238-274 Structural Breaks and Predictive Regression Models of Aggregate U.S. Stock Returns (2006). (27) RePEc:oup:jfinec:v:4:y:2006:i:2:p:275-309 The Generalized Hyperbolic Skew Students t-Distribution (2006). (28) RePEc:oup:jfinec:v:2:y:2004:i:4:p:531-564 Modeling the Conditional Covariance Between Stock and Bond Returns: A Multivariate GARCH Approach (2004). (29) RePEc:oup:jfinec:v:2:y:2004:i:4:p:477-492 Pessimistic Portfolio Allocation and Choquet Expected Utility (2004). (30) RePEc:oup:jfinec:v:6:y:2008:i:4:p:540-582 American Option Pricing Using GARCH Models and the Normal Inverse Gaussian Distribution (2008). (31) RePEc:oup:jfinec:v:2:y:2004:i:3:p:370-389 Asset Allocation by Variance Sensitivity Analysis (2004). (32) RePEc:oup:jfinec:v:4:y:2006:i:2:p:310-345 Empirical Comparisons in Short-Term Interest Rate Models Using Nonparametric Methods (2006). (33) RePEc:oup:jfinec:v:1:y:2003:i:1:p:55-95 Time Inhomogeneous Multiple Volatility Modeling (2003). (34) RePEc:oup:jfinec:v:2:y:2004:i:1:p:49-83 How to Forecast Long-Run Volatility: Regime Switching and the Estimation of Multifractal Processes (2004). (35) RePEc:oup:jfinec:v:1:y:2003:i:2:p:189-215 Assessing the Risk of Liquidity Suppliers on the Basis of Excess Demand Intensities (2003). (36) RePEc:oup:jfinec:v:4:y:2006:i:3:p:385-412 Dynamic Asymmetric GARCH (2006). (37) RePEc:oup:jfinec:v:4:y:2006:i:1:p:136-160 Incomplete Information, Heterogeneity, and Asset Pricing (2006). (38) RePEc:oup:jfinec:v:1:y:2003:i:3:p:365-419 A Closer Look at the Relation between GARCH and Stochastic Autoregressive Volatility (2003). (39) RePEc:oup:jfinec:v:2:y:2004:i:3:p:422-450 Nonparametric Tests for Positive Quadrant Dependence (2004). (40) RePEc:oup:jfinec:v:3:y:2005:i:3:p:372-398 Multivariate Lagrange Multiplier Tests for Fractional Integration (2005). (41) RePEc:oup:jfinec:v:2:y:2004:i:1:p:84-108 Backtesting Value-at-Risk: A Duration-Based Approach (2004). (42) RePEc:oup:jfinec:v:6:y:2008:i:4:p:407-458 Econometric Asset Pricing Modelling (2008). (43) RePEc:oup:jfinec:v:4:y:2006:i:3:p:494-530 Affine Models for Credit Risk Analysis (2006). (44) RePEc:oup:jfinec:v:1:y:2003:i:2:p:216-249 Using Multiple Imputation in the Analysis of Incomplete Observations in Finance (2003). (45) RePEc:oup:jfinec:v:4:y:2006:i:4:p:636-670 Long Memory and the Relation Between Implied and Realized Volatility (2006). (46) RePEc:oup:jfinec:v:4:y:2006:i:4:p:594-616 A Mixture Multiplicative Error Model for Realized Volatility (2006). (47) RePEc:oup:jfinec:v:3:y:2005:i:2:p:227-255 Nonparametric Inference of Value-at-Risk for Dependent Financial Returns (2005). (48) RePEc:oup:jfinec:v:8:y:2010:i:2:p:177-180 Separation in Cointegrated Systems (2010). (49) RePEc:oup:jfinec:v:5:y:2007:i:1:p:105-153 Switching VARMA Term Structure Models (2007). (50) RePEc:oup:jfinec:v:3:y:2005:i:3:p:422-441 The Stability of Factor Models of Interest Rates (2005). Recent citations received in: | 2008 | 2007 | 2006 | 2005 Recent citations received in: 2008 Recent citations received in: 2007 (1) RePEc:bfr:banfra:189 Multi-Lag Term Structure Models with Stochastic Risk Premia. (2007). Banque de France / Documents de Travail (2) RePEc:fir:econom:wp2007_04 Volatility Forecasting Using Explanatory Variables and Focused Selection Criteria (2007). Universita' degli Studi di Firenze, Dipartimento di Statistica G. Parenti / Econometrics Working Papers Archive (3) RePEc:knz:cofedp:0701 Dynamic Modeling of Large Dimensional Covariance Matrices (2007). Center of Finance and Econometrics, University of Konstanz / CoFE Discussion Paper (4) RePEc:knz:cofedp:0707 Estimating High-Frequency Based (Co-) Variances: A Unified Approach (2007). Center of Finance and Econometrics, University of Konstanz / CoFE Discussion Paper (5) RePEc:kyo:wpaper:634 Finite Sample Analysis of Weighted Realized Covariance with Noisy Asynchronous Observations (2007). Kyoto University, Institute of Economic Research / Working Papers (6) RePEc:osk:wpaper:0703 Test of Unbiasedness of the Integrated Covariance Estimation in the Presence of Noise (2007). Osaka University, Graduate School of Economics and Osaka School of International Public Policy (OSIPP) / Discussion Papers in Economics and Business Recent citations received in: 2006 (1) RePEc:cam:camdae:0649 Time-Varying Quantiles (2006). Faculty of Economics (formerly DAE), University of Cambridge / Cambridge Working Papers in Economics (2) RePEc:cfr:cefirw:w0092 Dynamic modeling under linear-exponential loss (2006). Center for Economic and Financial Research / CEFIR Working Papers (3) RePEc:cor:louvco:2006080 Modelling financial high frequency data using point processes (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (4) RePEc:cor:louvco:2006089 The information content of the Bond-Equity Yield Ratio: better than a random walk? (2006). Université catholique de Louvain, Center for Operations Research and Econometrics (CORE) / Discussion Papers (5) RePEc:cpr:ceprdp:5734 Optimal Currency Shares in International Reserves: The Impact of the Euro and the Prospects for the Dollar (2006). C.E.P.R. Discussion Papers / CEPR Discussion Papers (6) RePEc:ctl:louvec:2006039 Modelling Financial High Frequency Data Using Point Processes (2006). Université catholique de Louvain, Département des Sciences Economiques / Université catholique de Louvain, Département des Sciences Economiques Workin (7) RePEc:dgr:uvatin:20050044 The Euro Introduction and Non-Euro Currencies (2006). Tinbergen Institute / Tinbergen Institute Discussion Papers (8) RePEc:dul:wpaper:06-07rs Sector diversification during crises: a European perspective (2006). Université libre de Bruxelles, Department of Applied Economics (DULBEA) / Working Papers DULBEA (9) RePEc:eab:microe:1143 Multivariate Stochastic Volatility (2006). East Asian Bureau of Economic Research / Microeconomics Working Papers (10) RePEc:ebl:ecbull:v:3:y:2006:i:15:p:1-14 A new proxy of the average volatility of a basket of returns: A Monte Carlo study (2006). Economics Bulletin (11) RePEc:ecb:ecbwps:20060683 Financial integration of new EU Member States (2006). European Central Bank / Working Paper Series (12) RePEc:ecb:ecbwps:20060694 Optimal currency shares in international reserves - the impact of the euro and the prospects for the dollar (2006). European Central Bank / Working Paper Series (13) RePEc:ecl:ohidic:2007-2 Affine Term Structure Models (2006). Ohio State University, Charles A. Dice Center for Research in Financial Economics / Working Paper Series (14) RePEc:fip:fedgfe:2006-35 Realized jumps on financial markets and predicting credit spreads (2006). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (15) RePEc:hhs:hastef:0646 An introduction to univariate GARCH models (2006). Stockholm School of Economics / Working Paper Series in Economics and Finance (16) RePEc:iis:dispap:iiisdp132 Have European Stocks Become More Volatile? An Empirical Investigation of Idiosyncratic and Market Risk in the Euro Area (2006). IIIS / The Institute for International Integration Studies Discussion Paper Series (17) RePEc:iis:dispap:iiisdp139 The Euro and Financial Integration (2006). IIIS / The Institute for International Integration Studies Discussion Paper Series (18) RePEc:man:cgbcrp:77 Periodic Dynamic Conditional Correlations between Stock Markets in Europe and the US (2006). The School of Economic Studies, The Univeristy of Manchester / Centre for Growth and Business Cycle Research Discussion Paper Series (19) RePEc:man:sespap:0629 Periodic Dynamic Conditional Correlations between Stock Markets in Europe and the US (2006). School of Economics, The University of Manchester / The School of Economics Discussion Paper Series (20) RePEc:nbr:nberwo:12333 Optimal Currency Shares in International Reserves: The Impact of the Euro and the Prospects for the Dollar (2006). National Bureau of Economic Research, Inc / NBER Working Papers (21) RePEc:nuf:econwp:0506 Limit theorems for bipower variation in financial econometrics (2006). Economics Group, Nuffield College, University of Oxford / Economics Papers (22) RePEc:nuf:econwp:0603 Designing realised kernels to measure the ex-post variation of equity prices in the presence of noise (2006). Economics Group, Nuffield College, University of Oxford / Economics Papers (23) RePEc:nus:nusewp:wp0603 The Persistence and Predictive Power of the Dividend-Price Ratio (2006). National University of Singapore, Department of Economics / Departmental Working Papers (24) RePEc:oxf:wpaper:264 Designing realised kernels to measure the ex-post variation of equity prices in the presence of noise (2006). University of Oxford, Department of Economics / Economics Series Working Papers (25) RePEc:pra:mprapa:189 An Asymmetric Block Dynamic Conditional Correlation Multivariate GARCH Model (2006). University Library of Munich, Germany / MPRA Paper (26) RePEc:rut:rutres:200620 Predictive Density Estimators for Daily Volatility Based on the Use of Realized Measures (2006). Rutgers University, Department of Economics / Departmental Working Papers (27) RePEc:ven:wpaper:2006_53 A generalized Dynamic Conditional Correlation Model for Portfolio Risk Evaluation (2006). University of Venice Ca' Foscari, Department of Economics / Working Papers Recent citations received in: 2005 (1) RePEc:cfs:cfswop:wp200502 Practical Volatility and Correlation Modeling for Financial Market Risk Management (2005). Center for Financial Studies / CFS Working Paper Series (2) RePEc:crt:wpaper:0521 Conditional autoregressive valu at risk by regression quantile: Estimatingmarket risk for major stock markets (2005). University of Crete, Department of Economics / Working Papers (3) RePEc:dgr:uvatin:20050002 Model-based Measurement of Actual Volatility in High-Frequency Data (2005). Tinbergen Institute / Tinbergen Institute Discussion Papers (4) RePEc:fip:fedgfe:2005-63 Explaining credit default swap spreads with the equity volatility and jump risks of individual firms (2005). Board of Governors of the Federal Reserve System (U.S.) / Finance and Economics Discussion Series (5) RePEc:nbr:nberwo:11069 Practical Volatility and Correlation Modeling for Financial Market Risk Management (2005). National Bureau of Economic Research, Inc / NBER Working Papers (6) RePEc:nuf:econwp:0516 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (7) RePEc:oxf:wpaper:240 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). University of Oxford, Department of Economics / Economics Series Working Papers (8) RePEc:pen:papers:05-007 Practical Volatility and Correlation Modeling for Financial Market Risk Management (2005). Penn Institute for Economic Research, Department of Economics, University of Pennsylvania / PIER Working Paper Archive (9) RePEc:qed:wpaper:1186 The Implied-Realized Volatility Relation with Jumps in Underlying Asset Prices (2005). Queen's University, Department of Economics / Working Papers (10) RePEc:qed:wpaper:1187 Forecasting Exchange Rate Volatility in the Presence of Jumps (2005). Queen's University, Department of Economics / Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||