|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

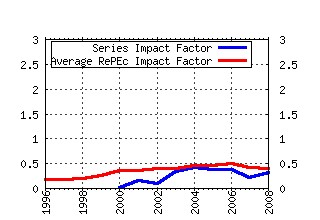

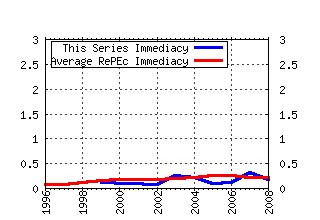

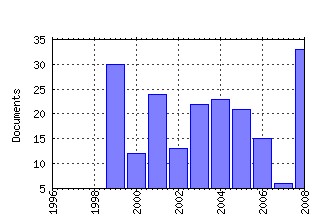

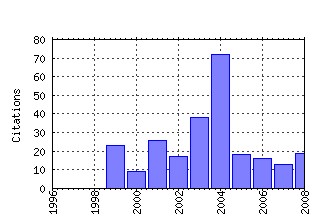

Oxford Financial Research Centre / OFRC Working Papers Series Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:sbs:wpsefe:2004fe21 A Central Limit Theorem for Realised Power and Bipower Variations of Continuous Semimartingales (2004). (2) RePEc:sbs:wpsefe:2003fe08 Equilibrium Analysis, Banking and Financial Instability (2003). (3) RePEc:sbs:wpsefe:2004fe05 A Model to Analyse Financial Fragility: Applications (2004). (4) RePEc:sbs:wpsefe:2007fe03 A Note on the Central Limit Theorem for Bipower Variation of General Functions (2007). (5) RePEc:sbs:wpsefe:2001fe11 Ownership and Control of German Corporations (2001). (6) RePEc:sbs:wpsefe:1999fe09 Finance, Investment and Growth (1999). (7) RePEc:sbs:wpsefe:2004fe02 Likelihood-based estimation of latent generalised ARCH structures (2004). (8) RePEc:sbs:wpsefe:2004fe20 Regular and Modified Kernel-Based Estimators of Integrated Variance: The Case with Independent Noise (2004). (9) RePEc:sbs:wpsefe:2006fe01 Evaluation of macroeconomic models for financial stability analysis (2006). (10) RePEc:sbs:wpsefe:2005fe05 Estimating quadratic variation when quoted prices jump by a constant increment (2005). (11) RePEc:sbs:wpsefe:2001fe15 Sources of Funds and Investment Strategies of Venture Capital Funds: Evidence from Germany, Israel, Japan and the UK (2001). (12) RePEc:sbs:wpsefe:2005fe04 Why are Securitization Issues Tranched? (2005). (13) RePEc:sbs:wpsefe:1999fe08 How Do Financial Systems Affect Economic Performance? (1999). (14) RePEc:sbs:wpsefe:2006fe09 Searching for a Metric for Financial Stability (2006). (15) RePEc:sbs:wpsefe:2002mf05 Variational Sums and Power Variation: a unifying approach to model selection and estimation in semimartingale models (2002). (16) RePEc:sbs:wpsefe:2008fe29 Multivariate realised kernels: consistent positive semi-definite estimators of the covariation of equity prices with noise and non-synchronous trading (2008). (17) RePEc:sbs:wpsefe:2003fe03 Equilibrium Analysis, Banking, Contagion and Financial Fragility (2003). (18) RePEc:sbs:wpsefe:2003fe13 A Model to Analyse Financial Fragility (2003). (19) RePEc:sbs:wpsefe:2003fe06 Procyclicality and the new Basel Accord - Banks choice of loan rating system (2003). (20) RePEc:sbs:wpsefe:2004fe10 Financial Liberalisation and Capital Regulation in Open Economies (2004). (21) RePEc:sbs:wpsefe:2004fe11 A Risk Assessment Model for Banks (2004). (22) RePEc:sbs:wpsefe:2001fe02 Business Groups and Risk Sharing around the World (2001). (23) RePEc:sbs:wpsefe:2003fe11 Multinational Bank Capital Regulation with Deposit Insurance and Diversification Effects (2003). (24) RePEc:sbs:wpsefe:2008fe25 An Econometric Analysis of Modulated Realised Covariance,

Regression and Correlation in Noisy Diffusion Models (2008). (25) RePEc:sbs:wpsefe:2008fe21 Copula-Based Models for Financial Time Series (2008). (26) RePEc:sbs:wpsefe:2001fe01 Credit Derivatives, Disintermediation and Investment Decisions (2000). (27) RePEc:sbs:wpsefe:2005fe18 Commitment to Overinvest and Price Informativeness (2005). (28) RePEc:sbs:wpsefe:1999fe01 Who Disciplines Management in Poorly Performing Companies? (1999). (29) RePEc:sbs:wpsefe:2004fe14 The Demise of Investment-Banking Partnerships: Theory and Evidence. (2004). (30) RePEc:sbs:wpsefe:2003mf05 Estimation of Integrated Volatility in Stochastic Volatility Models (2003). (31) RePEc:sbs:wpsefe:2008fe22 Evaluating Volatility and Correlation Forecasts (2008). (32) RePEc:sbs:wpsefe:2003fe02 Partnership Firms, Reputation and Human Capital (2003). (33) RePEc:sbs:wpsefe:2004fe08 Is Deposit Insurance a Good Thing, and If So, Who Should Pay for It? (2004). (34) RePEc:sbs:wpsefe:2002mf04 Distinguished Limits of Levy-Stable Processes, and Applications to Option Pricing (2002). (35) RePEc:sbs:wpsefe:2004fe04 Cancellation and uncertainty aversion on limit order books (2004). (36) RePEc:sbs:wpsefe:2004fe15 Global Uniqueness and Money Non-neutrality in a Walrasian Dynamics without Rational Expectations (2004). (37) RePEc:sbs:wpsefe:2000fe04 Has the introduction of bookbuilding increased the efficiency of international IPOs? (2000). (38) RePEc:sbs:wpsefe:2007fe02 Feasible inference for realised variance in the presence of jumps (2007). (39) RePEc:sbs:wpsefe:2002fe06 Evidence of Information Spillovers in the Production of Investment Banking Services (2002). (40) RePEc:sbs:wpsefe:2005fe02 Interbank Competition with Costly Screening (2005). (41) RePEc:sbs:wpsefe:2001fe05 A Theory of the Syndicate: Form Follows Function (2001). (42) RePEc:sbs:wpsefe:1999mf09 Optimal Hedging of Options with Small but Arbitrary Transaction Cost Structure (1999). (43) RePEc:sbs:wpsefe:2004fe18 A Time Series Analysis of Financial Fragility in the UK Banking System (2004). (44) RePEc:sbs:wpsefe:2000mf01 Non-Gaussian OU based models and some of their uses in financial economics (2000). (45) RePEc:sbs:wpsefe:2002mf03 Analytical Comparisons of Option prices in Stochastic Volatility Models (2002). (46) RePEc:sbs:wpsefe:2004fe03 A feasible central limit theory for realised volatility under leverage (2004). (47) RePEc:sbs:wpsefe:2001mf02 From market games to real-world markets (2001). (48) RePEc:sbs:wpsefe:2000fe03 Firm Value and Managerial Incentives: A Stochastic Frontier Approach (2000). (49) repec:sbs:wpsefe:2002fe07 (). (50) RePEc:sbs:wpsefe:2003mf08 Purely discontinuous Levy processes and power variation: inference for integrated volatility and the scale parameter (2003). Recent citations received in: | 2008 | 2007 | 2006 | 2005 Recent citations received in: 2008 (1) RePEc:ams:ndfwpp:08-10 Out-of-sample comparison of copula specifications in multivariate density forecasts (2008). Universiteit van Amsterdam, Center for Nonlinear Dynamics in Economics and Finance / CeNDEF Working Papers (2) RePEc:bla:randje:v:39:y:2008:i:4:p:1042-1058 Price-increasing competition (2008). RAND Journal of Economics (3) RePEc:cpr:ceprdp:7080 The Regulation of Entry: A Survey (2008). C.E.P.R. Discussion Papers / CEPR Discussion Papers (4) RePEc:cte:wsrepe:ws086321 Copulas in finance and insurance (2008). Universidad Carlos III, Departamento de EstadÃstica y EconometrÃa / Statistics and Econometrics Working Papers (5) RePEc:nbr:nberwo:14463 An Arbitrage-Free Generalized Nelson-Siegel Term Structure Model (2008). National Bureau of Economic Research, Inc / NBER Working Papers (6) RePEc:oxf:wpaper:397 Multivariate realised kernels: consistent positive semin-definite estimators of the covariation of equity prices with noise and non-synchronous trading (2008). University of Oxford, Department of Economics / Economics Series Working Papers Recent citations received in: 2007 (1) RePEc:aah:create:2007-42 Power variation for Gaussian processes with stationary increments (2007). School of Economics and Management, University of Aarhus / CREATES Research Papers (2) RePEc:cep:stiecm:/2007/523 Inference about Realized Volatility using Infill Subsampling (2007). Suntory and Toyota International Centres for Economics and Related Disciplines, LSE / STICERD - Econometrics Paper Series Recent citations received in: 2006 (1) RePEc:col:000094:002543 EL RIESGO DE MERCADO DE LA DEUDA PÃBLICA:¿UNA RESTRICCIÃN A LA POLÃTICA MONETARIA?EL CASO COLOMBIANO (2006). TITULARIZADORA COLOMBIANA / INFORMES (2) RePEc:dnb:dnbwpp:119 Modelling Scenario Analysis and Macro Stress-testing (2006). Netherlands Central Bank, Research Department / DNB Working Papers Recent citations received in: 2005 (1) RePEc:nuf:econwp:0516 Variation, jumps, market frictions and high frequency data in financial econometrics (2005). Economics Group, Nuffield College, University of Oxford / Economics Papers (2) RePEc:oxf:wpaper:230 Explaining Launch Spreads on Structured Bonds (2005). University of Oxford, Department of Economics / Economics Series Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||