|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

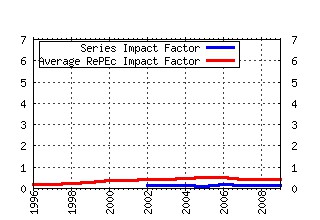

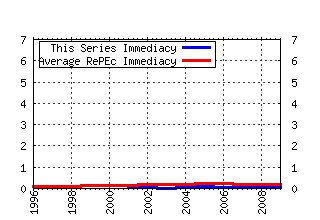

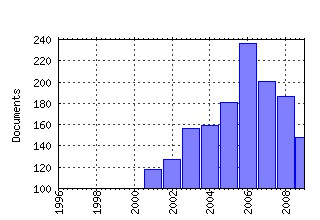

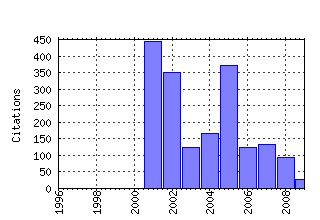

Journal of the American Statistical Association Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:bes:jnlasa:v:96:y:2001:m:march:p:42-55 The Distribution of Realized Exchange Rate Volatility (2001). (2) RePEc:bes:jnlasa:v:97:y:2002:m:december:p:1167-1179 Forecasting Using Principal Components From a Large Number of Predictors (2002). (3) RePEc:bes:jnlasa:v:100:y:2005:p:1394-1411 A Tale of Two Time Scales: Determining Integrated Volatility With Noisy High-Frequency Data (2005). (4) RePEc:bes:jnlasa:v:100:y:2005:p:830-840 The Generalized Dynamic Factor Model: One-Sided Estimation and Forecasting (2005). (5) RePEc:bes:jnlasa:v:96:y:2001:m:march:p:270-281 Marginal Likelihood From the Metropolis-Hastings Output (2001). (6) RePEc:bes:jnlasa:v:97:y:2002:m:march:p:284-292 Bootstrap Tests for Distributional Treatment Effects in Instrumental Variable Models (2002). (7) RePEc:bes:jnlasa:v:99:y:2004:p:1015-1026 Cross-Validation and the Estimation of Conditional Probability Densities (2004). (8) RePEc:bes:jnlasa:v:102:y:2007:m:june:p:432-441 Disability and Employment: Reevaluating the Evidence in Light of Reporting Errors (2007). (9) RePEc:bes:jnlasa:v:97:y:2002:m:september:p:663-673 Accounting for the Black-White Wealth Gap: A Nonparametric Approach (2002). (10) RePEc:bes:jnlasa:v:102:y:2007:m:june:p:603-617 Determining the Number of Factors in the General Dynamic Factor Model (2007). (11) RePEc:bes:jnlasa:v:96:y:2001:m:december:p:1348-1360 Variable Selection via Nonconcave Penalized Likelihood and its Oracle Properties (2001). (12) RePEc:bes:jnlasa:v:101:y:2006:p:1418-1429 The Adaptive Lasso and Its Oracle Properties (2006). (13) RePEc:bes:jnlasa:v:101:y:2006:p:980-990 Quantile Autoregression (2006). (14) RePEc:bes:jnlasa:v:96:y:2001:m:march:p:194-209 Markov Chain Monte Carlo Estimation of Classical and Dynamic Switching and Mixture Models (2001). (15) RePEc:bes:jnlasa:v:97:y:2002:m:september:p:872-882 Three-Step Censored Quantile Regression and Extramarital Affairs (2002). (16) RePEc:bes:jnlasa:v:103:y:2008:m:march:p:410-423 Mixtures of g Priors for Bayesian Variable Selection (2008). (17) RePEc:bes:jnlasa:v:103:i:484:y:2008:p:1481-1495 Multiple Inference and Gender Differences in the Effects of Early Intervention: A Reevaluation of the Abecedarian, Perry Preschool, and Early Training Projects (2008). (18) RePEc:bes:jnlasa:v:99:y:2004:p:854-866 Causal Inference With General Treatment Regimes: Generalizing the Propensity Score (2004). (19) RePEc:bes:jnlasa:v:96:y:2001:m:march:p:12-19 Investigating Child Mortality in Malawi Using Family and Community Random Effects: A Bayesian Analysis (2001). (20) RePEc:bes:jnlasa:v:99:y:2004:p:799-804 Getting It Right: Joint Distribution Tests of Posterior Simulators (2004). (21) RePEc:bes:jnlasa:v:103:i:483:y:2008:p:1028-1038 Imputing Risk Tolerance From Survey Responses (2008). (22) RePEc:bes:jnlasa:v:97:y:2002:m:june:p:432-442 Multiple-Output Production With Undesirable Outputs: An Application to Nitrogen Surplus in Agriculture (2002). (23) RePEc:bes:jnlasa:v:105:i:490:y:2010:p:493-505 Synthetic Control Methods for Comparative Case Studies: Estimating the Effect of Californiaâs Tobacco Control Program (2010). (24) RePEc:bes:jnlasa:v:102:y:2007:p:359-378 Strictly Proper Scoring Rules, Prediction, and Estimation (2007). (25) RePEc:bes:jnlasa:v:102:y:2007:m:december:p:1172-1184 Testing Forecast Optimality Under Unknown Loss (2007). (26) RePEc:bes:jnlasa:v:98:y:2003:p:629-642 Semiparametric Estimation of Multivariate Fractional Cointegration (2003). (27) RePEc:bes:jnlasa:v:97:y:2002:m:december:p:1141-1153 Parsimonious Covariance Matrix Estimation for Longitudinal Data (2002). (28) RePEc:bes:jnlasa:v:96:y:2001:m:june:p:640-652 Goodness-of-Fit Tests for Parametric Regression Models (2001). (29) RePEc:bes:jnlasa:v:99:y:2004:p:156-168 Monte Carlo Smoothing for Nonlinear Time Series (2004). (30) RePEc:bes:jnlasa:v:101:y:2006:p:1228-1240 Efficient Estimation of Semiparametric Multivariate Copula Models (2006). (31) RePEc:bes:jnlasa:v:96:y:2001:m:december:p:1151-1160 Empirical Bayes Analysis of a Microarray Experiment (2001). (32) RePEc:bes:jnlasa:v:100:y:2005:p:532-544 Diagnostic Checking in ARMA Models With Uncorrelated Errors (2005). (33) RePEc:bes:jnlasa:v:100:y:2005:p:6-16 Weather Forecasting for Weather Derivatives (2005). (34) RePEc:bes:jnlasa:v:98:y:2003:p:299-323 Principal Stratification Approach to Broken Randomized Experiments: A Case Study of School Choice Vouchers in New York City (2003). (35) RePEc:bes:jnlasa:v:100:y:2005:p:1226-1237 Quantiles for Counts (2005). (36) RePEc:bes:jnlasa:v:99:y:2004:p:673-686 Stable and Efficient Multiple Smoothing Parameter Estimation for Generalized Additive Models (2004). (37) RePEc:bes:jnlasa:v:100:y:2005:p:545-553 Bootstrapping Unit Root Tests for Autoregressive Time Series (2005). (38) RePEc:bes:jnlasa:v:96:y:2001:m:december:p:1387-1396 A Note on the Efficiency of Sandwich Covariance Matrix Estimation (2001). (39) RePEc:bes:jnlasa:v:99:y:2004:p:775-787 Unit Root Quantile Autoregression Inference (2004). (40) RePEc:bes:jnlasa:v:97:y:2002:m:june:p:601-610 A Powerful Portmanteau Test of Lack of Fit for Time Series (2002). (41) RePEc:bes:jnlasa:v:96:y:2001:m:june:p:500-509 Are Points in Tennis Independent and Identically Distributed? Evidence From a Dynamic Binary Panel Data Model (2001). (42) RePEc:bes:jnlasa:v:96:y:2001:m:june:p:458-468 Reappraising Medfly Longevity: A Quantile Regression Survival Analysis (2001). (43) RePEc:bes:jnlasa:v:102:y:2007:m:december:p:1349-1362 Multi-Scale Jump and Volatility Analysis for High-Frequency Financial Data (2007). (44) RePEc:bes:jnlasa:v:100:y:2005:p:212-221 Nonparametric Identification and Estimation of a Censored Location-Scale Regression Model (2005). (45) RePEc:bes:jnlasa:v:98:y:2003:p:135-146 On Additive Conditional Quantiles With High Dimensional Covariates (2003). (46) RePEc:bes:jnlasa:v:100:y:2005:p:94-108 Exact and Approximate Stepdown Methods for Multiple Hypothesis Testing (2005). (47) RePEc:bes:jnlasa:v:97:y:2002:m:march:p:77-87 Comparison of Discrimination Methods for the Classification of Tumors Using Gene Expression Data (2002). (48) RePEc:bes:jnlasa:v:99:y:2004:p:205-215 An ANOVA Model for Dependent Random Measures (2004). (49) RePEc:bes:jnlasa:v:96:y:2001:m:june:p:440-448 Marginal Structural Models to Estimate the Joint Causal Effect of Nonrandomized Treatments (2001). (50) RePEc:bes:jnlasa:v:97:y:2002:m:june:p:611-631 Model-Based Clustering, Discriminant Analysis, and Density Estimation (2002). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:cfs:cfswop:wp200918 Modelling and Forecasting Liquidity Supply Using Semiparametric Factor Dynamics (2009). CFS Working Paper Series (2) RePEc:dgr:kubcen:200929 Estimating Extreme Bivariate Quantile Regions (2009). Discussion Paper (3) RePEc:nbr:nberwo:14860 Complementarity and Aggregate Implications of Assortative Matching: A Nonparametric Analysis (2009). NBER Working Papers (4) RePEc:spr:alstar:v:93:y:2009:i:4:p:387-402 Dynamic semiparametric factor models in risk neutral density estimation (2009). AStA Advances in Statistical Analysis (5) RePEc:spr:testjl:v:18:y:2009:i:3:p:452-454 Comments on: A review on empirical likelihood methods for regression (2009). TEST: An Official Journal of the Spanish Society of Statistics and Operations Research (6) RePEc:zbw:sfb475:200911 Interventions in ingarch processes (2009). Technical Reports Recent citations received in: 2008 (1) RePEc:eca:wpaper:2008_042 Multivariate quantiles and multiple-output regression quantiles: from L1 optimization to halfspace depth (2008). Working Papers ECARES (2) RePEc:jss:jstsof:27:i06 Censored Quantile Regression Redux (2008). Journal of Statistical Software (3) RePEc:pra:mprapa:6773 On the Effect of Prior Assumptions in Bayesian Model Averaging with Applications to Growth Regression (2008). MPRA Paper (4) RePEc:wbk:wbrwps:4759 Cash transfers, behavioral changes, and cognitive development in early childhood : evidence from a randomized experiment (2008). Policy Research Working Paper Series (5) RePEc:xrp:wpaper:xreap2008-09 A priori ratemaking using bivariate poisson regression models (2008). Working Papers (6) RePEc:zbw:sfb475:200822 Practical considerations for optimal designs in clinical dose finding studies (2008). Technical Reports (7) RePEc:zbw:sfb475:200826 A geometric characterization of c-optimal designs for heteroscedastic regression (2008). Technical Reports Recent citations received in: 2007 (1) RePEc:aah:create:2007-29 A Vector Autoregressive Model for Electricity Prices Subject to Long Memory and Regime Switching (2007). CREATES Research Papers (2) RePEc:bdi:wptemi:td_631_07 New Eurocoin: Tracking Economic Growth in Real Time (2007). Temi di discussione (Economic working papers) (3) RePEc:cpb:discus:92 On the optimality of expert-adjusted forecasts (2007). CPB Discussion Paper (4) RePEc:ecb:ecbwps:20070836 Reporting biases and survey results - evidence from European professional forecasters (2007). Working Paper Series (5) RePEc:ese:iserwp:2007-15 Estimating income poverty in the presence of measurement error and missing data problems (2007). ISER Working Paper Series (6) RePEc:mtn:ancoec:070102 Doing thousands of hypothesis tests at the same time (2007). Metron - International Journal of Statistics (7) RePEc:ner:leuven:urn:hdl:123456789/175476 Estimation and decomposition of downside risk for portfolios with non-normal returns. (2007). Open Access publications from Katholieke Universiteit Leuven (8) RePEc:pra:mprapa:862 Estimation of an Occupational Choice Model when Occupations are Misclassified (2007). MPRA Paper (9) RePEc:udb:wpaper:uwec-2007-25-p Default Priors and Predictive Performance in Bayesian Model Averaging, with Application to Growth Determinants (2007). Working Papers Recent citations received in: 2006 (1) RePEc:cam:camdae:0649 Time-Varying Quantiles (2006). Cambridge Working Papers in Economics (2) RePEc:cor:louvco:2006077 Intradaily seasonality of returns distribution. A quantile regression approach and intradaily VaR estimation (2006). CORE Discussion Papers (3) RePEc:cte:werepe:we064111 A CONSISTENT SPECIFICATION TEST FOR MODELS DEFINED BY CONDITIONAL MOMENT RESTRICTIONS (2006). Economics Working Papers (4) RePEc:dgr:uvatin:20060105 Extracting Business Cycles using Semi-parametric Time-varying Spectra with Applications to US Macroeconomic Time Series (2006). Tinbergen Institute Discussion Papers (5) RePEc:ebl:ecbull:v:3:y:2006:i:5:p:1-6 Omitted Asymmetric Persistence and Conditional Heteroskedasticity (2006). Economics Bulletin (6) RePEc:ecb:ecbwps:20060667 The behaviour of the real exchange rate: evidence from regression quantiles. (2006). Working Paper Series (7) RePEc:ecl:harjfk:rwp06-048 Who Misvotes? The Effect of Differential Cognition Costs on Election Outcomes (2006). Working Paper Series (8) RePEc:fgv:epgewp:631 Debt ceiling and fiscal sustainability in Brazil: a quantile autoregression approach (2006). Economics Working Papers (Ensaios Economicos da EPGE) (9) RePEc:hum:wpaper:sfb649dp2006-075 Inhomogeneous Dependency Modelling with Time Varying Copulae (2006). SFB 649 Discussion Papers (10) RePEc:spr:testjl:v:15:y:2006:i:2:p:271-344 Regularization in statistics (2006). TEST: An Official Journal of the Spanish Society of Statistics and Operations Research (11) RePEc:zbw:sfb475:200603 Robust Learning from Bites for Data Mining (2006). Technical Reports Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||