|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

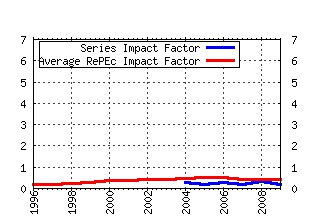

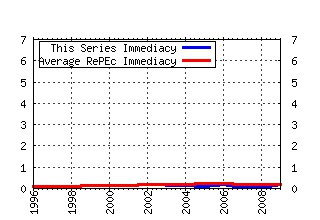

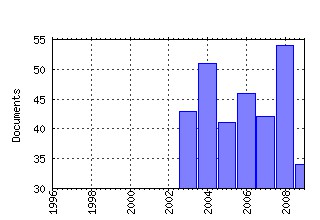

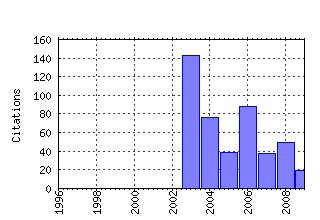

Journal of Time Series Analysis Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:bla:jtsera:v:24:y:2003:i:4:p:379-400 A Sieve Bootstrap For The Test Of A Unit Root (2003). (2) RePEc:bla:jtsera:v:24:y:2003:i:2:p:193-220 SEARCHING FOR ADDITIVE OUTLIERS IN NONSTATIONARY TIME SERIES* (2003). (3) RePEc:bla:jtsera:v:29:y:2008:i:1:p:163-185 Fractional integration and structural breaks at unknown periods of time (2008). (4) RePEc:bla:jtsera:v:27:y:2006:i:3:p:381-409 A Stationarity Test in the Presence of an Unknown Number of Smooth Breaks (2006). (5) RePEc:bla:jtsera:v:25:y:2004:i:5:p:649-669 A Dependence Metric for Possibly Nonlinear Processes (2004). (6) RePEc:bla:jtsera:v:28:y:2007:i:3:p:408-433 CUSUM of Squares-Based Tests for a Change in Persistence (2007). (7) RePEc:bla:jtsera:v:27:y:2006:i:1:p:51-60 Uniform Limit Theory for Stationary Autoregression (2006). (8) RePEc:bla:jtsera:v:24:y:2003:i:3:p:345-378 Gaussian Semi-parametric Estimation of Fractional Cointegration (2003). (9) RePEc:bla:jtsera:v:24:y:2003:i:1:p:85-98 Filtering and smoothing of state vector for diffuse state-space models (2003). (10) RePEc:bla:jtsera:v:24:y:2003:i:1:p:45-63 On the efficacy of simulated maximum likelihood for estimating the parameters of stochastic differential Equations* (2003). (11) RePEc:bla:jtsera:v:24:y:2003:i:2:p:237-252 ON THE DETERMINATION OF THE NUMBER OF REGIMES IN MARKOV-SWITCHING AUTOREGRESSIVE MODELS (2003). (12) RePEc:bla:jtsera:v:26:y:2005:i:1:p:123-133 Unit-root testing against the alternative hypothesis of up to m structural breaks (2005). (13) RePEc:bla:jtsera:v:29:y:2008:i:2:p:371-401 Bootstrap Unit-Root Tests: Comparison and Extensions (2008). (14) RePEc:bla:jtsera:v:25:y:2004:i:1:p:27-32 Error Correction Models for Fractionally Cointegrated Time Series (2004). (15) RePEc:bla:jtsera:v:27:y:2006:i:4:p:545-576 Range Unit-Root (RUR) Tests: Robust against Nonlinearities, Error Distributions, Structural Breaks and Outliers (2006). (16) RePEc:bla:jtsera:v:24:y:2003:i:4:p:461-482 Diagnostic Checking in a Flexible Nonlinear Time Series Model (2003). (17) RePEc:bla:jtsera:v:27:y:2006:i:5:p:671-684 Spurious Regression Under Broken-Trend Stationarity (2006). (18) RePEc:bla:jtsera:v:25:y:2004:i:5:p:701-722 Analysis of low count time series data by poisson autoregression (2004). (19) RePEc:bla:jtsera:v:27:y:2006:i:2:p:289-308 Inference in Autoregression under Heteroskedasticity (2006). (20) RePEc:bla:jtsera:v:27:y:2006:i:2:p:211-251 Consistent estimation of the memory parameter for nonlinear time series (2006). (21) RePEc:bla:jtsera:v:24:y:2003:i:1:p:99-126 Bootstrapping unit root tests for integrated processes (2003). (22) RePEc:bla:jtsera:v:25:y:2004:i:4:p:449-465 Bootstrap predictive inference for ARIMA processes (2004). (23) RePEc:bla:jtsera:v:27:y:2006:i:3:p:347-365 Dynamics of Model Overfitting Measured in terms of Autoregressive Roots (2006). (24) RePEc:bla:jtsera:v:30:y:2009:i:2:p:208-238 A parametric estimation method for dynamic factor models of large dimensions (2009). (25) RePEc:bla:jtsera:v:27:y:2006:i:5:p:753-766 Joint Determination of the State Dimension and Autoregressive Order for Models with Markov Regime Switching (2006). (26) RePEc:bla:jtsera:v:25:y:2004:i:2:p:301-313 Assessment of Local Influence in GARCH Processes (2004). (27) RePEc:bla:jtsera:v:24:y:2003:i:5:p:539-551 Testing for Linear Trend with Application to Relative Primary Commodity Prices (2003). (28) RePEc:bla:jtsera:v:28:y:2007:i:4:p:471-497 Effects of outliers on the identification and estimation of GARCH models (2007). (29) RePEc:bla:jtsera:v:26:y:2005:i:2:p:185-210 Blockwise empirical entropy tests for time series regressions (2005). (30) RePEc:bla:jtsera:v:28:y:2007:i:5:p:763-782 Modelling the Dynamic Dependence Structure in Multivariate Financial Time Series (2007). (31) RePEc:bla:jtsera:v:25:y:2004:i:3:p:409-417 Asymmetric adjustment and smooth transitions: a combination of some unit root tests (2004). (32) RePEc:bla:jtsera:v:25:y:2004:i:2:p:159-172 Some comments on specification tests in nonparametric absolutely regular processes (2004). (33) RePEc:bla:jtsera:v:24:y:2003:i:4:p:423-439 Reducing size distortions of parametric stationarity tests (2003). (34) RePEc:bla:jtsera:v:27:y:2006:i:4:p:477-503 Structural Laplace Transform and Compound Autoregressive Models (2006). (35) RePEc:bla:jtsera:v:29:y:2008:i:3:p:453-475 Stability of nonlinear AR-GARCH models (2008). (36) RePEc:bla:jtsera:v:24:y:2003:i:1:p:65-84 Testing for serial dependence in time series models of counts (2003). (37) RePEc:bla:jtsera:v:27:y:2006:i:5:p:725-738 Modelling Count Data Time Series with Markov Processes Based on Binomial Thinning (2006). (38) RePEc:bla:jtsera:v:25:y:2004:i:2:p:265-282 On the Autocorrelation Properties of Long-Memory GARCH Processes (2004). (39) RePEc:bla:jtsera:v:25:y:2004:i:5:p:691-700 A joint test of fractional integration and structural breaks at a known period of time (2004). (40) RePEc:bla:jtsera:v:25:y:2004:i:1:p:33-53 Seasonal Unit Root Tests Under Structural Breaks* (2004). (41) RePEc:bla:jtsera:v:27:y:2006:i:5:p:703-723 Tests for Long-Run Granger Non-Causality in Cointegrated Systems (2006). (42) RePEc:bla:jtsera:v:31:y:2010:i:5:p:305-328 A sequential procedure to determine the number of breaks in trend with an integrated or stationary noise component (2010). (43) RePEc:bla:jtsera:v:28:y:2007:i:6:p:910-922 Using the HEGY Procedure When Not All Roots Are Present (2007). (44) RePEc:bla:jtsera:v:30:y:2009:i:1:p:47-69 Transformations and seasonal adjustment (2009). (45) RePEc:bla:jtsera:v:29:y:2008:i:2:p:300-330 Time-Transformed Unit Root Tests for Models with Non-Stationary Volatility (2008). (46) RePEc:bla:jtsera:v:30:y:2009:i:3:p:263-285 Testing for a break in persistence under long-range dependencies (2009). (47) RePEc:bla:jtsera:v:25:y:2004:i:6:p:895-922 Semiparametric Bayesian Inference of Long-Memory Stochastic Volatility Models (2004). (48) RePEc:bla:jtsera:v:24:y:2003:i:3:p:311-335 Testing Serial Correlation in Semiparametric Time Series Models (2003). (49) RePEc:bla:jtsera:v:29:y:2008:i:1:p:74-124 Duration time-series models with proportional hazard (2008). (50) RePEc:bla:jtsera:v:26:y:2005:i:1:p:83-105 Testing Non-Correlation and Non-Causality between Multivariate ARMA Time Series (2005). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:aah:create:2009-24 A Meta-Distribution for Non-Stationary Samples (2009). CREATES Research Papers (2) RePEc:eui:euiwps:eco2009/17 Forecasting Aggregated Time Series Variables: A Survey (2009). (3) RePEc:ime:imedps:09-e-23 Inconsistency of a Unit Root Test against Stochastic Unit Root Processes (2009). IMES Discussion Paper Series (4) RePEc:nlv:wpaper:1001 Forecasting the US Real House Price Index: Structural and Non-Structural Models with and without Fundamentals (2009). Working Papers (5) RePEc:uct:uconnp:2009-42 Forecasting the US Real House Price Index: Structural and Non-Structural Models with and without Fundamentals (2009). Working papers (6) RePEc:udt:wpecon:2009-03 Multivariate Contemporaneous Threshold Autoregressive Models (2009). Department of Economics Working Papers Recent citations received in: 2008 (1) RePEc:aah:create:2008-30 Parameter estimation in nonlinear AR-GARCH models (2008). CREATES Research Papers (2) RePEc:nuf:econwp:0806 Unit Root Testing with Unstable Volatility (2008). Economics Papers (3) RePEc:oxf:wpaper:396 Parameter estimation in nonlinear AR-GARCH models (2008). Economics Series Working Papers (4) RePEc:shr:wpaper:08-17 Modified Fast Double Sieve Bootstraps for ADF Tests (2008). Cahiers de recherche Recent citations received in: 2007 (1) RePEc:aah:create:2007-44 Long memory modelling of inflation with stochastic variance and structural breaks (2007). CREATES Research Papers (2) RePEc:dgr:kubcen:200723 Efficient Estimation of Autoregression Parameters and Innovation Distributions for Semiparametric Integer-Valued AR(p) Models (Subsequently replaced by DP 2008-53) (2007). Discussion Paper (3) RePEc:han:dpaper:dp-381 Testing for a break in persistence under long-range dependencies (2007). Diskussionspapiere der Wirtschaftswissenschaftlichen Fakultät der Universität Hannover Recent citations received in: 2006 (1) RePEc:bdm:wpaper:2006-12 Spurious Cointegration: The Engle-Granger Test in the Presence of Structural Breaks (2006). Working Papers (2) RePEc:cca:wpaper:32 International Macroeconomic Dynamics: A Factor Vector Autoregressive Approach (2006). Carlo Alberto Notebooks (3) RePEc:cwl:cwldpp:1585 Adaptive Estimation of Autoregressive Models with Time-Varying Variances (2006). Cowles Foundation Discussion Papers (4) RePEc:cwl:cwldpp:1585r Adaptive Estimation of Autoregressive Models with Time-Varying Variances (2006). Cowles Foundation Discussion Papers (5) RePEc:dgr:uvatin:20060101 Periodic Unobserved Cycles in Seasonal Time Series with an Application to US Unemployment (2006). Tinbergen Institute Discussion Papers (6) RePEc:hst:hstdps:d06-197 Asymptotic Properties of the Efficient Estimators for Cointegrating Regression Models with Serially Dependent Errors (2006). Hi-Stat Discussion Paper Series (7) RePEc:icr:wpicer:41-2006 International Macroeconomic Dynamics: a Factor Vector Autoregressive Approach (2006). ICER Working Papers (8) RePEc:udt:wpecon:2006-04 Contemporaneous Threshold Autoregressive Models: Estimation, Testing and Forecasting (2006). Department of Economics Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||