|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

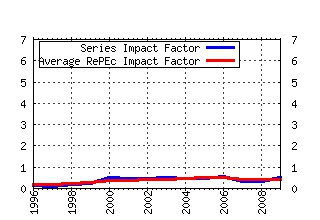

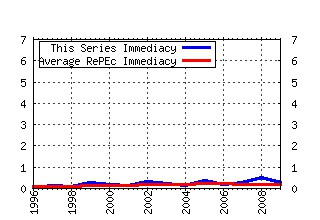

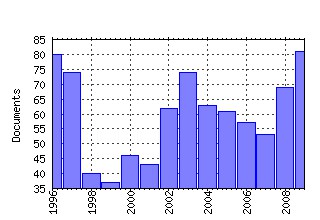

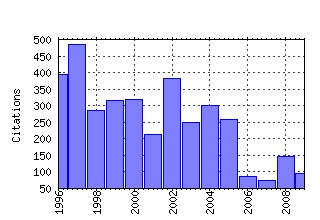

Econometric Theory Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:cup:etheor:v:11:y:1995:i:01:p:122-150_00 Multivariate Simultaneous Generalized ARCH (1995). (2) RePEc:cup:etheor:v:4:y:1988:i:01:p:60-69_01 Comment (1988). (3) RePEc:cup:etheor:v:12:y:1996:i:04:p:657-681_00 Which Moments to Match? (1996). (4) RePEc:cup:etheor:v:6:y:1990:i:02:p:291-292_00 Comment (1990). (5) RePEc:cup:etheor:v:13:y:1997:i:05:p:747-754_00 Econometric Analysis of Panel Data Badi H. Baltagi Wiley, 1995 (1997). (6) RePEc:cup:etheor:v:20:y:2004:i:03:p:597-625_20 PANEL COINTEGRATION: ASYMPTOTIC AND FINITE SAMPLE PROPERTIES OF POOLED TIME SERIES TESTS WITH AN APPLICATION TO THE PPP HYPOTHESIS (2004). (7) RePEc:cup:etheor:v:12:y:1996:i:4:p:657-81 (). (8) RePEc:cup:etheor:v:11:y:1995:i:1:p:122-50 (). (9) RePEc:cup:etheor:v:19:y:2003:i:02:p:280-310_19 ASYMPTOTIC THEORY FOR A VECTOR ARMA-GARCH MODEL (2003). (10) RePEc:cup:etheor:v:13:y:1997:i:03:p:315-352_00 Estimating Multiple Breaks One at a Time (1997). (11) RePEc:cup:etheor:v:12:y:1996:i:03:p:409-431_00 Markov Chain Monte Carlo Simulation Methods in Econometrics (1996). (12) RePEc:cup:etheor:v:7:y:1991:i:01:p:1-21_00 Asymptotically Efficient Estimation of Cointegration Regressions (1991). (13) RePEc:cup:etheor:v:21:y:2005:i:01:p:232-261_05 AUTOMATED INFERENCE AND LEARNING IN MODELING FINANCIAL VOLATILITY (2005). (14) RePEc:cup:etheor:v:10:y:1994:i:01:p:91-115_00 A Residual-Based Test of the Null of Cointegration Against the Alternative of No Cointegration (1994). (15) RePEc:cup:etheor:v:17:y:2001:i:06:p:1113-1141_17 THE GENERALIZED DYNAMIC FACTOR MODEL: REPRESENTATION THEORY (2001). (16) RePEc:cup:etheor:v:4:y:1988:i:01:p:70-76_01 Reply (1988). (17) RePEc:cup:etheor:v:13:y:1997:i:06:p:808-817_00 Optimal Prediction Under Asymmetric Loss (1997). (18) RePEc:cup:etheor:v:18:y:2002:i:01:p:17-39_18 MIXING AND MOMENT PROPERTIES OF VARIOUS GARCH AND STOCHASTIC VOLATILITY MODELS (2002). (19) RePEc:cup:etheor:v:11:y:1995:i:05:p:1131-1147_00 Inference in Models with Nearly Integrated Regressors (1995). (20) RePEc:cup:etheor:v:2:y:1986:i:01:p:107-131_01 Asymptotic Theory for ARCH Models: Estimation and Testing (1986). (21) RePEc:cup:etheor:v:14:y:1998:i:01:p:70-86_14 STRONG CONSISTENCY OF ESTIMATORS FOR MULTIVARIATE ARCH MODELS (1998). (22) RePEc:cup:etheor:v:10:y:1994:i:01:p:29-52_00 Asymptotic Theory for the Garch(1,1) Quasi-Maximum Likelihood Estimator (1994). (23) RePEc:cup:etheor:v:15:y:1999:i:06:p:814-823_15 UNEQUALLY SPACED PANEL DATA REGRESSIONS WITH AR(1) DISTURBANCES (1999). (24) RePEc:cup:etheor:v:12:y:1996:i:3:p:409-31 (). (25) RePEc:cup:etheor:v:15:y:1999:i:03:p:269-298_15 ASYMPTOTICS FOR NONLINEAR TRANSFORMATIONS OF INTEGRATED TIME SERIES (1999). (26) RePEc:cup:etheor:v:18:y:2002:i:03:p:722-729_18 NECESSARY AND SUFFICIENT MOMENT CONDITIONS FOR THE GARCH(r,s) AND ASYMMETRIC POWER GARCH(r,s) MODELS (2002). (27) RePEc:cup:etheor:v:14:y:1998:i:06:p:783-793_14 A NOTE ON THE CONVERGENCE OF NONPARAMETRIC DEA ESTIMATORS FOR PRODUCTION EFFICIENCY SCORES (1998). (28) RePEc:cup:etheor:v:9:y:1993:i:02:p:222-240_00 Testing Identifiability and Specification in Instrumental Variable Models (1993). (29) RePEc:cup:etheor:v:13:y:1997:i:3:p:315-52 (). (30) RePEc:cup:etheor:v:11:y:1995:i:03:p:530-536_00 Causality in the Long Run (1995). (31) RePEc:cup:etheor:v:15:y:1999:i:04:p:549-582_15 THE NONSTATIONARY FRACTIONAL UNIT ROOT (1999). (32) RePEc:cup:etheor:v:8:y:1992:i:04:p:489-500_01 Convergence to Stochastic Integrals for Dependent Heterogeneous Processes (1992). (33) RePEc:cup:etheor:v:5:y:1989:i:02:p:181-240_01 Partially Identified Econometric Models (1989). (34) RePEc:cup:etheor:v:11:y:1995:i:05:p:1148-1171_00 Rethinking the Univariate Approach to Unit Root Testing: Using Covariates to Increase Power (1995). (35) RePEc:cup:etheor:v:5:y:1989:i:01:p:95-131_01 Statistical Inference in Regressions with Integrated Processes: Part 2 (1989). (36) RePEc:cup:etheor:v:4:y:1988:i:03:p:468-497_01 Statistical Inference in Regressions with Integrated Processes: Part 1 (1988). (37) RePEc:cup:etheor:v:13:y:1997:i:06:p:818-848_00 Wald-Type Tests for Detecting Breaks in the Trend Function of a Dynamic Time Series (1997). (38) RePEc:cup:etheor:v:11:y:1995:i:03:p:560-586_00 Nonparametric Kernel Estimation for Semiparametric Models (1995). (39) RePEc:cup:etheor:v:5:y:1989:i:02:p:256-271_01 Testing for Unit Roots in Time Series Data (1989). (40) RePEc:cup:etheor:v:13:y:1997:i:6:p:808-17 (). (41) RePEc:cup:etheor:v:18:y:2002:i:02:p:313-348_18 TESTING FOR A UNIT ROOT IN A TIME SERIES WITH A LEVEL SHIFT AT UNKNOWN TIME (2002). (42) RePEc:cup:etheor:v:15:y:1999:i:03:p:361-376_15 THE SIZE DISTORTION OF BOOTSTRAP TESTS (1999). (43) RePEc:cup:etheor:v:17:y:2001:i:04:p:686-710_17 ON THE LOG PERIODOGRAM REGRESSION ESTIMATOR OF THE MEMORY PARAMETER IN LONG MEMORY STOCHASTIC VOLATILITY MODELS (2001). (44) RePEc:cup:etheor:v:11:y:1995:i:02:p:359-368_00 An LM Test for a Unit Root in the Presence of a Structural Change (1995). (45) RePEc:cup:etheor:v:10:y:1994:i:1:p:95-115 (). (46) RePEc:cup:etheor:v:17:y:2001:i:02:p:451-470_17 ASYMPTOTIC PROPERTIES OF WEIGHTED M-ESTIMATORS FOR STANDARD STRATIFIED SAMPLES (2001). (47) RePEc:cup:etheor:v:20:y:2004:i:05:p:813-843_20 INSTRUMENTAL VARIABLE ESTIMATION OF A THRESHOLD MODEL (2004). (48) RePEc:cup:etheor:v:11:y:1995:i:5:p:1131-47 (). (49) RePEc:cup:etheor:v:7:y:1991:i:1:p:1-21 (). (50) RePEc:cup:etheor:v:14:y:1998:i:03:p:295-325_14 CONSISTENT SPECIFICATION TESTING WITH NUISANCE PARAMETERS PRESENT ONLY UNDER THE ALTERNATIVE (1998). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:aah:create:2009-22 Co-integration Rank Testing under Conditional Heteroskedasticity (2009). CREATES Research Papers (2) RePEc:aah:create:2009-37 Nearly Efficient Likelihood Ratio Tests of the Unit Root Hypothesis (2009). CREATES Research Papers (3) RePEc:aah:create:2009-44 Semiparametric Modelling and Estimation: A Selective Overview (2009). CREATES Research Papers (4) RePEc:adl:wpaper:2009-26 Uniform Consistency for Nonparametric Estimators in Null Recurrent Time Series (2009). School of Economics Working Papers (5) RePEc:bos:wpaper:wp2009-005 A Sequential Procedure to Determine the Number of Breaks in Trend with an Integrated or Stationary Noise Component (2009). Boston University - Department of Economics - Working Papers Series (6) RePEc:cwl:cwldpp:1700 Dynamic Misspecification in Nonparametric Cointegrating Regression (2009). Cowles Foundation Discussion Papers (7) RePEc:cwl:cwldpp:1702 Nonparametric Structural Estimation via Continuous Location Shifts in an Endogenous Regressor (2009). Cowles Foundation Discussion Papers (8) RePEc:dgr:umamet:2009056 Detrending Bootstrap Unit Root Tests (2009). Research Memoranda (9) RePEc:eca:wpaper:2009_023 A Robust Criterion for Determining the Number of Factors in Approximate Factor Models (2009). Working Papers ECARES (10) RePEc:imf:imfwpa:09/231 Three Cycles: Housing, Credit, and Real Activity (2009). IMF Working Papers (11) RePEc:not:notgts:09/01 Robust methods for detecting multiple level breaks in autocorrelated time series [Revised to become No. 10/01 above] (2009). Discussion Papers (12) RePEc:not:notgts:09/03 The impact of the initial condition on robust tests for a linear trend (2009). Discussion Papers (13) RePEc:not:notgts:09/05 Testing for unit roots in the presence of a possible break in trend and non-stationary volatility (2009). Discussion Papers (14) RePEc:nzb:nzbdps:2009/12 A quarterly post-World War II real GDP series for New Zealand (2009). Reserve Bank of New Zealand Discussion Paper Series (15) RePEc:pra:mprapa:18850 Estimating Semiparametric Panel Data Models by Marginal Integration (2009). MPRA Paper (16) RePEc:pra:mprapa:31315 Regressions with Asymptotically Collinear Regressor (2009). MPRA Paper (17) RePEc:pra:mprapa:32102 Exploring the effect of countriesâ economic prosperity on their biodiversity performance (2009). MPRA Paper (18) RePEc:ptu:wpaper:w200902 Finite Sample Performance of Frequency and Time Domain Tests for Seasonal Fractional Integration (2009). Working Papers (19) RePEc:stn:sotoec:0918 Generating functions and short recursions, with applications to the moments of quadratic forms in noncentral normal vectors (2009). Discussion Paper Series In Economics And Econometrics (20) RePEc:tse:wpaper:22272 Set Identified Linear Models (2009). TSE Working Papers (21) RePEc:udt:wpecon:2009-06 Contemporaneous-Threshold Smooth Transition GARCH Models (2009). Department of Economics Working Papers (22) RePEc:zbw:ifweej:200932 Avoiding extinction: equal treatment of the present and the future (2009). Economics - The Open-Access, Open-Assessment E-Journal Recent citations received in: 2008 (1) RePEc:aah:create:2008-37 Uniform Convergence Rates of Kernel Estimators with Heterogenous, Dependent Data (2008). CREATES Research Papers (2) RePEc:aah:create:2008-50 Testing for Co-integration in Vector Autoregressions with Non-Stationary Volatility (2008). CREATES Research Papers (3) RePEc:aah:create:2008-52 Likelihood based testing for no fractional cointegration (2008). CREATES Research Papers (4) RePEc:aah:create:2008-53 Maximum likelihood estimation of fractionally cointegrated systems (2008). CREATES Research Papers (5) RePEc:aah:create:2008-62 Testing for Unit Roots in the Presence of a Possible Break in Trend and Non-Stationary Volatility (2008). CREATES Research Papers (6) RePEc:bos:wpaper:wp2008-010 Testing for Breaks in Coefficients and Error Variance: Simulations and Applications (2008). Boston University - Department of Economics - Working Papers Series (7) RePEc:bos:wpaper:wp2008-011 Testing Jointly for Structural Changes in the Error Variance and Coefficients of a Linear Regression Model (2008). Boston University - Department of Economics - Working Papers Series (8) RePEc:crd:wpaper:08003 GMM Redundancy Results for General Missing Data Problems (2008). Working Papers (9) RePEc:dgr:eureir:1765013780 Shock and volatility spillovers among equity sectors of the Gulf Arab stock markets (2008). Econometric Institute Report (10) RePEc:dgr:eureir:1765013910 The ten commandments for optimizing value-at-risk and daily capital charges (2008). Econometric Institute Report (11) RePEc:dgr:umamet:2008048 Cross-Sectional Dependence Robust Block Bootstrap Panel Unit Root Tests (2008). Research Memoranda (12) RePEc:eab:financ:22571 Volatility Dynamics in Foreign Exchange Rates : Further Evidence from the Malaysian Ringgit and Singapore Dollar (2008). Finance Working Papers (13) RePEc:eui:euiwps:eco2008/24 Testing for the Cointegrating Rank of a Vector Autoregressive Process with Uncertain Deterministic Trend Term (2008). (14) RePEc:hit:ccesdp:6 Model Selection Criteria for the Leads-and-Lags Cointegrating Regression (2008). CCES Discussion Paper Series (15) RePEc:hst:ghsdps:gd08-006 Model Selection Criteria for the Leads-and-Lags Cointegrating Regression (2008). Global COE Hi-Stat Discussion Paper Series (16) RePEc:ise:isegwp:wp182008 Persistence in Airline Accidents (2008). Working Papers (17) RePEc:ivi:wpasad:2008-11 Specification Tests for the Distribution of Errors in Nonoarametric Regression: A Martingale Approach (2008). Working Papers. Serie AD (18) RePEc:kof:wpskof:08-189 Negative Volatility Spillovers in the Unrestricted ECCC-GARCH Model (2008). KOF Working papers (19) RePEc:nbr:nberwo:14447 Inferring Welfare Maximizing Treatment Assignment under Budget Constraints (2008). NBER Working Papers (20) RePEc:nbs:wpaper:2008/12 Is real GDP per capita a stationary process? Smooth transitions, nonlinear trends and unit root testing (2008). Working Papers (21) RePEc:ner:maastr:urn:nbn:nl:ui:27-22287 Panel unit root tests in the presence of cross-sectional dependencies: comparison and implications for modelling. (2008). Open Access publications from Maastricht University (22) RePEc:nuf:econwp:0806 Unit Root Testing with Unstable Volatility (2008). Economics Papers (23) RePEc:oxf:wpaper:396 Parameter estimation in nonlinear AR-GARCH models (2008). Economics Series Working Papers (24) RePEc:pad:wpaper:0064 Thresholds, News Impact Surfaces and Dynamic Asymmetric Multivariate GARCH (2008). Marco Fanno Working Papers (25) RePEc:pra:mprapa:11988 Nonstationary-Volatility Robust Panel Unit Root Tests and the Great Moderation (2008). MPRA Paper (26) RePEc:pra:mprapa:12008 Now, whose schools are really better (or weaker) than Germanys? A multiple testing approach (2008). MPRA Paper (27) RePEc:pra:mprapa:6913 On the distribution of the adaptive LASSO estimator (2008). MPRA Paper (28) RePEc:sca:scaewp:0805 Volatility Dynamics in Foreign Exchange Rates: Further Evidence from the Malaysian Ringgit and Singapore Dollar (2008). SCAPE Policy Research Working Paper Series (29) RePEc:sip:dpaper:07-053 Testing for Common Values in Canadian Treasury Bill Auctions (2008). Discussion Papers (30) RePEc:spr:alstar:v:92:y:2008:i:1:p:91-99 Bias correction for the regression-based LM fractional integration test (2008). AStA Advances in Statistical Analysis (31) RePEc:spr:testjl:v:17:y:2008:i:3:p:461-471 Rejoinder on: Control of the false discovery rate under dependence using the bootstrap and subsampling (2008). TEST: An Official Journal of the Spanish Society of Statistics and Operations Research (32) RePEc:ssb:dispap:539 Non-parametric Identification of the Mixed Hazards Model with Interval-Censored Durations (2008). Discussion Papers (33) RePEc:uct:uconnp:2008-49 Dynamic Stock Market Interactions between the Canadian, Mexican, and the United States Markets: The NAFTA Experience (2008). Working papers (34) RePEc:wrk:warwec:876 Testing for Smooth Transition Nonlinearity in Adjustments of Cointegrating Systems (2008). The Warwick Economics Research Paper Series (TWERPS) (35) RePEc:zbw:sfb475:200811 An intersection test for panel unit roots (2008). Technical Reports (36) RePEc:zur:iewwpx:320 Robust Performance Hypothesis Testing with the Sharpe Ratio (2008). IEW - Working Papers (37) RePEc:zur:iewwpx:337 Control of the False Discovery Rate under Dependence using the Bootstrap and Subsampling (2008). IEW - Working Papers Recent citations received in: 2007 (1) RePEc:aah:aarhec:2007-16 A Statistical Programme Assignment Model (2007). Economics Working Papers (2) RePEc:cmf:wpaper:wp2007_0713 ON THE EFFICIENCY AND CONSISTENCY OF LIKELIHOOD ESTIMATION IN MULTIVARIATE CONDITIONALLY HETEROSKEDASTIC DYNAMIC REGRESSION MODELS (2007). Working Papers (3) RePEc:ctl:louvec:2007033 Theory and inference for a Markov switching GARCH model (2007). Discussion Papers (ECON - Département des Sciences Economiques) (4) RePEc:cwl:cwldpp:1595 Transition Modeling and Econometric Convergence Tests (2007). Cowles Foundation Discussion Papers (5) RePEc:hhs:osloec:2007_010 Long-term Outcomes of Vocational Rehabilitation Programs: Labor Market Transitions and Job Durations for Immigrants (2007). Memorandum (6) RePEc:hhs:osloec:2007_013 Unemployment Insurance in Welfare States: Soft Constraints and Mild Sanctions (2007). Memorandum (7) RePEc:iea:carech:0709 Theory and inference for a Markov switching Garch model. (2007). Cahiers de recherche (8) RePEc:inu:caeprp:2007019 Detecting Misspecifications in Autoregressive Conditional Duration Models (2007). Caepr Working Papers (9) RePEc:iza:izadps:dp2877 Unemployment Insurance in Welfare States: Soft Constraints and Mild Sanctions (2007). IZA Discussion Papers (10) RePEc:iza:izadps:dp3165 A Statistical Programme Assignment Model (2007). IZA Discussion Papers (11) RePEc:lvl:lacicr:0733 Theory and Inference for a Markov-Switching GARCH Model (2007). Cahiers de recherche (12) RePEc:not:notgts:06/03 Testing for a unit root when uncertain about the trend [Revised to become 07/03 above] (2007). Discussion Papers (13) RePEc:not:notgts:07/03 Unit root testing in practice: dealing with uncertainty over the trend and initial condition (2007). Discussion Papers (14) RePEc:pra:mprapa:11980 Specification testing in discretized diffusion models: Theory and practice (2007). MPRA Paper (15) RePEc:pra:mprapa:2744 A Gravity approach to evaluate the significance of trade liberalization in vertically-related goods in the presence of non-tariff barriers (2007). MPRA Paper Recent citations received in: 2006 (1) RePEc:cor:louvco:2006042 Deciding between GARCH and stochastic volatility via strong decision rules (2006). CORE Discussion Papers (2) RePEc:cor:louvco:2006068 A GARCH (1,1) estimator with (almost) no moment conditions on the error term (2006). CORE Discussion Papers (3) RePEc:cor:louvco:2006071 Asymptotic theory for a factor GARCH model (2006). CORE Discussion Papers (4) RePEc:cwl:cwldpp:1594 Asymptotic Theory for Local Time Density Estimation and Nonparametric Cointegrating Regression (2006). Cowles Foundation Discussion Papers (5) RePEc:dgr:uvatin:20060078 The Asymptotic and Finite Sample Distributions of OLS and Simple IV in Simultaneous Equations (2006). Tinbergen Institute Discussion Papers (6) RePEc:eui:euiwps:eco2006/29 Testing for the Cointegrating Rank of a VAR Process with Level Shift and Trend Break (2006). (7) RePEc:eui:euiwps:eco2006/34 How the Removal of Deposit Rate Ceilings Has Changed Monetary Transmission in the US: Theory and Evidence (2006). (8) RePEc:hum:wpaper:sfb649dp2006-012 Bootstrapping Systems Cointegration Tests with a Prior Adjustment for Deterministic Terms (2006). SFB 649 Discussion Papers (9) RePEc:hum:wpaper:sfb649dp2006-067 Testing for the Cointegrating Rank of a VAR Process with Level Shift and Trend Break (2006). SFB 649 Discussion Papers (10) RePEc:msh:ebswps:2006-20 Tests for Over-identifying Restrictions in Partially Identified Linear Structural Equations (2006). Monash Econometrics and Business Statistics Working Papers (11) RePEc:qed:wpaper:1029 Determining the Cointegrating Rank in Nonstationary Fractional Systems by the Exact Local Whittle Approach (2006). Working Papers (12) RePEc:qed:wpaper:1101 Simple (but effective) tests of long memory versus structural breaks (2006). Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||