|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

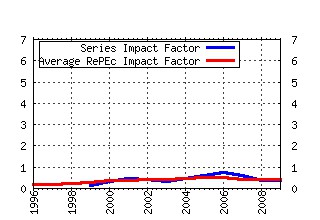

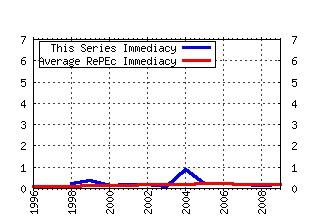

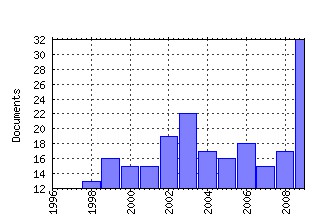

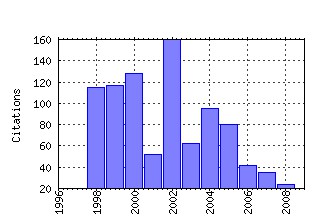

Journal of Financial Markets Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:finmar:v:5:y:2002:i:1:p:31-56 Illiquidity and stock returns: cross-section and time-series effects (2002). (2) RePEc:eee:finmar:v:3:y:2000:i:3:p:205-258 Market microstructure: A survey (2000). (3) RePEc:eee:finmar:v:2:y:1999:i:2:p:99-134 Order flow composition and trading costs in a dynamic limit order market1 (1999). (4) RePEc:eee:finmar:v:1:y:1998:i:3-4:p:353-383 Aggressiveness and survival of overconfident traders (1998). (5) RePEc:eee:finmar:v:7:y:2004:i:1:p:53-74 Order aggressiveness in limit order book markets (2004). (6) RePEc:eee:finmar:v:1:y:1998:i:2:p:203-219 Liquidity and stock returns: An alternative test (1998). (7) RePEc:eee:finmar:v:1:y:1998:i:1:p:1-50 Optimal control of execution costs (1998). (8) RePEc:eee:finmar:v:8:y:2005:i:2:p:217-264 Market microstructure: A survey of microfoundations, empirical results, and policy implications (2005). (9) RePEc:eee:finmar:v:7:y:2004:i:1:p:1-25 Impacts of trades in an error-correction model of quote prices (2004). (10) RePEc:eee:finmar:v:4:y:2001:i:1:p:73-84 On the survival of overconfident traders in a competitive securities market (2001). (11) RePEc:eee:finmar:v:5:y:2002:i:3:p:309-321 Price discovery and common factor models (2002). (12) RePEc:eee:finmar:v:3:y:2000:i:2:p:83-111 Inferring investor behavior: Evidence from TORQ data (2000). (13) RePEc:eee:finmar:v:8:y:2005:i:3:p:265-287 Should securities markets be transparent? (2005). (14) RePEc:eee:finmar:v:5:y:2002:i:3:p:259-276 Some desiderata for the measurement of price discovery across markets (2002). (15) RePEc:eee:finmar:v:2:y:1999:i:3:p:227-271 Reputation and performance fee effects on portfolio choice by investment advisers1 (1999). (16) RePEc:eee:finmar:v:2:y:1999:i:3:p:193-226 Intra-day market activity (1999). (17) RePEc:eee:finmar:v:7:y:2004:i:3:p:271-299 Market liquidity as a sentiment indicator (2004). (18) RePEc:eee:finmar:v:5:y:2002:i:3:p:277-308 Security price adjustment across exchanges: an investigation of common factor components for Dow stocks (2002). (19) RePEc:eee:finmar:v:10:y:2007:i:1:p:1-25 Measuring the resiliency of an electronic limit order book (2007). (20) RePEc:eee:finmar:v:6:y:2003:i:4:p:461-489 Quote setting and price formation in an order driven market (2003). (21) RePEc:eee:finmar:v:3:y:2000:i:3:p:259-286 On the occurrence and consequences of inaccurate trade classification (2000). (22) RePEc:eee:finmar:v:3:y:2000:i:4:p:333-363 Market structure, informational efficiency and liquidity: An experimental comparison of auction and dealer markets (2000). (23) RePEc:eee:finmar:v:6:y:2003:i:3:p:233-257 Issues in assessing trade execution costs (2003). (24) RePEc:eee:finmar:v:2:y:1999:i:4:p:329-357 The organization of financial exchange markets: Theory and evidence (1999). (25) RePEc:eee:finmar:v:2:y:1999:i:1:p:29-48 Market depth and order size1 (1999). (26) RePEc:eee:finmar:v:5:y:2002:i:2:p:127-167 Market architecture: limit-order books versus dealership markets (2002). (27) RePEc:eee:finmar:v:1:y:1998:i:1:p:51-87 Decimalization and competition among stock markets: Evidence from the Toronto Stock Exchange cross-listed securities (1998). (28) RePEc:eee:finmar:v:8:y:2005:i:4:p:377-399 Duration, volume and volatility impact of trades (2005). (29) RePEc:eee:finmar:v:6:y:2003:i:3:p:363-387 Intra-industry momentum: the case of REITs (2003). (30) RePEc:eee:finmar:v:1:y:1998:i:2:p:175-201 Financial analysts and information-based trade (1998). (31) RePEc:eee:finmar:v:8:y:2005:i:1:p:89-109 International momentum strategies: a stochastic dominance approach (2005). (32) RePEc:eee:finmar:v:5:y:2002:i:3:p:329-339 Stalking the efficient price in market microstructure specifications: an overview (2002). (33) RePEc:eee:finmar:v:11:y:2008:i:3:p:228-258 Melting pot or salad bowl: Some evidence from U.S. investments abroad (2008). (34) RePEc:eee:finmar:v:7:y:2004:i:2:p:145-185 Expandable limit order markets (2004). (35) RePEc:eee:finmar:v:6:y:2003:i:4:p:517-538 Traders choice between limit and market orders: evidence from NYSE stocks (2003). (36) RePEc:eee:finmar:v:4:y:2001:i:4:p:385-412 Knowing me, knowing you: : Trader anonymity and informed trading in parallel markets (2001). (37) RePEc:eee:finmar:v:9:y:2006:i:4:p:408-432 Order book characteristics and the volume-volatility relation: Empirical evidence from a limit order market (2006). (38) RePEc:eee:finmar:v:2:y:1999:i:1:p:49-68 The alpha factor asset pricing model: A parable (1999). (39) RePEc:eee:finmar:v:5:y:2002:i:2:p:223-257 The impact of the Federal Reserve Banks open market operations (2002). (40) RePEc:eee:finmar:v:9:y:2006:i:2:p:162-179 On the importance of timing specifications in market microstructure research (2006). (41) RePEc:eee:finmar:v:12:y:2009:i:2:p:143-172 Technology and liquidity provision: The blurring of traditional definitions (2009). (42) RePEc:eee:finmar:v:3:y:2000:i:2:p:177-204 The determinants of trading volume of high-yield corporate bonds (2000). (43) RePEc:eee:finmar:v:5:y:2002:i:1:p:57-82 Intraday analysis of market integration: Dutch blue chips traded in Amsterdam and New York (2002). (44) RePEc:eee:finmar:v:10:y:2007:i:2:p:107-143 Informative trading or just costly noise? An analysis of Central Bank interventions (2007). (45) RePEc:eee:finmar:v:1:y:1998:i:3-4:p:321-352 Strategic trading, asymmetric information and heterogeneous prior beliefs (1998). (46) RePEc:eee:finmar:v:9:y:2006:i:4:p:333-365 Quantifying cognitive biases in analyst earnings forecasts (2006). (47) RePEc:eee:finmar:v:7:y:2004:i:3:p:301-333 Trading strategies during circuit breakers and extreme market movements (2004). (48) RePEc:eee:finmar:v:1:y:1998:i:3-4:p:385-402 Long-lived information and intraday patterns (1998). (49) RePEc:eee:finmar:v:6:y:2003:i:1:p:1-21 Excess demand and equilibration in multi-security financial markets: the empirical evidence (2003). (50) RePEc:eee:finmar:v:8:y:2005:i:3:p:288-308 Empirical evidence on the evolution of liquidity: Choice of market versus limit orders by informed and uninformed traders (2005). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:ces:ceswps:_2656 Exchange Rate Management in Emerging Markets: Intervention via an Electronic Limit Order Book (2009). CESifo Working Paper Series (2) RePEc:cfs:cfswop:wp200918 Modelling and Forecasting Liquidity Supply Using Semiparametric Factor Dynamics (2009). CFS Working Paper Series (3) RePEc:ebg:heccah:0920 Liquidity cycles and make/take fees in electronic markets (2009). Les Cahiers de Recherche (4) RePEc:ide:wpaper:20653 Liquidity Shocks and Order Book Dynamics (2009). IDEI Working Papers (5) RePEc:nbr:nberwo:15009 Liquidity Shocks and Order Book Dynamics (2009). NBER Working Papers (6) RePEc:tse:wpaper:21944 Liquidity Shocks and Order Book Dynamics (2009). TSE Working Papers Recent citations received in: 2008 (1) RePEc:nbr:nberwo:14158 Short Sales and Trade Classification Algorithms (2008). NBER Working Papers (2) RePEc:vic:vicddp:0802 Why Larger Lenders obtain Higher Returns: Evidence from Sovereign Syndicated Loans (2008). Department Discussion Papers Recent citations received in: 2007 (1) RePEc:nbr:nberwo:13625 When Does a Mutual Funds Trade Reveal its Skill? (2007). NBER Working Papers (2) RePEc:oxf:wpaper:340 Estimating Quadratic Variation When Quoted Prices Change by a Constant Increment (2007). Economics Series Working Papers (3) RePEc:pra:mprapa:5548 Liquidation in the Face of Adversity: Stealth Vs. Sunshine Trading, Predatory Trading Vs. Liquidity Provision (2007). MPRA Paper Recent citations received in: 2006 (1) RePEc:bde:wpaper:0630 Option-implied preferences adjustments, density forecasts, and the equity risk premium (2006). Banco de España Working Papers (2) RePEc:cor:louvco:2006110 Does the open limit order book matter in explaining long run volatility ? (2006). CORE Discussion Papers (3) RePEc:crt:wpaper:0615 The Components of the Bid-Ask Spread: The case of the Athens Stock Exchange (2006). Working Papers (4) RePEc:ebg:essewp:dr-06017 Preferencing, internalization and inventory position (2006). ESSEC Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||