|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

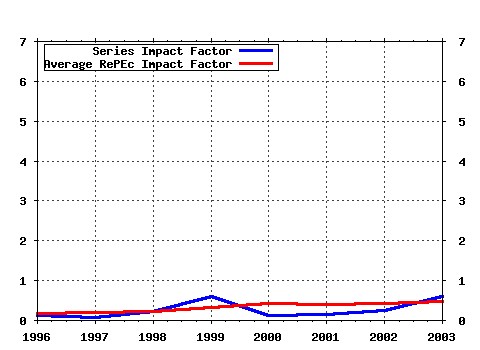

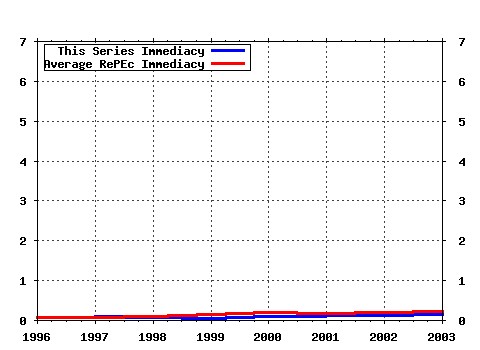

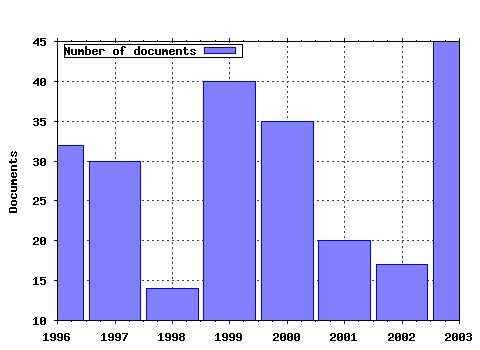

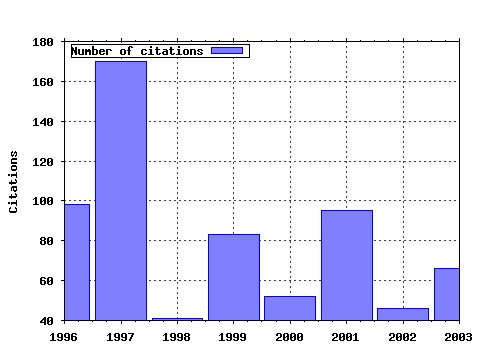

Journal of Accounting and Economics Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:jaecon:v:24:y:1997:i:2:p:127-127 . (1997). Journal of Accounting and Economics (2) RePEc:eee:jaecon:v:19:y:1995:i:2-3:p:179-208 Complementarities and fit strategy, structure, and organizational change in manufacturing (1995). Journal of Accounting and Economics (3) RePEc:eee:jaecon:v:7:y:1985:i:1-3:p:11-42 Corporate performance and managerial remuneration : An empirical analysis (1985). Journal of Accounting and Economics (4) RePEc:eee:jaecon:v:7:y:1985:i:1-3:p:85-107 The effect of bonus schemes on accounting decisions (1985). Journal of Accounting and Economics (5) RePEc:eee:jaecon:v:8:y:1986:i:1:p:3-35 Predicting takeover targets : A methodological and empirical analysis (1986). Journal of Accounting and Economics (6) RePEc:eee:jaecon:v:5:y:1983:i::p:179-194 Discretionary disclosure (1983). Journal of Accounting and Economics (7) RePEc:eee:jaecon:v:13:y:1990:i:4:p:305-340 Evidence that stock prices do not fully reflect the implications of current earnings for future earnings (1990). Journal of Accounting and Economics (8) RePEc:eee:jaecon:v:21:y:1996:i:1:p:5-43 Employee stock option exercises an empirical analysis (1996). Journal of Accounting and Economics (9) RePEc:eee:jaecon:v:3:y:1981:i:3:p:183-199 Auditor size and audit quality (1981). Journal of Accounting and Economics (10) RePEc:eee:jaecon:v:33:y:2002:i:1:p:3-42 Stock options for undiversified executives (2002). Journal of Accounting and Economics (11) RePEc:eee:jaecon:v:8:y:1986:i:2:p:159-172 Information quality and the valuation of new issues (1986). Journal of Accounting and Economics (12) RePEc:eee:jaecon:v:24:y:1997:i:1:p:3-37 The conservatism principle and the asymmetric timeliness of earnings (1997). Journal of Accounting and Economics (13) RePEc:eee:jaecon:v:19:y:1995:i:2-3:p:247-277 Incentive compensation in a corporate hierarchy (1995). Journal of Accounting and Economics (14) RePEc:eee:jaecon:v:18:y:1994:i:2:p:207-231 Employee stock options (1994). Journal of Accounting and Economics (15) RePEc:eee:jaecon:v:16:y:1993:i:1-3:p:55-100 Accounting earnings and top executive compensation (1993). Journal of Accounting and Economics (16) RePEc:eee:jaecon:v:29:y:2000:i:1:p:1-51 The effect of international institutional factors on properties of accounting earnings (2000). Journal of Accounting and Economics (17) RePEc:eee:jaecon:v:18:y:1994:i:1:p:3-42 Accounting earnings and cash flows as measures of firm performance : The role of accounting accruals (1994). Journal of Accounting and Economics (18) RePEc:eee:jaecon:v:28:y:1999:i:2:p:151-184 The use of equity grants to manage optimal equity incentive levels (1999). Journal of Accounting and Economics (19) RePEc:eee:jaecon:v:31:y:2001:i:1-3:p:105-231 Capital markets research in accounting (2001). Journal of Accounting and Economics (20) RePEc:eee:jaecon:v:15:y:1992:i:4:p:445-484 A theory of responsibility centers (1992). Journal of Accounting and Economics (21) RePEc:eee:jaecon:v:19:y:1995:i:2-3:p:443-470 Corporate research & development investments international comparisons (1995). Journal of Accounting and Economics (22) RePEc:eee:jaecon:v:24:y:1997:i:1:p:99-126 Earnings management to avoid earnings decreases and losses (1997). Journal of Accounting and Economics (23) RePEc:eee:jaecon:v:32:y:2001:i:1-3:p:237-333 Financial accounting information and corporate governance (2001). Journal of Accounting and Economics (24) RePEc:eee:jaecon:v:16:y:1993:i:1-3:p:273-315 Financial performance surrounding CEO turnover (1993). Journal of Accounting and Economics (25) RePEc:eee:jaecon:v:2:y:1980:i:1:p:3-28 The information content of security prices (1980). Journal of Accounting and Economics (26) RePEc:eee:jaecon:v:32:y:2001:i:1-3:p:3-87 Contracting theory and accounting (2001). Journal of Accounting and Economics (27) RePEc:eee:jaecon:v:12:y:1990:i:4:p:341-363 Voluntary disclosure with a strategic opponent (1990). Journal of Accounting and Economics (28) RePEc:eee:jaecon:v:31:y:2001:i:1-3:p:321-387 Empirical tax research in accounting (2001). Journal of Accounting and Economics (29) RePEc:eee:jaecon:v:20:y:1995:i:3:p:297-322 Auditor brand name reputations and industry specializations (1995). Journal of Accounting and Economics (30) RePEc:eee:jaecon:v:11:y:1989:i:2-3:p:255-274 Firm characteristics and analyst following (1989). Journal of Accounting and Economics (31) RePEc:eee:jaecon:v:7:y:1985:i:1-3:p:43-66 Executive compensation, management turnover, and firm performance : An empirical investigation (1985). Journal of Accounting and Economics (32) RePEc:eee:jaecon:v:20:y:1995:i:2:p:155-192 Price and return models (1995). Journal of Accounting and Economics (33) RePEc:eee:jaecon:v:25:y:1998:i:1:p:1-34 Relative valuation roles of equity book value and net income as a function of financial health (1998). Journal of Accounting and Economics (34) RePEc:eee:jaecon:v:5:y:1983:i::p:3-30 The association between performance plan adoption and corporate capital investment (1983). Journal of Accounting and Economics (35) RePEc:eee:jaecon:v:17:y:1994:i:1-2:p:145-176 Debt covenant violation and manipulation of accruals (1994). Journal of Accounting and Economics (36) RePEc:eee:jaecon:v:21:y:1996:i:2:p:161-193 CEO compensation: The role of individual performance evaluation (1996). Journal of Accounting and Economics (37) RePEc:eee:jaecon:v:24:y:1997:i:1:p:39-67 Changes in the value-relevance of earnings and book values over the past forty years (1997). Journal of Accounting and Economics (38) RePEc:eee:jaecon:v:34:y:2003:i:1-3:p:89-127 The structure and performance consequences of equity grants to employees of new economy firms (2003). Journal of Accounting and Economics (39) RePEc:eee:jaecon:v:36:y:2003:i:1-3:p:337-386 Limited attention, information disclosure, and financial reporting (2003). Journal of Accounting and Economics (40) RePEc:eee:jaecon:v:31:y:2001:i:1-3:p:255-307 Empirical research on accounting choice (2001). Journal of Accounting and Economics (41) RePEc:eee:jaecon:v:11:y:1989:i:2-3:p:143-181 An analysis of intertemporal and cross-sectional determinants of earnings response coefficients (1989). Journal of Accounting and Economics (42) RePEc:eee:jaecon:v:31:y:2001:i:1-3:p:3-75 The relevance of the value-relevance literature for financial accounting standard setting (2001). Journal of Accounting and Economics (43) RePEc:eee:jaecon:v:11:y:1989:i:4:p:295-329 Financial statement analysis and the prediction of stock returns (1989). Journal of Accounting and Economics (44) RePEc:eee:jaecon:v:32:y:2001:i:1-3:p:97-180 Essays on disclosure (2001). Journal of Accounting and Economics (45) RePEc:eee:jaecon:v:32:y:2001:i:1-3:p:349-410 Assessing empirical research in managerial accounting: a value-based management perspective (2001). Journal of Accounting and Economics (46) RePEc:eee:jaecon:v:10:y:1988:i:1:p:53-83 Analysts forecasts as earnings expectations (1988). Journal of Accounting and Economics (47) RePEc:eee:jaecon:v:15:y:1992:i:2-3:p:265-302 Earnings news and small traders : An intraday analysis (1992). Journal of Accounting and Economics (48) RePEc:eee:jaecon:v:22:y:1996:i:1-3:p:357-391 Market valuation of employee stock options (1996). Journal of Accounting and Economics (49) RePEc:eee:jaecon:v:26:y:1999:i:1-3:p:237-269 Disclosure requirements and stock exchange listing choice in an international context (1999). Journal of Accounting and Economics (50) RePEc:eee:jaecon:v:25:y:1998:i:1:p:101-127 Underwriting relationships, analysts earnings forecasts and investment recommendations (1998). Journal of Accounting and Economics Latest citations received in: | 2003 | 2002 | 2001 | 2000 Latest citations received in: 2003 (1) RePEc:bru:bruppp:03-18 The Impact of Risk on the Decision to Exercise an ESO (2003). Economics and Finance Section, School of Social Sciences, Brunel University / Public Policy Discussion Papers (2) RePEc:cpr:ceprdp:3843 Which Investors Fear Expropriation? Evidence from Investors Stock Picking (2003). C.E.P.R. Discussion Papers / CEPR Discussion Papers (3) RePEc:fra:franaf:123 The Cost of Employee Stock Options (2003). Goethe University Frankfurt am Main / Working Paper Series: Finance and Accounting (4) RePEc:htr:hcecon:301 Operational Efficiency and the Value-Relevance of Earnings (2003). Hunter College: Department of Economics / Hunter College Department of Economics Working Papers (5) RePEc:mit:sloanp:1839 Bridging the Reporting Gap: A Proposal for More Informative Reconciling of Book and Tax Income (2003). Massachusetts Institute of Technology (MIT), Sloan School of Management / Working papers (6) RePEc:nbr:nberwo:10013 Simple Forecasts and Paradigm Shifts (2003). National Bureau of Economic Research, Inc / NBER Working Papers (7) RePEc:uno:wpaper:2003-14 Heterogeneous beliefs and employee stock options (2003). University of New Orleans, Department of Economics and Finance / Working Papers Latest citations received in: 2002 (1) RePEc:nbr:nberwo:9059 Managing Option Fragility (2002). National Bureau of Economic Research, Inc / NBER Working Papers (2) RePEc:sbs:wpsefe:2002fe01 Stock Based Compensation: Firm-specific risk, Efficiency and Incentives (2002). Oxford Financial Research Centre / OFRC Working Papers Series Latest citations received in: 2001 Latest citations received in: 2000 (1) RePEc:fip:fedbcp:y:2000:i:jun:p:89-112:n:44 The role of financial reporting in reducing financial risks in the market (2000). Conference Series ; [Proceedings] (2) RePEc:uma:periwp:wp5 Is Africa a Net Creditor? New Estimates of Capital Flight from Severely Indebted Sub-Saharan African Countries (2000). Political Economy Research Institute, University of Massachusetts at Amherst / Working Papers (3) RePEc:ums:papers:2000-01 Is Africa a Net Creditor? New Estimates of Capital Flight from Severely Indebted Sub-Saharan African Countries, 1970-1996 (2000). University of Massachusetts Amherst, Department of Economics / Working Papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |