|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

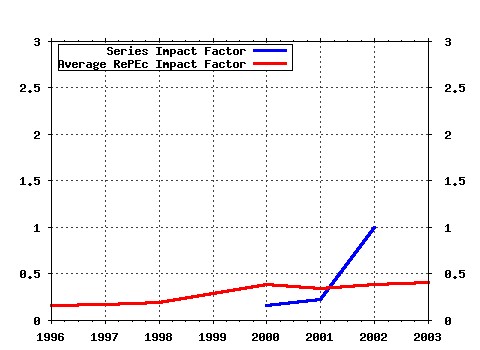

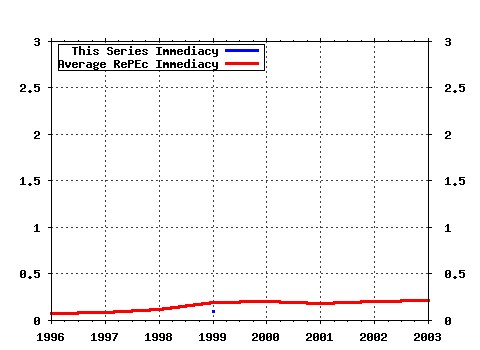

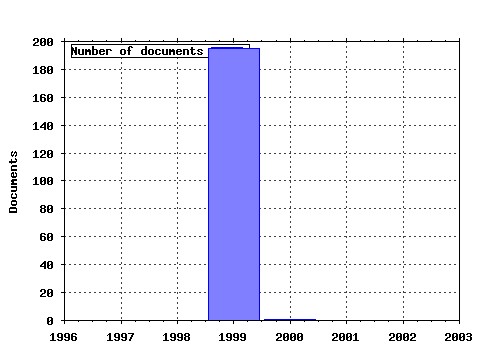

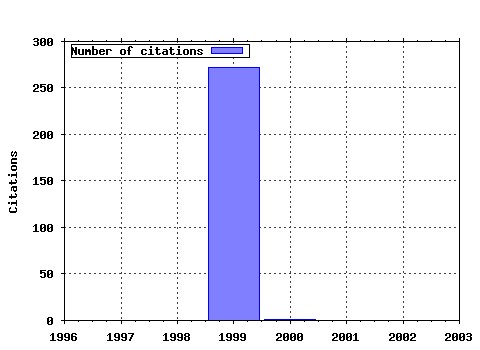

Society for Computational Economics / Computing in Economics and Finance 1999 Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:sce:scecf9:1022 Frictionless Commerce? A Comparison of Internet and Conventional Retailers (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (2) RePEc:sce:scecf9:1151 Optimal Monetary Policy with Staggered Wage and Price Contracts (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (3) RePEc:sce:scecf9:223 Heterogeneous Beliefs, Risk and Learning in a Simple Asset-Pricing Model (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (4) RePEc:sce:scecf9:401 Computational Experiments and Reality (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (5) RePEc:sce:scecf9:841 Simple Monetary Policy Rules Under Model Uncertainty (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (6) RePEc:sce:scecf9:1233 A Method for Taking Models to the Data (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (7) RePEc:sce:scecf9:1344 Stock Market Mean Reversion and the Optimal Equity Allocation of a Long-Lived Investor (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (8) RePEc:sce:scecf9:1113 Statistical Analysis of Cointegrated VAR Processes with Markovian Regime Shifts (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (9) RePEc:sce:scecf9:621 Are Deep Parameters Stable? The Lucas Critique as an Empirical Hypothesis (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (10) RePEc:sce:scecf9:1052 Optimal Horizons for Inflation Targeting (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (11) RePEc:sce:scecf9:112 Stochastic Volatility: Univariate and Multivariate Extensions (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (12) RePEc:sce:scecf9:1342 Evolution and Time Horizons in an Agent-Based Stock Market (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (13) RePEc:sce:scecf9:1241 Tests of Equal Forecast Accuracy and Encompassing for Nested Models (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (14) RePEc:sce:scecf9:1152 Real Implications of the Zero Bound on Nominal Interest Rates (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (15) RePEc:sce:scecf9:824 Simulation Based Finite- and Large-Sample Inference Methods in Simultaneous Equations (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (16) RePEc:sce:scecf9:1033 Using Symbolic Regression to Infer Strategies from Experimental Data (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (17) RePEc:sce:scecf9:832 Using Simulation Methods for Bayesian Econometric Models (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (18) RePEc:sce:scecf9:251 Inaccuracy of Loglinear Approximation in Welfare Calculations: the Case of International Risk Sharing (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (19) RePEc:sce:scecf9:511 Size Distortions of Tests of the Null Hypothesis of Stationarity: Evidence and Implications for Applied Work (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (20) RePEc:sce:scecf9:643 On the Identification of Cointegrated Systems in Small Samples: Practical Procedures with an Application to UK Wages and Prices (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (21) RePEc:sce:scecf9:722 Micro and Macro Hysteresis in Employment under Exchange Rate Uncertainty (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (22) RePEc:sce:scecf9:844 Permanent and Transitory Policy Shocks in a VAR with Asymmetric Information (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (23) RePEc:sce:scecf9:551 The Role of Automated Semiotic Classifications in Economic Domains (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (24) RePEc:sce:scecf9:154 Solving Large and Small Models on Microcomputers (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (25) RePEc:sce:scecf9:734 Asymmetric Shocks and Long-Run Economic Performances across Italian Regions (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (26) RePEc:sce:scecf9:111 Nonparametric Estimation of Multifactor Continuous Time Interest-Rate Models (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (27) RePEc:sce:scecf9:334 Perturbation Solution of Nonlinear Rational Expectations Models (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (28) RePEc:sce:scecf9:1243 An Approximate Wavelet MLE of Short- and Long-Memory Parameters (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (29) RePEc:sce:scecf9:721 Hysteresis and Unemployment: a Preliminary Investigation (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (30) RePEc:sce:scecf9:943 Long Memory Characteristics of the Distribution of Treasury Security Yields, Returns, and Volatility (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (31) RePEc:sce:scecf9:221 Learning with Bounded Memory in Stochastic Models (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (32) RePEc:sce:scecf9:353 Optimal Monetary Policy with Heterogeneous Agents: Is There a Case for Inflation? (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (33) RePEc:sce:scecf9:133 Valuation of Barrier Options in a Black-Scholes Setup with Jump Risk (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (34) RePEc:sce:scecf9:313 Forecasting Volatility under Multivariate Stochastic Volatility Model via Reprojection (1999). Society for Computational Economics / Computing in Economics and Finance 1999 (35) RePEc:sce:scecf9:944 A re-evaluation of empirical tests of the Fisher hypothesis (2000). Society for Computational Economics / Computing in Economics and Finance 1999 Latest citations received in: | 2003 | 2002 | 2001 | 2000 Latest citations received in: 2003 Latest citations received in: 2002 Latest citations received in: 2001 Latest citations received in: 2000 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |