|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

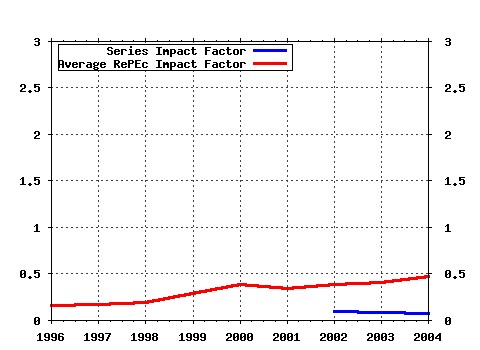

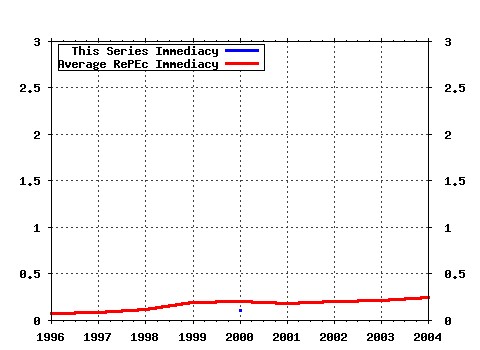

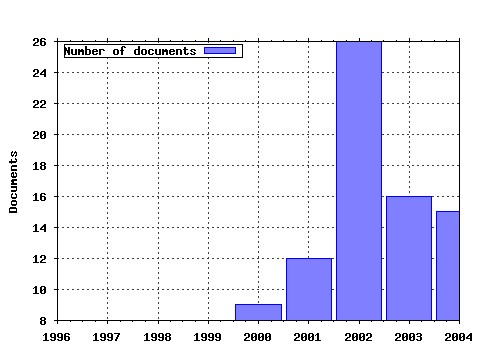

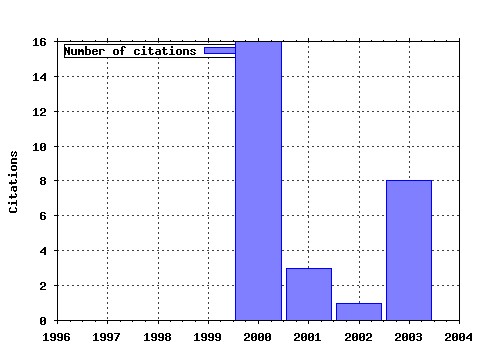

School of Business, Reading University / ICMA Centre Discussion Papers in Finance Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:rdg:icmadp:icma-dp2000-05 The ACD Model: Predictability of the Time Between Concecutive Trades (2000). (2) RePEc:rdg:icmadp:icma-dp2003-07 Multivariate GARCH Models: Software Choice and Estimation Issues (2003). (3) RePEc:rdg:icmadp:icma-dp2000-01 Value at Risk and Market Crashes (2000). (4) RePEc:rdg:icmadp:icma-dp2002-19 Smart Fund Managers? Stupid Money? (2003). (5) RePEc:rdg:icmadp:icma-dp2001-09 The Statistical Properties of Hedge Fund Index Returns (2001). (6) RePEc:rdg:icmadp:icma-dp2000-06 Orthogonal Methods for Generating Large Positive Semi-Definite Covariance Matrices (2000). (7) RePEc:rdg:icmadp:icma-dp2003-03 Statistical Properties of Forward Libor Rates (2003). (8) RePEc:rdg:icmadp:icma-dp2002-15 Generalization of the Sharpe Ratio and the Arbitrage-Free Pricing of Higher Moments (2002). (9) RePEc:rdg:icmadp:icma-dp2006-07 Speculative Bubbles in the S&P 500: Was the Tech Bubble Confined to the Tech Sector? (2006). (10) RePEc:rdg:icmadp:icma-dp2001-07 Credit Risk Diversification (2001). (11) RePEc:rdg:icmadp:icma-dp2005-05 The Spider in the Hedge (2005). (12) RePEc:rdg:icmadp:icma-dp2003-06 Short and Long Term Smile Effects: The Binomial Normal Mixture Diffusion Model (2003). (13) RePEc:rdg:icmadp:icma-dp2006-03 Hedging Options with Scale-Invariant Models (2006). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 Latest citations received in: 2001 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |