|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

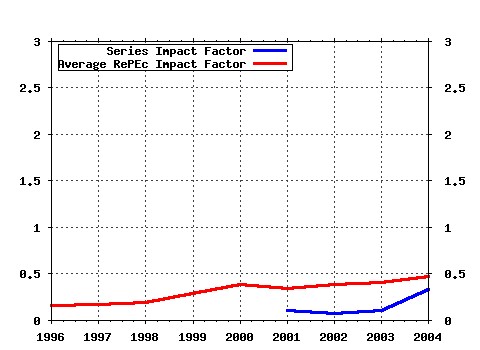

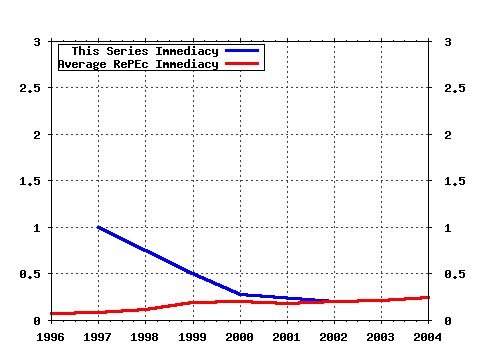

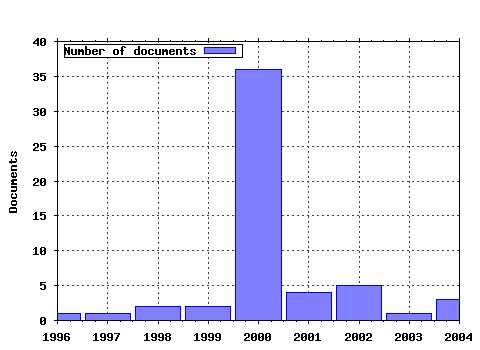

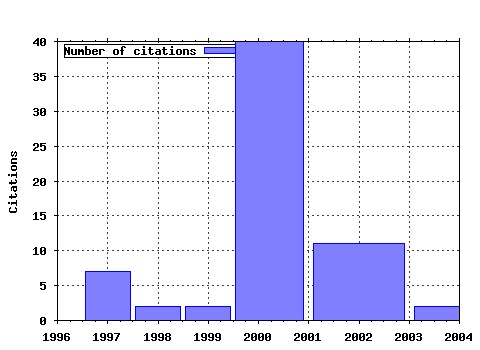

Science & Finance, Capital Fund Management / Science & Finance (CFM) working paper archive Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:sfi:sfiwpa:500028 Herd behavior and aggregate fluctuations in financial markets (2000). (2) RePEc:sfi:sfiwpa:0203511 Statistical properties of stock order books: empirical results and models (2002). (3) RePEc:sfi:sfiwpa:9705087 Scaling in stock market data: stable laws and beyond (1997). (4) RePEc:sfi:sfiwpa:500037 Financial markets as adaptative systems (2000). (5) RePEc:sfi:sfiwpa:500026 Wealth condensation in a simple model of economy (2000). (6) RePEc:sfi:sfiwpa:500027 A Langevin approach to stock market fluctuations and crashes (2000). (7) RePEc:sfi:sfiwpa:500047 An empirical investigation of the forward interest rate term structure (2000). (8) RePEc:sfi:sfiwpa:500023 Power-laws in economics and finance: some ideas from physics (2000). (9) RePEc:sfi:sfiwpa:500033 Hedging large risks reduces the transaction costs (2000). (10) RePEc:sfi:sfiwpa:9906347 Apparent multifractality in financial time series (1999). (11) RePEc:sfi:sfiwpa:500040 The Black-Scholes option pricing problem in mathematical finance: generalization and extensions for a large class of stochastic processes (2000). (12) RePEc:sfi:sfiwpa:500063 Random walks, liquidity molasses and critical response in financial markets (2004). (13) RePEc:sfi:sfiwpa:500051 Noise dressing of financial correlation matrices (1998). (14) RePEc:sfi:sfiwpa:500035 Financial modeling and option theory with the truncated Lévy process (2000). (15) RePEc:sfi:sfiwpa:0204047 The skewed multifractal random walk with applications to option smiles (2002). (16) RePEc:sfi:sfiwpa:500031 Hedged Monte-Carlo: low variance derivative pricing with objective probabilities (2000). (17) RePEc:sfi:sfiwpa:500039 Real-world options: smile and residual risk (2000). (18) RePEc:sfi:sfiwpa:500038 Option pricing in the presence of extreme fluctuations (2000). (19) RePEc:sfi:sfiwpa:500048 Phenomenology of the interest rate curve (2000). (20) RePEc:sfi:sfiwpa:500045 Missing information and asset allocation (2000). (21) RePEc:sfi:sfiwpa:500025 Population dynamics in a random environment (2000). (22) RePEc:sfi:sfiwpa:500053 Random matrix theory and financial correlations (2000). (23) RePEc:sfi:sfiwpa:313238 An introduction to statistical finance (2002). (24) RePEc:sfi:sfiwpa:500049 Strings Attached (2000). Latest citations received in: | 2004 | 2003 | 2002 | 2001 Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 (1) RePEc:sfi:sfiwpa:0210710 More statistical properties of order books and price impact (2002). Science & Finance, Capital Fund Management / Science & Finance (CFM) working paper archive Latest citations received in: 2001 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |