|

|

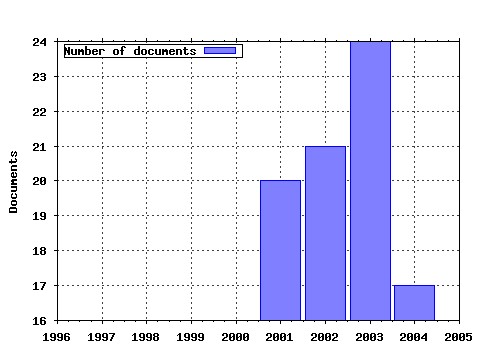

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Abacus Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:bla:abacus:v:37:y:2001:i:2:p:139-165 Institutional Pressures, Monopolistic Conditions and the Implementation of Early Cost Management Practices: The Case of the Royal Tobacco Factory of Seville (1820-1887) (2001). (2) RePEc:bla:abacus:v:39:y:2003:i:1:p:42-65 Shopping Around for Accounting Practices: The Financial Statement Presentation of French Groups (2003). (3) RePEc:bla:abacus:v:37:y:2001:i:1:p:79-109 The Accounting-Clinical Interface-Implementing Budgets for Hospital Doctors (2001). (4) RePEc:bla:abacus:v:41:y:2005:i:2:p:159-180 Accounting for the U.K.s Private Finance Initiative: An Interview-Based Investigation (2005). (5) RePEc:bla:abacus:v:38:y:2002:i:1:p:46-77 Accounting Practice Harmony, Accounting Regulation and Firm Characteristics (2002). (6) RePEc:bla:abacus:v:41:y:2005:i:1:p:21-39 Auditing in the United States: a historical perspective (2005). (7) RePEc:bla:abacus:v:37:y:2001:i:3:p:352-368 The Effects of Fraud Risk and Management Representation on Auditors Hypothesis Generation (2001). (8) RePEc:bla:abacus:v:40:y:2004:i:1:p:21-48 Stock Price Response to News of Securities Fraud Litigation: An Analysis of Sequential and Conditional Information (2004). (9) RePEc:bla:abacus:v:37:y:2001:i:2:p:217-232 Evaluation of Extraordinary and Exceptional Items Disclosed by Hong Kong Companies (2001). (10) RePEc:bla:abacus:v:39:y:2003:i:2:p:233-249 Presenting Discounted Future Cash Receipts and Payments in Financial Statements (2003). (11) RePEc:bla:abacus:v:42:y:2006:i:3-4:p:296-301 Evidence-based financial reporting regulation (2006). (12) RePEc:bla:abacus:v:38:y:2002:i:3:p:425-464 Commonwealth Convergence Toward a Narrower Scope of Auditor Liability to Third Parties for Negligent Misstatements (2002). (13) RePEc:bla:abacus:v:41:y:2005:i:2:p:117-137 Accounting and the Construction of Taste: Standard Labour Costs and the Georgian Cabinet-Maker (2005). (14) RePEc:bla:abacus:v:38:y:2002:i:1:p:1-15 The Value Relevance of Financial Institutions Fair Value Disclosures: A Study in the Difficulty of Linking Unrealized Gains and Losses to Equity Values (2002). (15) RePEc:bla:abacus:v:40:y:2004:i:1:p:49-75 The Profits of the Dutch East India Companys Japan Trade (2004). (16) RePEc:bla:abacus:v:37:y:2001:i:3:p:329-351 The Influence of the Accountant on British Business Performance From the Late Nineteenth Century to the Present Day (2001). (17) RePEc:bla:abacus:v:39:y:2003:i:3:p:279-297 An Evolving Conceptual Framework? (2003). (18) RePEc:bla:abacus:v:37:y:2001:i:2:p:188-216 Contextualizing the Process of Accounting Regulation: A Study of Nineteenth-Century British Friendly Societies (2001). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 (1) RePEc:tky:fseres:2002cf171 Concept and Relevance of Income (2002). CIRJE, Faculty of Economics, University of Tokyo / CIRJE F-Series Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |