|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

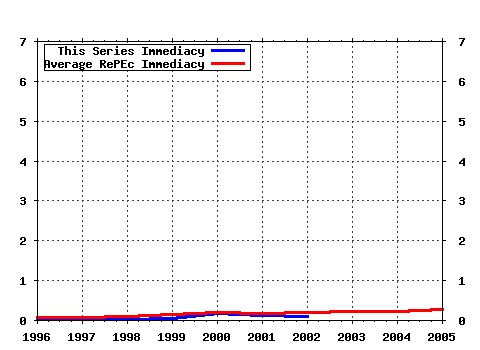

Econometric Reviews Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:taf:emetrv:v:11:y:1992:i:2:p:143-172 Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances (1992). (2) RePEc:taf:emetrv:v:3:y:1984:i:1:p:1-100 Forecasting and conditional projection using realistic prior distributions (1984). (3) RePEc:taf:emetrv:v:19:y:2000:i:3:p:321-340 GMM Estimation with persistent panel data: an application to production functions (2000). (4) RePEc:taf:emetrv:v:15:y:1996:i:3:p:197-235 A test for independence based on the correlation dimension (1996). (5) RePEc:taf:emetrv:v:15:y:1996:i:2:p:115-158 Bootstrapping time series models (1996). (6) RePEc:taf:emetrv:v:15:y:1996:i:4:p:369-386 Making wald tests work for cointegrated VAR systems (1996). (7) RePEc:taf:emetrv:v:13:y:1994:i:1:p:1-91 Artificial neural networks: an econometric perspective (1994). (8) RePEc:taf:emetrv:v:17:y:1998:i:1:p:57-84 A residual-based test of the null of cointegration in panel data (1998). (9) RePEc:taf:emetrv:v:13:y:1994:i:2:p:205-229 The role of the constant and linear terms in cointegration analysis of nonstationary variables (1994). (10) RePEc:taf:emetrv:v:2:y:1983:i:2:p:159-218 Diagnostic tests as residual analysis (1983). (11) RePEc:taf:emetrv:v:11:y:1992:i:3:p:265-306 Testing the lucas critique: A review (1992). (12) RePEc:taf:emetrv:v:11:y:1992:i:1:p:1-71 The econometrics of female labor supply and children (1992). (13) RePEc:taf:emetrv:v:13:y:1994:i:2:p:259-285 Vector autoregression and causality: a theoretical overview and simulation study (1994). (14) RePEc:taf:emetrv:v:21:y:2002:i:1:p:49-87 LONG-RUN STRUCTURAL MODELLING (2002). (15) RePEc:taf:emetrv:v:5:y:1986:i:1:p:51-56 Modeling The persistence Of Conditional Variances: A Comment (1986). (16) RePEc:taf:emetrv:v:20:y:2001:i:3:p:247-318 A REVIEW OF SYSTEMS COINTEGRATION TESTS (2001). (17) RePEc:taf:emetrv:v:19:y:2000:i:3:p:263-286 Nonstationary panel data analysis: an overview of some recent developments (2000). (18) RePEc:taf:emetrv:v:21:y:2002:i:1:p:1-47 SMOOTH TRANSITION AUTOREGRESSIVE MODELS - A SURVEY OF RECENT DEVELOPMENTS (2002). (19) RePEc:taf:emetrv:v:5:y:1986:i:1:p:1-50 Modelling the persistence of conditional variances (1986). (20) RePEc:taf:emetrv:v:8:y:1989:i:2:p:207-212 Econometric tests of rationality and market efficiency (1989). (21) RePEc:taf:emetrv:v:8:y:1989:i:2:p:151-186 Econometric tests of rationality and market efficiency (1989). (22) RePEc:taf:emetrv:v:17:y:1998:i:1:p:1-29 Confidence intervals for impulse responses under departures from normality (1998). (23) RePEc:taf:emetrv:v:15:y:1996:i:3:p:261-274 Nonparametric testing of closeness between two unknown distribution functions (1996). (24) RePEc:taf:emetrv:v:9:y:1990:i:2:p:123-184 Specification of household engel curves by nonparametric regression (1990). (25) RePEc:taf:emetrv:v:19:y:2000:i:1:p:1-48 Recent developments in bootstrapping time series (2000). (26) RePEc:taf:emetrv:v:18:y:1999:i:3:p:287-330 An introduction to hypergeometric functions for economists (1999). (27) RePEc:taf:emetrv:v:12:y:1993:i:3:p:261-330 Modeling asset returns with alternative stable distributions (1993). (28) RePEc:taf:emetrv:v:26:y:2007:i:2-4:p:113-172 Bayesian Analysis of DSGE Models (2007). (29) RePEc:taf:emetrv:v:7:y:1988:i:1:p:65-95 Prediction theory for autoregressivemoving average processes (1988). (30) RePEc:taf:emetrv:v:9:y:1990:i:2:p:211-240 Testing purchasing power parity: some evidence of the effects of transaction costs (1990). (31) RePEc:taf:emetrv:v:24:y:2005:i:4:p:369-404 (). (32) RePEc:taf:emetrv:v:12:y:1993:i:2:p:137-181 A compendium to information theory in economics and econometrics (1993). (33) RePEc:taf:emetrv:v:21:y:2002:i:3:p:309-336 A MONTE CARLO COMPARISON OF VARIOUS ASYMPTOTIC APPROXIMATIONS TO THE DISTRIBUTION OF INSTRUMENTAL VARIABLES ESTIMATORS (2002). (34) RePEc:taf:emetrv:v:19:y:2000:i:1:p:55-68 Bootstrap tests: how many bootstraps? (2000). (35) RePEc:taf:emetrv:v:1:y:1982:i:2:p:151-190 On unification of the asymptotic theory of nonlinear econometric models (1982). (36) RePEc:taf:emetrv:v:12:y:1993:i:1:p:1-32 Testing stationarity and trend stationarity against the unit root hypothesis (1993). (37) RePEc:taf:emetrv:v:12:y:1993:i:2:p:183-216 An introduction to econometric applications of empirical process theory for dependent random variables (1993). (38) RePEc:taf:emetrv:v:10:y:1991:i:3:p:253-325 Basic structure of the asymptotic theory in dynamic nonlinear econometric models (1991). (39) RePEc:taf:emetrv:v:19:y:2000:i:4:p:312-320 Estimation and decomposition of productivity change when production is not efficient: a paneldata approach (2000). (40) RePEc:taf:emetrv:v:21:y:2002:i:3:p:273-307 SEPARATION, WEAK EXOGENEITY, AND P-T DECOMPOSITION IN COINTEGRATED VAR SYSTEMS WITH COMMON FEATURES (2002). (41) RePEc:taf:emetrv:v:10:y:1991:i:1:p:1-59 State space modeling of multiple time series (1991). (42) RePEc:taf:emetrv:v:18:y:1999:i:1:p:1-73 Using simulation methods for bayesian econometric models: inference, development,and communication (1999). (43) RePEc:taf:emetrv:v:6:y:1987:i:2:p:257-270 Semi parametric estimation of employment duration models (1987). (44) RePEc:taf:emetrv:v:15:y:1996:i:4:p:401-429 Testing for structural change in cointegrated regression models: some comparisons and generalizations (1996). (45) RePEc:taf:emetrv:v:21:y:2002:i:4:p:431-447 ON THE ASYMPTOTICS OF ADF TESTS FOR UNIT ROOTS (2002). (46) RePEc:taf:emetrv:v:17:y:1998:i:2:p:185-214 Inference on cointegrating ranks using lr and lm tests based on pseudo-likelihoods (1998). (47) RePEc:taf:emetrv:v:19:y:2000:i:3:p:341-366 Estimation of tobit-type models with individual specific effects (2000). (48) RePEc:taf:emetrv:v:3:y:1984:i:2:p:211-242 Tests of specification in econometrics (1984). (49) RePEc:taf:emetrv:v:6:y:1987:i:1:p:5-40 Semiparametric estimation of employment duration models (1987). (50) RePEc:taf:emetrv:v:13:y:1994:i:3:p:291-336 A bayesian analysis of trend determination in economic time series (1994). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 Latest citations received in: 2004 Latest citations received in: 2003 Latest citations received in: 2002 (1) RePEc:ins:quaeco:qf0216 Testing for common trends in conditional I(2) VAR models (2002). Department of Economics, University of Insubria / Economics and Quantitative Methods (2) RePEc:tud:ddpiec:113 Seasonal Unit Root Tests under Structural Breaks (2002). Institut für Volkswirtschaftslehre (Department of Economics), Technische Universität Darmstadt (Darmstadt University of Technology) / Darmstadt Disc Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |