|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

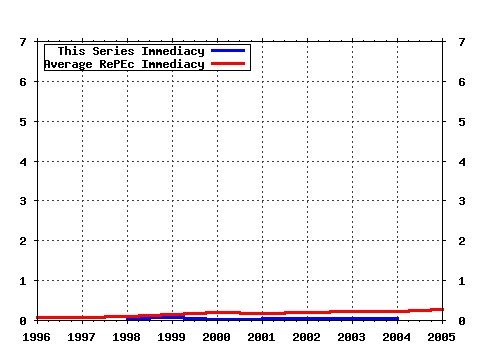

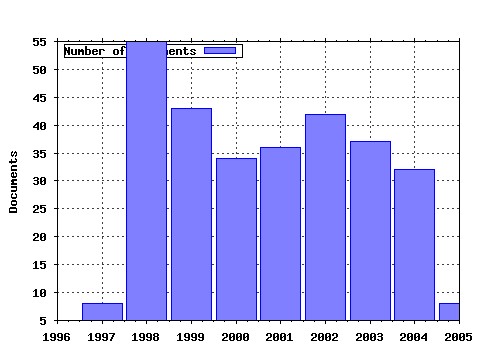

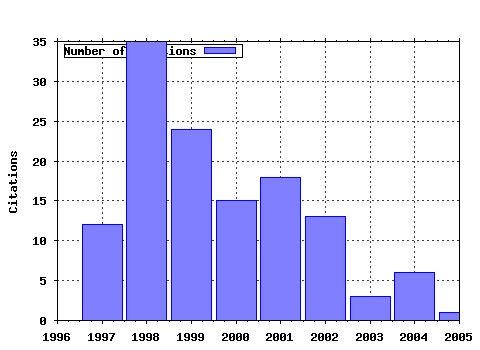

European Accounting Review Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:taf:euract:v:8:y:1999:i:2:p:383-395 Financial information on the Internet: a survey of the homepages of Austrian companies (1999). (2) RePEc:taf:euract:v:8:y:1999:i:2:p:365-371 External reporting of accounting and financial information via the Internet in Spain (1999). (3) RePEc:taf:euract:v:6:y:1998:i:3:p:355-375 Auditor independence, incomplete contracts and the role of legal liability (1998). (4) RePEc:taf:euract:v:8:y:1999:i:2:p:373-381 The Internet as a vehicle for investor relations: the Swedish case (1999). (5) RePEc:taf:euract:v:8:y:1999:i:2:p:321-333 Financial reporting on the Internet by leading UK companies (1999). (6) RePEc:taf:euract:v:13:y:2004:i:1:p:131-159 The adjustment of financial ratios in the presence of soft budget constraints: evidence from Bulgaria (2004). (7) RePEc:taf:euract:v:6:y:1997:i:1:p:69-81 Finnish earnings response coefficients: the information content of losses (1997). (8) RePEc:taf:euract:v:7:y:1998:i:4:p:723-751 The development of the role of the audit in the Czech Republic (1998). (9) RePEc:taf:euract:v:7:y:1998:i:3:p:407-440 The development of the role of the statutory audit in the transitional Polish economy (1998). (10) RePEc:taf:euract:v:8:y:1999:i:1:p:93-113 The Spanish accounting system and international accounting harmonization (1999). (11) RePEc:taf:euract:v:9:y:2000:i:1:p:7-29 Environmental disclosures in the annual reports of large companies in Spain (2000). (12) RePEc:taf:euract:v:11:y:2002:i:1:p:153-190 Financial accounting developments in the European Union: past events and future prospects (2002). (13) RePEc:taf:euract:v:9:y:2000:i:3:p:349-369 Evaluating the statistical significance of de facto accounting harmonization: a study of European global players (2000). (14) RePEc:taf:euract:v:10:y:2001:i:1:p:51-72 Measurement of harmony of financial reporting within and between countries: the case of the Nordic countries (2001). (15) RePEc:taf:euract:v:7:y:1998:i:4:p:675-696 The early adoption of consolidated accounting in Spain (1998). (16) RePEc:taf:euract:v:7:y:1998:i:2:p:289-314 International accounting education in Western Europe (1998). (17) RePEc:taf:euract:v:7:y:1998:i:1:p:105-124 The usefulness of earnings in explaining stock returns in an emerging market: the case of Cyprus (1998). (18) RePEc:taf:euract:v:8:y:1999:i:1:p:67-92 Comparative analysis of failure prediction methods: the Finnish case (1999). (19) RePEc:taf:euract:v:6:y:1997:i:1:p:85-108 The enigma of the Greek auditing profession: some preliminary results concerning the impact of liberalization on auditor behaviour (1997). (20) RePEc:taf:euract:v:7:y:1998:i:3:p:541-569 Audit independence and nonaudit services: a comparative study in differing British and French perspectives (1998). (21) RePEc:taf:euract:v:6:y:1997:i:1:p:45-68 The influence of company characteristics and accounting regulation on information disclosed by Spanish firms (1997). (22) RePEc:taf:euract:v:11:y:2002:i:3:p:537-572 Do managers perform better under EVA bonus schemes? (2002). (23) RePEc:taf:euract:v:7:y:1998:i:2:p:331-333 The future shape of harmonization: a reply (1998). (24) RePEc:taf:euract:v:8:y:1999:i:3:p:481-491 Earnings manipulation: cost of capital versus tax (1999). (25) RePEc:taf:euract:v:7:y:1998:i:2:p:275-288 The Contingency Model of Governmental Accounting Innovations: a discussion (1998). (26) RePEc:taf:euract:v:7:y:1998:i:3:p:467-491 Disciplinary practices and auditors in Europe: a comparison between Germany and the Netherlands (1998). (27) RePEc:taf:euract:v:7:y:1998:i:2:p:163-183 Accounting earnings and firm valuation: the French case (1998). (28) RePEc:taf:euract:v:6:y:1997:i:1:p:19-44 Activity-based techniques and the death of the beancounter (1997). (29) RePEc:taf:euract:v:8:y:1999:i:2:p:335-350 Financial reporting on the Internet and the external audit (1999). (30) RePEc:taf:euract:v:8:y:1999:i:4:p:585-607 Regularities in the equity price response to earnings announcements in Spain (1999). (31) RePEc:taf:euract:v:13:y:2004:i:2:p:373-390 Accounting for derivatives: An evaluation of reporting practice by UK banks (2004). (32) RePEc:taf:euract:v:10:y:2001:i:1:p:133-147 European languages of account (2001). (33) RePEc:taf:euract:v:10:y:2001:i:3:p:407-437 Measuring to understand intangible performance drivers (2001). (34) RePEc:taf:euract:v:12:y:2003:i:3:p:567-579 Investor relations on the Internet: a survey of the Euronext zone (2003). (35) RePEc:taf:euract:v:11:y:2002:i:4:p:741-773 The impact of voluntary corporate disclosures on the ex-ante cost of capital for Swiss firms (2002). (36) RePEc:taf:euract:v:7:y:1998:i:2:p:185-208 Reforming the reform: changing roles for accounting and management in the Italian health care sector (1998). (37) RePEc:taf:euract:v:10:y:2001:i:1:p:33-50 Cost management and value creation: the missing link (2001). (38) RePEc:taf:euract:v:8:y:1999:i:4:p:609-629 The value relevance of earnings disaggregation provided in the Spanish profit and loss account (1999). (39) RePEc:taf:euract:v:7:y:1998:i:4:p:655-673 Towards the establishment of an internal market for audit services within the European Union (1998). (40) RePEc:taf:euract:v:10:y:2001:i:3:p:505-522 Caught in an evaluatory trap: a dilemma for public services under NPFM (2001). (41) RePEc:taf:euract:v:10:y:2001:i:1:p:107-131 The relationship between accounting numbers and returns: some empirical evidence from the emerging market of the Czech Republic (2001). (42) RePEc:taf:euract:v:7:y:1998:i:4:p:579-604 The role of accrual accounting in restricting dividends to shareholders (1998). (43) RePEc:taf:euract:v:9:y:2000:i:4:p:477-498 Occupational identity of management accountants in Britain and Germany (2000). (44) RePEc:taf:euract:v:10:y:2001:i:2:p:361-383 New opportunities for farm accounting (2001). (45) RePEc:taf:euract:v:12:y:2003:i:2:p:327-355 Intangibles and credit decisions: results from an experiment (2003). (46) RePEc:taf:euract:v:7:y:1998:i:2:p:209-236 The politics of accounting technology in Danish central government (1998). (47) RePEc:taf:euract:v:8:y:1999:i:1:p:51-65 The future of auditing: the debate in the UK (1999). (48) RePEc:taf:euract:v:9:y:2000:i:1:p:31-52 Environmental management accounting in Europe: current practice and future potential (2000). (49) RePEc:taf:euract:v:10:y:2001:i:4:p:843-867 The emergence of the Big Five in Sweden (2001). (50) RePEc:taf:euract:v:11:y:2002:i:3:p:573-599 Empirical evidence of the effect of European accounting differences on the stock market valuation of earnings and book value (2002). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 Latest citations received in: 2004 (1) RePEc:hhs:bofitp:2004_012 The Political Economy of Restructuring and Subsidisation: An International Perspective (2004). Bank of Finland, Institute for Economies in Transition / BOFIT Discussion Papers (2) RePEc:por:fepwps:150 Accounting practices for financial instruments. How far are Portuguese companies from IAS? (2004). Universidade do Porto, Faculdade de Economia do Porto / FEP Working Papers Latest citations received in: 2003 Latest citations received in: 2002 (1) RePEc:dgr:umamet:2002069 Voluntary adoption of non-local GAAP in the European Union: a study of determinants (2002). Maastricht : METEOR, Maastricht Research School of Economics of Technology and Organization / Research Memoranda (2) RePEc:taf:euract:v:11:y:2002:i:1:p:33-41 Creating a new community: the establishment and development of the European Accounting Association (2002). European Accounting Review Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |