|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

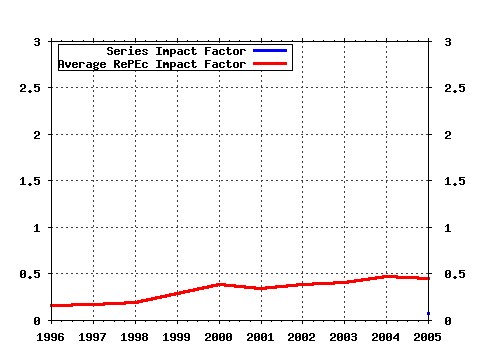

EconWPA / Risk and Insurance Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Latest citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:wpa:wuwpri:0501003 Interest-rate risk in the Indian banking system (2005). (2) RePEc:wpa:wuwpri:0404001 Optimization of Convex Risk Functions (2004). (3) RePEc:wpa:wuwpri:0403001 Value-at-Risk and Expected Shortfall for Linear Portfolios with elliptically distributed RisK Factors (2004). (4) RePEc:wpa:wuwpri:0506002 A Fast Algorithm for Computing Expected Loan Portfolio Tranche Loss in the Gaussian Factor Model. (2005). (5) RePEc:wpa:wuwpri:0306002 Dynamic Financial Analysis - Understanding Risk and Value Creation in Insurance (2003). (6) RePEc:wpa:wuwpri:0509001 Value-at-Risk: The Delta-normal Approach (2005). (7) RePEc:wpa:wuwpri:0308003 From Fault Tree to Credit Risk Assessment: An Empirical Attempt (2003). (8) RePEc:wpa:wuwpri:0404002 Conditional Risk Mappings (2005). Latest citations received in: | 2005 | 2004 | 2003 | 2002 Latest citations received in: 2005 (1) RePEc:wpa:wuwpfi:0506015 Using Hermite Expansions for Fast and Arbitrarily Accurate Computation of the Expected Loss of a Loan Portfolio Tranche in the Gaussian Factor Model (2005). EconWPA / Finance (2) RePEc:wpa:wuwpri:0507004 Fast Computation of the Economic Capital, the Value at Risk and the Greeks of a Loan Portfolio in the Gaussian Factor Model (2005). EconWPA / Risk and Insurance Latest citations received in: 2004 (1) RePEc:wpa:wuwpge:0403003 VaR and ES for linear Portfolis with mixture of elliptically distributed Risk Factors. (2004). EconWPA / GE, Growth, Math methods (2) RePEc:wpa:wuwpge:0403004 VaR and ES for linear Portfolios with mixture of elliptically distributed Risk Factors. (2004). EconWPA / GE, Growth, Math methods (3) RePEc:wpa:wuwpri:0406001 VaR and ES for Linear Portfolios with mixture of Generalized Laplace Distributed Risk Factors (2004). EconWPA / Risk and Insurance (4) RePEc:wpa:wuwpri:0407002 Optimization of Risk Measures (2004). EconWPA / Risk and Insurance Latest citations received in: 2003 (1) RePEc:wpa:wuwpri:0311001 Performance and Risk Measurement Challenges For Hedge Funds: Empirical Considerations (2003). EconWPA / Risk and Insurance Latest citations received in: 2002 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |