|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

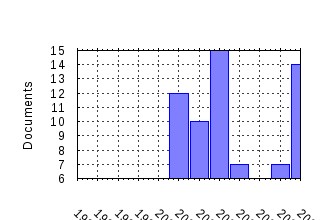

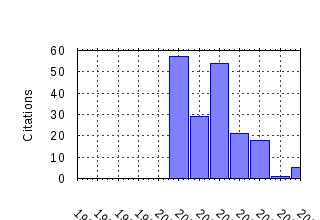

ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:icr:wpmath:11-2003 A smooth model of decision making under ambiguity. (2003). (2) RePEc:icr:wpmath:17-2001 A subjective spin on roulette wheels. (2001). (3) RePEc:icr:wpmath:18-2001 Optimal two-object auctions with synergies. (2001). (4) RePEc:icr:wpmath:11-2001 Expected utility theory without the completeness axiom. (2001). (5) RePEc:icr:wpmath:17-2002 Ambiguity from the Differential Viewpoint. (2002). (6) RePEc:icr:wpmath:05-2002 Multivariate Option Pricing with Copulas. (2002). (7) RePEc:icr:wpmath:05-2001 On Fragility of Bubbles in Equilibrium Asset Pricing Models of Lucas-Type. (2001). (8) RePEc:icr:wpmath:12-2001 Random correspndences as bundles of random variables. (2001). (9) RePEc:icr:wpmath:4-2005 Non mean reverting affine processes for stochastic mortality. (2005). (10) RePEc:icr:wpmath:21-2001 Risk, ambiguity, and the separation of utility and beliefs. (2001). (11) RePEc:icr:wpmath:23-2001 Credit rationing, wealth inequality, and allocation of talent. (2001). (12) RePEc:icr:wpmath:13-2003 Ultramodular functions. (2003). (13) RePEc:icr:wpmath:30-2003 Monotone Continuous Multiple Priors. (2003). (14) RePEc:icr:wpmath:30-2001 Yaari dual theory without the completeness axiom. (2001). (15) RePEc:icr:wpmath:06-2002 Pricing Vulnerable Options with Copulas. (2002). (16) RePEc:icr:wpmath:40-2002 Certainty Independence and the Separation of Utility and Beliefs. (2002). (17) RePEc:icr:wpmath:39-2002 Wealth Polarization and Pulverization in Fractal Societies. (2002). (18) RePEc:icr:wpmath:27-2004 Portfolio Selection with Monotone Mean-Variance Preferences. (2004). (19) RePEc:icr:wpmath:16-2003 Multidimensional generalized Gini indices. (2003). (20) RePEc:icr:wpmath:10-2002 Coherence without Additivity. (2002). (21) RePEc:icr:wpmath:24-2002 Insurance Premia Consistent with the Market. (2002). (22) RePEc:icr:wpmath:02-2003 Existence of solutions and asset pricing bubbles in general equilibrium models. (2003). (23) RePEc:icr:wpmath:07-2003 Cores and stable sets of finite dimensional games. (2003). (24) RePEc:icr:wpmath:15-2003 Unequal uncertainties and uncertain inequalities: an axiomatic approach. (2003). (25) RePEc:icr:wpmath:14-2003 Choquet insurance pricing: a caveat. (2003). (26) RePEc:icr:wpmath:01-2003 The convexity-cone approach to comparative risk and downside risk. (2003). (27) RePEc:icr:wpmath:6-2005 A Multivariate Jump-Driven Financial Asset Model. (2005). (28) RePEc:icr:wpmath:10-2003 A folk theorem for minority games. (2003). (29) RePEc:icr:wpmath:05-2004 Variational representation of preferences under ambiguity. (2004). (30) RePEc:icr:wpmath:18-2003 Decision Making with Imprecise Probabilistic Information. (2003). (31) RePEc:icr:wpmath:26-2003 Positive value of information in games. (2003). (32) RePEc:icr:wpmath:09-2001 Subcalculus for set functions and cores of TU games. (2001). (33) RePEc:icr:wpmath:25-2003 Archimedean Copulae and Positive Dependence. (2003). (34) RePEc:icr:wpmath:27-2003 Zonoids, Linear Dependence, and Size-Biased Distributions on the Simplex. (2003). (35) RePEc:icr:wpmath:28-2003 Some Counterexamples in Positive Dependence. (2003). (36) RePEc:icr:wpmath:28-2004 A strong law of large numbers for capacities. (2004). (37) RePEc:icr:wpmath:11-2007 Modeling Long Memory and Structural Breaks in Conditional Variances: an Adaptive FIGARCH Approach (2007). (38) RePEc:icr:wpmath:29-2001 BV as a dual space. (2001). (39) RePEc:icr:wpmath:13-2004 Contributions to the understanding of Bayesian consistency. (2004). (40) RePEc:icr:wpmath:08-2001 Probabilistic sophistication and multiple priors. (2001). (41) RePEc:icr:wpmath:5-2005 Bayesian Inference via Classes of Normalized Random Measures. (2005). (42) RePEc:icr:wpmath:09-2002 Optimal investment strategies and risk measures in defined contribution pension

schemes. (2002). (43) RePEc:icr:wpmath:12-2004 Hierarchical mixture modelling with normalized inverse Gaussian priors. (2004). (44) RePEc:icr:wpmath:6-2006 Credit risk in pure jump structural models (2006). (45) RePEc:icr:wpmath:14-2007 Construction and Stationary Distribution of the Fleming-Viot Process with Viability Selection (2007). (46) RePEc:icr:wpmath:5-2007 Bank Efficiency and Banking Sector Development: the Case of Italy (2007). (47) RePEc:icr:wpmath:12-2005 Calibrating risk-neutral default correlation. (2005). Recent citations received in: | 2007 | 2006 | 2005 | 2004 Recent citations received in: 2007 (1) RePEc:icr:wpmath:18-2007 The Neutral Population Model and Bayesian Nonparametrics (2007). ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series Recent citations received in: 2006 Recent citations received in: 2005 Recent citations received in: 2004 (1) RePEc:clu:wpaper:0405-09 Ambiguous events and Maxmin Expected Utility (2004). Columbia University, Department of Economics / Discussion Papers (2) RePEc:clu:wpaper:0405-10 States, models and unitary equivalence I: Representation theorems and analogical reasoning (2004). Columbia University, Department of Economics / Discussion Papers (3) RePEc:icr:wpmath:13-2004 Contributions to the understanding of Bayesian consistency. (2004). ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series (4) RePEc:icr:wpmath:23-2004 On consistency of nonparametric normal mixtures for Bayesian density estimation. (2004). ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series (5) RePEc:icr:wpmath:24-2004 On rates of convergence for posterior distributions in infiniteâdimensional models. (2004). ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series (6) RePEc:icr:wpmath:27-2004 Portfolio Selection with Monotone Mean-Variance Preferences. (2004). ICER - International Centre for Economic Research / ICER Working Papers - Applied Mathematics Series Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||