|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

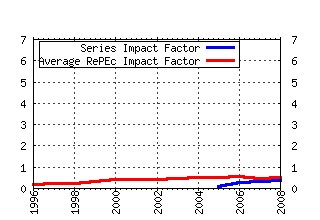

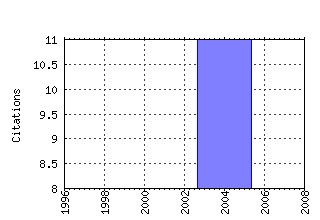

The Geneva Papers on Risk and Insurance Theory Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:kap:geneva:v:31:y:2006:i:2:p:111-146 (). (2) RePEc:kap:geneva:v:32:y:2007:i:1:p:1-36 Overconfidence and trading volume (2007). (3) RePEc:kap:geneva:v:29:y:2004:i:1:p:55-74 Labor Income Risk and Car Insurance in the UK (2004). (4) RePEc:kap:geneva:v:29:y:2004:i:1:p:43-54 Health and Wealth: How do They Affect Individual Preferences? (2004). (5) RePEc:kap:geneva:v:30:y:2005:i:1:p:41-55 (). (6) RePEc:kap:geneva:v:29:y:2004:i:1:p:75-108 The Effective Duration and Convexity of Liabilities for Property-Liability Insurers Under Stochastic Interest Rates (2004). (7) RePEc:kap:geneva:v:32:y:2007:i:2:p:147-167 Screening equilibria in experimental markets (2007). (8) RePEc:kap:geneva:v:32:y:2007:i:2:p:113-128 The optimal assetÃÂ allocation of the main types of pension funds: a unified framework (2007). (9) RePEc:kap:geneva:v:29:y:2004:i:1:p:5-22 Infrequent Extreme Risks (2004). (10) RePEc:kap:geneva:v:30:y:2005:i:1:p:71-97 (). (11) RePEc:kap:geneva:v:29:y:2004:i:2:p:165-186 Reimbursing Preventive Care (2004). (12) RePEc:kap:geneva:v:32:y:2007:i:1:p:61-90 On the role of market insurance in a dynamic model (2007). Recent citations received in: | 2008 | 2007 | 2006 | 2005 Recent citations received in: 2008 Recent citations received in: 2007 (1) RePEc:pra:mprapa:5228 Hedging Strategies in Forest Management (2007). University Library of Munich, Germany / MPRA Paper (2) RePEc:pra:mprapa:6497 Investor Overconfidence and the Forward Discount Puzzle (2007). University Library of Munich, Germany / MPRA Paper Recent citations received in: 2006 Recent citations received in: 2005 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||