|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Warwick Business School, Financial Econometrics Research Centre / Working Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

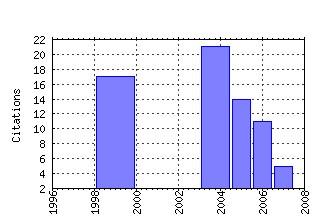

Most cited documents in this series: (1) RePEc:wbs:wpaper:wp99-17 Modelling Emerging Market Risk Premia Using Higher Moments (1999). (2) RePEc:wbs:wpaper:wp05-02 Time-Variation of Higher Moments in a Financial Market with Heterogeneous Agents: An Analytical Approach (2005). (3) RePEc:wbs:wpaper:wp04-05 Properties of Optimal Forecasts under Asymmetric Loss and Nonlinearity (2004). (4) RePEc:wbs:wpaper:wp05-13 The Empirical Failure of the Expectations Hypothesis of the Term Structure of Bond Yields (2005). (5) RePEc:wbs:wpaper:wp06-18 Price Stability and Volatility in Markets with Positive and Negative Expectations Feedback: An Experimental Investigation (2006). (6) RePEc:wbs:wpaper:wp04-16 Predictive Density Accuracy Tests (2004). (7) RePEc:wbs:wpaper:wp04-19 Simple Tests for Models of Dependence Between Multiple Financial Time Series, with Applications to U.S. Equity Returns and Exchange Rates (2004). (8) RePEc:wbs:wpaper:wp06-17 Dynamic instability in a phenomenological model of correlated assets (2006). (9) RePEc:wbs:wpaper:wp06-08 Effects of Tobin Taxes in Minority Game Markets (2006). (10) RePEc:wbs:wpaper:wp04-14 Properties of Realized Variance for a Pure Jump Process: Calendar Time Sampling versus Business Time Sampling (2004). (11) RePEc:wbs:wpaper:wp07-08 A Prototype Model of Speculative Dynamics With Position-Based Trading (2007). (12) RePEc:wbs:wpaper:wp99-21 How do UK-Based Foreign Exchange Dealers Think Their Market Operates? (1999). (13) RePEc:wbs:wpaper:wp04-11 Modeling and Forecasting Stock Returns: Exploiting the Futures Market, Regime Shifts and International Spillovers (2004). (14) RePEc:wbs:wpaper:wp07-02 Should Network Structure Matter in Agent-Based Finance? (2007). (15) RePEc:wbs:wpaper:wp05-10 Incentive Contracts and Hedge Fund Management (2005). (16) RePEc:wbs:wpaper:wp04-08 Is Seasonal Heteroscedasticity Real? An International Perspective (2004). (17) RePEc:wbs:wpaper:wp01-09 Numerical Issues in Threshold Autoregressive Modelling of Time Series (2001). (18) RePEc:wbs:wpaper:wp05-11 Towards a Solution to the Puzzles in Exchange Rate Economics: Where Do We Stand? (2005). (19) RePEc:wbs:wpaper:wp04-10 Empirical Exchange Rate Models and Currency Risk: Some Evidence from Density Forecasts (2004). (20) RePEc:wbs:wpaper:wp06-19 The Markov-Switching Multifractal Model of Asset Returns: GMM Estimation and Linear Forecasting of Volatility (2006). (21) RePEc:wbs:wpaper:wp05-09 Employee Stock Options: Much More Valuable Than You Thought (2005). (22) RePEc:wbs:wpaper:wp99-07 An Analysis of the Performance of European Foreign Exchange Forecasters (1999). (23) RePEc:wbs:wpaper:wp04-06 Testing and Modelling Market Microstructure Effects with an Application to the Dow Jones Industrial Average (2004). (24) RePEc:wbs:wpaper:wp99-02 Intraday Technical Trading in the Foreign Exchange Market (1999). (25) RePEc:wbs:wpaper:wp02-10 Reinterpreting the Real Exchange Rate - Yield Diffential Nexus (2002). (26) RePEc:wbs:wpaper:wp01-15 Tracking Error: Ex-Ante versus Ex-Post Measures (2001). (27) RePEc:wbs:wpaper:wp99-11 On the Evolution of Credibility and Flexible Exchange Rate Target Zones (1999). (28) RePEc:wbs:wpaper:wp99-04 Technical Analysis and Central Bank Intervention (1999). (29) RePEc:wbs:wpaper:wp06-15 A Behavioral Model for Participation Games with Negative Feedback (2006). (30) RePEc:wbs:wpaper:wp07-11 Rational Forecasts or Social Opinion Dynamics? Identification of Interaction Effects in a Business Climate Survey (2007). (31) RePEc:wbs:wpaper:wp02-08 Testing Mertons Model for Credit Spreads on Zero-Coupon Bonds (2002). (32) RePEc:wbs:wpaper:wp06-02 Price and Wealth Dynamics in a Speculative Market with Generic Procedurally Rational Traders (2006). (33) RePEc:wbs:wpaper:wp04-12 Federal Funds Rate Prediction (2004). (34) RePEc:wbs:wpaper:wp07-07 Estimation of a Microfounded Herding Model On German Survey Expectations (2007). Recent citations received in: | 2008 | 2007 | 2006 | 2005 Recent citations received in: 2008 Recent citations received in: 2007 Recent citations received in: 2006 (1) RePEc:ams:ndfwpp:06-10 A Behavioral Model for Participation Games with Negative Feedback (2006). Universiteit van Amsterdam, Center for Nonlinear Dynamics in Economics and Finance / CeNDEF Working Papers (2) RePEc:dgr:uvatin:20060073 A Behavioral Model for Participation Games with Negative Feedback (2006). Tinbergen Institute / Tinbergen Institute Discussion Papers (3) RePEc:nbr:nberwo:12797 Multifrequency Jump-Diffusions: An Equilibrium Approach (2006). National Bureau of Economic Research, Inc / NBER Working Papers Recent citations received in: 2005 (1) RePEc:kap:compec:v:26:y:2005:i:1:p:19-49 Estimation of Agent-Based Models: The Case of an Asymmetric Herding Model (2005). Computational Economics (2) RePEc:zbw:cauewp:3559 A noise trader model as a generator of apparent financial power laws and long memory (2005). Christian-Albrechts-University of Kiel, Department of Economics / Economics working papers Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||