|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

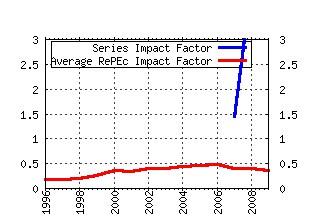

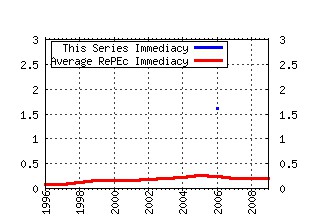

Handbook of Economic Forecasting Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:eee:ecofch:1-04 Forecast Combinations (2006). (2) RePEc:eee:ecofch:1-03 Forecast Evaluation (2006). (3) RePEc:eee:ecofch:1-05 Predictive Density Evaluation (2006). (4) RePEc:eee:ecofch:1-10 Forecasting with Many Predictors (2006). (5) RePEc:eee:ecofch:1-15 Volatility and Correlation Forecasting (2006). (6) RePEc:eee:ecofch:1-17 Forecasting with Real-Time Macroeconomic Data (2006). (7) RePEc:eee:ecofch:1-01 Bayesian Forecasting (2006). (8) RePEc:eee:ecofch:1-14 Survey Expectations (2006). (9) RePEc:eee:ecofch:1-12 Forecasting with Breaks (2006). (10) RePEc:eee:ecofch:1-09 Approximate Nonlinear Forecasting Methods (2006). (11) RePEc:eee:ecofch:1-08 Forecasting economic variables with nonlinear models (2006). (12) RePEc:eee:ecofch:1-07 Forecasting with Unobserved Components Time Series Models (2006). (13) RePEc:eee:ecofch:1-16 Leading Indicators (2006). (14) RePEc:eee:ecofch:1-02 Forecasting and Decision Theory (2006). (15) RePEc:eee:ecofch:1-11 Forecasting with Trending Data (2006). (16) RePEc:eee:ecofch:1-06 Forecasting with VARMA Models (2006). (17) RePEc:eee:ecofch:1-13 Forecasting Seasonal Time Series (2006). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 Recent citations received in: 2008 Recent citations received in: 2007 Recent citations received in: 2006 (1) RePEc:ags:umdrwp:28556 Time Series Analysis (2006). Working Papers (2) RePEc:bdm:wpaper:2006-08 Forecast Combination with Entry and Exit of Experts (2006). Working Papers (3) RePEc:cam:camdae:0649 Time-Varying Quantiles (2006). Cambridge Working Papers in Economics (4) RePEc:ces:ceswps:_1870 Econometrics: A Birdâs Eye View (2006). CESifo Working Paper Series (5) RePEc:chb:bcchwp:376 Shrinkage Based Tests of the Martingale Difference Hypothesis (2006). Working Papers Central Bank of Chile (6) RePEc:col:000094:003230 Modelling autoregressive processes with a shifting mean (2006). BORRADORES DE ECONOMIA (7) RePEc:cpr:ceprdp:5485 Forecasting Economic Aggregates by Disaggregates (2006). CEPR Discussion Papers (8) RePEc:cpr:ceprdp:6012 A Simple Benchmark for Forecasts of Growth and Inflation (2006). CEPR Discussion Papers (9) RePEc:ecb:ecbwps:20060584 A new theory of forecasting. (2006). Working Paper Series (10) RePEc:ecb:ecbwps:20060589 Forecasting economic aggregates by disaggregates. (2006). Working Paper Series (11) RePEc:fip:fedgfe:2006-15 Do macro variables, asset markets, or surveys forecast inflation better? (2006). Finance and Economics Discussion Series (12) RePEc:fip:fedker:y:2006:i:qi:p:43-85:n:v.91no.1 The trend growth rate of employment : past, present, and future (2006). Economic Review (13) RePEc:fip:fedkrw:rwp06-09 Forecasting of small macroeconomic VARs in the presence of instabilities (2006). Research Working Paper (14) RePEc:fip:fedkrw:rwp06-12 Averaging forecasts from VARs with uncertain instabilities (2006). Research Working Paper (15) RePEc:nbr:nberte:0326 Approximately Normal Tests for Equal Predictive Accuracy in Nested Models (2006). NBER Technical Working Papers (16) RePEc:pen:papers:06-019 Time Series Analysis (2006). PIER Working Paper Archive (17) RePEc:pra:mprapa:180 Comparing Models of Macroeconomic Fluctuations: How Big Are the Differences? (2006). MPRA Paper (18) RePEc:prt:dpaper:7_2006 Inflation Forecasts, Monetary Policy and Unemployment Dynamics: Evidence from the US and the Euro Area (2006). Discussion Papers (19) RePEc:rdg:icmadp:icma-dp2006-09 Momentum Profits and Time-Varying Unsystematic Risk (2006). (20) RePEc:rio:texdis:531 Realized volatility: a review (2006). Textos para discussão (21) RePEc:rut:rutres:200615 The Incremental Predictive Information Associated with Using Theoretical New Keynesian DSGE Models Versus Simple Linear Alternatives (2006). Departmental Working Papers (22) RePEc:rut:rutres:200617 International Evidence on the Efficacy of new-Keynesian Models of Inflation Persistence (2006). Departmental Working Papers (23) RePEc:uts:rpaper:175 Volatility Forecast Comparison using Imperfect Volatility Proxies (2006). Research Paper Series (24) RePEc:vcu:wpaper:0602 International Evidence on the Efficacy of new-Keynesian Models of Inflation Persistence (2006). Working Papers (25) RePEc:wiw:wiwrsa:ersa06p196 Regional Unemployment Forecasting Using Structural Component Models With Spatial Autocorrelation (2006). ERSA conference papers (26) RePEc:wrk:warwec:772 Internal consistency of survey respondents.forecasts : Evidence based on the Survey of Professional Forecasters (2006). The Warwick Economics Research Paper Series (TWERPS) (27) RePEc:wrk:warwec:773 Macroeconomic Forecasting with Mixed Frequency Data : Forecasting US output growth and inflation. (2006). The Warwick Economics Research Paper Series (TWERPS) (28) RePEc:wrk:warwec:774 Forecast Encompassing Tests and Probability Forecasts (2006). The Warwick Economics Research Paper Series (TWERPS) (29) RePEc:wrk:warwec:777 Quantile Forecasts of Daily Exchange Rate Returns from Forecasts of Realized Volatility (2006). The Warwick Economics Research Paper Series (TWERPS) Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||