|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

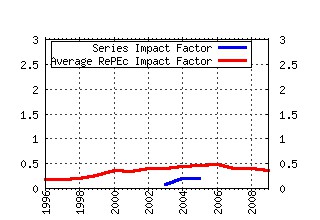

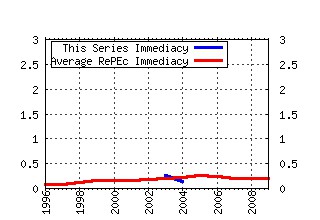

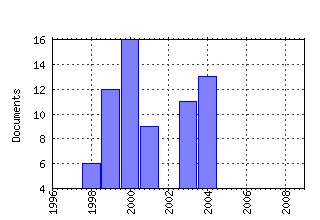

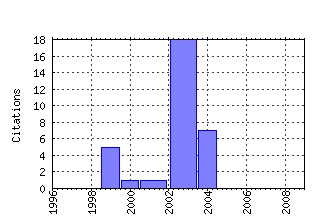

Finance Lab Working Papers Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:ibm:finlab:flwp_48 Small Sample Properties of GARCH Estimates and Persistence (2003). (2) RePEc:ibm:finlab:flwp_68 Endogenous Collateral (2004). (3) RePEc:ibm:finlab:flwp_57 Generalized Hyperbolic Distributions and Brazilian Data (2003). (4) RePEc:ibm:finlab:flwp_14 Alternative Models to extract asset volatility: a comparative study (1999). (5) RePEc:ibm:finlab:flwp_54 Put-Call Duality and Symmetry (2003). (6) RePEc:ibm:finlab:flwp_49 Evaluating an Alternative Risk Preference in Affine Term Structure Models (2003). (7) RePEc:ibm:finlab:flwp_12 Índice de Sharpe e outros Indicadores de Performance Aplicados a Fundos de Ações Brasileiros (1999). (8) RePEc:ibm:finlab:flwp_55 Goodness-of-fit Tests focus on VaR Estimation (2003). (9) RePEc:ibm:finlab:flwp_37 A Jump Difusion Yield Factor Model of Interest Rate (2001). (10) RePEc:ibm:finlab:flwp_34 Inflation, output and stock prices: evidence from Brazil (2000). (11) RePEc:ibm:finlab:flwp_59 How Persistent is Volatility? An Answer with Stochastic Volatility Models with Markov Regime Switching State Equations (2004). (12) RePEc:ibm:finlab:flwp_53 Volatility Estimation and Option Pricing with Fractional Brownian Motion (2003). (13) RePEc:ibm:finlab:flwp_58 Analyzing the Use of Generalized Hyperbolic Distributions to Value at Risk Calculations (2003). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 Recent citations received in: 2008 Recent citations received in: 2007 Recent citations received in: 2006 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||