|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

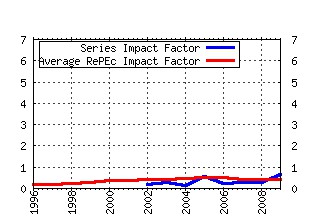

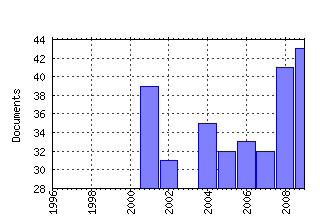

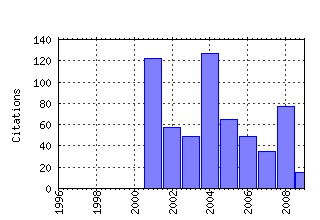

Journal of Forecasting Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:jof:jforec:v:23:y:2004:i:6:p:405-430 Combination forecasts of output growth in a seven-country data set (2004). (2) RePEc:jof:jforec:v:20:y:2001:i:3:p:161-79 Impulse Response Analysis in Vector Autoregressions with Unknown Lag Order. (2001). (3) RePEc:jof:jforec:v:26:y:2007:i:4:p:271-302 Forecasting German GDP using alternative factor models based on large datasets (2007). (4) RePEc:jof:jforec:v:27:y:2008:i:3:p:217-235 Single-index and portfolio models for forecasting value-at-risk thresholds (2008). (5) RePEc:jof:jforec:v:24:y:2005:i:2:p:77-103 Forecasting recessions using the yield curve (2005). (6) RePEc:jof:jforec:v:27:y:2008:i:1:p:1-19 Forecasting value-at-risk with a parsimonious portfolio spillover GARCH (PS-GARCH) model (2008). (7) RePEc:jof:jforec:v:27:y:2008:i:3:p:237-265 How successful are dynamic factor models at forecasting output and inflation? A meta-analytic approach (2008). (8) RePEc:jof:jforec:v:23:y:2004:i:7:p:479-496 Finding good predictors for inflation: a Bayesian model averaging approach (2004). (9) RePEc:jof:jforec:v:20:y:2001:i:8:p:581-601 Forecasting with k-Factor Gegenbauer Processes: Theory and Applications. (2001). (10) RePEc:jof:jforec:v:23:y:2004:i:3:p:173-196 Vector smooth transition regression models for US GDP and the composite index of leading indicators (2004). (11) RePEc:jof:jforec:v:22:y:2003:i:1:p:1-22 Volatility forecasting for risk management (2003). (12) RePEc:jof:jforec:v:20:y:2001:i:2:p:87-109 Evaluating the Predictive Accuracy of Volatility Models. (2001). (13) RePEc:jof:jforec:v:21:y:2002:i:7:p:513-42 The Performance of Non-linear Exchange Rate Models: A Forecasting Comparison. (2002). (14) RePEc:jof:jforec:v:23:y:2004:i:6:p:431-447 Quarterly real GDP estimates for China and ASEAN4 with a forecast evaluation (2004). (15) RePEc:jof:jforec:v:20:y:2001:i:6:p:441-49 Creating High-Frequency National Accounts with State-Space Modelling: A Monte Carlo Experiment. (2001). (16) RePEc:jof:jforec:v:22:y:2003:i:5:p:359-375 On SETAR non-linearity and forecasting (2003). (17) RePEc:jof:jforec:v:25:y:2006:i:2:p:101-128 Evaluating predictive performance of value-at-risk models in emerging markets: a reality check (2006). (18) RePEc:jof:jforec:v:24:y:2005:i:3:p:189-201 Beating the random walk in Central and Eastern Europe (2005). (19) RePEc:jof:jforec:v:27:y:2008:i:6:p:537-549 Scalar BEKK and indirect DCC (2008). (20) RePEc:jof:jforec:v:25:y:2006:i:2:p:129-152 Autoregressive gamma processes (2006). (21) RePEc:jof:jforec:v:23:y:2004:i:8:p:541-557 Comparing the accuracy of density forecasts from competing models (2004). (22) RePEc:jof:jforec:v:21:y:2002:i:7:p:473-500 A Threshold Stochastic Volatility Model. (2002). (23) RePEc:jof:jforec:v:22:y:2003:i:4:p:337-358 Selection of Value-at-Risk models (2003). (24) RePEc:jof:jforec:v:20:y:2001:i:1:p:1-19 Testing in Unobserved Components Models. (2001). (25) RePEc:jof:jforec:v:23:y:2004:i:1:p:51-66 Forecasting football results and the efficiency of fixed-odds betting (2004). (26) RePEc:jof:jforec:v:25:y:2006:i:1:p:49-75 Building neural network models for time series: a statistical approach (2006). (27) RePEc:jof:jforec:v:24:y:2005:i:1:p:17-37 Prediction intervals for exponential smoothing using two new classes of state space models (2005). (28) RePEc:jof:jforec:v:29:y:2010:i:1-2:p:215-230 Dynamic probit models and financial variables in recession forecasting (2010). (29) RePEc:jof:jforec:v:22:y:2003:i:1:p:49-66 Subset threshold autoregression (2003). (30) RePEc:jof:jforec:v:21:y:2002:i:7:p:501-11 Forecasting Daily Foreign Exchange Rates Using Genetically Optimized Neural Networks. (2002). (31) RePEc:jof:jforec:v:20:y:2001:i:2:p:135-43 A Double-Threshold GARCH Model for the French Franc/Deutschmark Exchange Rate. (2001). (32) RePEc:jof:jforec:v:24:y:2005:i:8:p:575-592 Nowcasting quarterly GDP growth in a monthly coincident indicator model (2005). (33) RePEc:jof:jforec:v:27:y:2008:i:1:p:41-51 Can forecasting performance be improved by considering the steady state? An application to Swedish inflation and interest rate (2008). (34) RePEc:jof:jforec:v:21:y:2002:i:5:p:381-93 An Outlier Robust GARCH Model and Forecasting Volatility of Exchange Rate Returns. (2002). (35) RePEc:jof:jforec:v:23:y:2004:i:1:p:19-49 Medium-term forecasts of potential GDP and inflation using age structure information (2004). (36) RePEc:jof:jforec:v:25:y:2006:i:3:p:209-221 The importance of interest rates for forecasting the exchange rate (2006). (37) RePEc:jof:jforec:v:20:y:2001:i:6:p:425-40 Choosing among Competing Econometric Forecasts: Regression-Based Forecast Combination Using Model Selection. (2001). (38) RePEc:jof:jforec:v:21:y:2002:i:3:p:181-92 Relationships between Australian Real Estate and Stock Market Prices--A Case of Market Inefficiency. (2002). (39) RePEc:jof:jforec:v:26:y:2007:i:1:p:1-22 Forecasting inflation using economic indicators: the case of France The views expressed in the paper are those of the authors and do not necessarily reflect those of (2007). (40) RePEc:jof:jforec:v:21:y:2002:i:2:p:81-105 Testing for (Common) Stochastic Trends in the Presence of Structural Breaks. (2002). (41) RePEc:jof:jforec:v:20:y:2001:i:4:p:285-95 Robust Evaluation of Fixed-Event Forecast Rationality. (2001). (42) RePEc:jof:jforec:v:29:y:2010:i:1-2:p:186-199 GDP nowcasting with ragged-edge data: a semi-parametric modeling (2010). (43) RePEc:jof:jforec:v:27:y:2008:i:5:p:371-390 Short-term forecasts of euro area real GDP growth: an assessment of real-time performance based on vintage data (2008). (44) RePEc:jof:jforec:v:23:y:2004:i:4:p:275-296 Updating ARMA predictions for temporal aggregates (2004). (45) repec:jof:jforec:v:27:y:2008:i:7:p:621-636 (). (46) RePEc:jof:jforec:v:24:y:2005:i:7:p:523-537 The multi-chain Markov switching model (2005). (47) RePEc:jof:jforec:v:26:y:2007:i:2:p:77-94 The use of monthly indicators to forecast quarterly GDP in the short run: an application to the G7 countries (2007). (48) RePEc:jof:jforec:v:21:y:2002:i:8:p:543-58 Forecasting Trend Output in the Euro Area. (2002). (49) RePEc:jof:jforec:v:28:y:2009:i:2:p:167-182 Comparing the DSGE model with the factor model: an out-of-sample forecasting experiment (2009). (50) RePEc:jof:jforec:v:22:y:2003:i:4:p:299-315 Non-linear forecasts of stock returns (2003). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:iso:wpaper:0096 Prediction Accuracy of Different Market Structures Bookmakers versus a Betting Exchange (2009). Working Papers Recent citations received in: 2008 (1) RePEc:ces:ifowps:_57 Freedom of Choice in Macroeconomic Forecasting: An Illustration with German Industrial Production and Linear Models (2008). Ifo Working Paper Series (2) RePEc:cpr:ceprdp:6708 Factor-MIDAS for now- and forecasting with ragged-edge data: A model comparison for German GDP (2008). CEPR Discussion Papers (3) RePEc:eui:euiwps:eco2008/16 Factor-MIDAS for Now- and Forecasting with Ragged-Edge Data: A Model Comparison for German GDP (2008). (4) RePEc:ihs:ihsesp:231 Optimizing Time-series Forecasts for Inflation and Interest Rates Using Simulation and Model Averaging (2008). Economics Series (5) RePEc:imf:imfwpa:08/46 External Linkages and Economic Growth in Colombia: Insights from A Bayesian VAR Model (2008). IMF Working Papers (6) RePEc:pit:wpaper:367 Exploiting Non-Linearities in GDP Growth for Forecasting and Anticipating Regime Changes (2008). Working Papers (7) RePEc:zbw:fubsbe:200810 Does money growth granger-cause inflation in the Euro Area? Evidence from output-of-sample forecasts using Bayesian VARs (2008). Discussion Papers Recent citations received in: 2007 (1) RePEc:ces:ifowps:_46 Assessing the Forecast Properties of the CESifo World Economic Climate Indicator: Evidence for the Euro Area (2007). Ifo Working Paper Series Recent citations received in: 2006 (1) RePEc:diw:diwvjh:75-2-2 Geschichte der quantitativen Konjunkturprognose-Evaluation in Deutschland (2006). Vierteljahrshefte zur Wirtschaftsforschung / Quarterly Journal of Economic Research (2) RePEc:fgv:epgewp:630 Are price limits on futures markets that cool? Evidence from the Brazilian

Mercantile and Futures Exchange (2006). Economics Working Papers (Ensaios Economicos da EPGE) Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||