|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

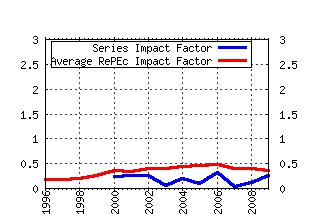

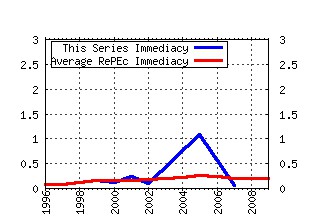

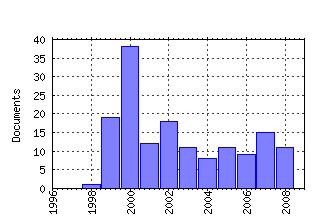

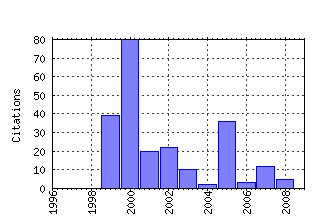

CoFE Discussion Paper Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:knz:cofedp:0005 Does the Governed Corporation Perform Better?

Governance Structures and Corporate Performance in Germany (2000). (2) RePEc:knz:cofedp:0004 Do Lending Relationships Matter? Evidence from Bank Survey Data in Germany (2000). (3) RePEc:knz:cofedp:0206 The processing of non-anticipated information in financial markets: Analyzing the impact of surprises in the employment report (2002). (4) RePEc:knz:cofedp:0504 Default risk sharing between banks and markets: the contribution of collateralized debt obligations (2005). (5) RePEc:knz:cofedp:9908 Local Polynomial Estimation with a FARIMA-GARCH Error Process (1999). (6) RePEc:knz:cofedp:0502 Incentive Contracts and Hedge Fund Management (2005). (7) RePEc:knz:cofedp:9901 When are Options Overpriced? The Black-Scholes Model and

Alternative Characterisations of the Pricing Kernel. (1999). (8) RePEc:knz:cofedp:0111 Iterative plug-in algorithms for SEMIFAR models - definition, convergence and asymptotic properties (2001). (9) RePEc:knz:cofedp:0509 Mispricing of S&P 500 Index Options (2005). (10) RePEc:knz:cofedp:9913 SEMIFAR Forecasts, with Applications to Foreign Exchange Rates (1999). (11) RePEc:knz:cofedp:0002 Horizontal and Vertical R&D Cooperation (2000). (12) RePEc:knz:cofedp:0104 Estimating the Neighborhood Influence on Decision Makers: Theory and an Application on

the Analysis of Innovation Decisions (2001). (13) RePEc:knz:cofedp:0105 Econometric Analysis of Financial Transaction Data: Pitfalls and Opportunities (2001). (14) RePEc:knz:cofedp:0507 An Experimental Test of the Impact of Overconfidence and Gender on Trading Activity (2005). (15) RePEc:knz:cofedp:9916 SEMIFAR Models - A Semiparametric Framework for Modelling Trends, Long

Range Dependence and Nonstationarity (1999). (16) RePEc:knz:cofedp:0016 Data-driven estimation of semiparametric fractional autoregressive models (2000). (17) RePEc:knz:cofedp:0510 The dynamics of overconfidence: Evidence from stock market forecasters (2005). (18) RePEc:knz:cofedp:0212 Simultaneously Modelling Conditional Heteroskedasticity and Scale Change (2002). (19) RePEc:knz:cofedp:0304 Schätzung ökonometrischer Modelle auf der Grundlage anonymisierter Daten (2003). (20) RePEc:knz:cofedp:0032 Commodity Taxation and international Trade in Imperfect Markets (2000). (21) RePEc:knz:cofedp:0303 A Dynamic Integer Count Data Model for Financial Transaction Prices (2003). (22) RePEc:knz:cofedp:0707 Estimating High-Frequency Based (Co-) Variances: A Unified Approach (2007). (23) RePEc:knz:cofedp:0608 Wie werden Collateralized Debt Obligation-Transaktionen gestaltet? (2006). (24) RePEc:knz:cofedp:9914 Volatility of Stock Market Indices - An Analysis based on SEMIFAR Models (1999). (25) RePEc:knz:cofedp:0806 Modelling and Forecasting Multivariate Realized Volatility (2008). (26) RePEc:knz:cofedp:9904 Misspecified heteroskedasticity in the panel probit model:

A small sample comparison of GMM and SML estimators (1999). (27) RePEc:knz:cofedp:0305 Multiplicative Background Risk (2003). (28) RePEc:knz:cofedp:0708 Two-Dimensional Risk-Neutral Valuation Relationships for the Pricing of

Options. (2007). (29) RePEc:knz:cofedp:0205 Modelling Intraday Trading Activity Using Box-Cox-ACD Models (2002). (30) RePEc:knz:cofedp:9906 The Service Sentiment Indicator - A Business Climate Indicator for the

German Business - Related Services Sector (1999). (31) RePEc:knz:cofedp:0019 Nonparametric M-Estimation with Long-Memory Errors (2000). (32) RePEc:knz:cofedp:0809 Recovering Delisting Returns of Hedge Funds (2008). (33) RePEc:knz:cofedp:0706 Hydrodynamics from kinetic models of conservative economies (2007). (34) RePEc:knz:cofedp:9919 Volatility Estimation on the Basis of Price Intensities (1999). (35) RePEc:knz:cofedp:0037 Modifying the double smoothing bandwidth selector in nonparametric regression (2000). (36) RePEc:knz:cofedp:0108 Heterogeneity of Investors and Asset Pricing in a Risk-Value World (2001). (37) RePEc:knz:cofedp:9918 SEMIFAR Models, with Applications to Commodities, Exchange Rates and the

Volatility of Stock Market Indices (1999). (38) RePEc:knz:cofedp:0033 Taxation of Investment and Finance in an International Setting: Implications for Tax Competition (2000). (39) RePEc:knz:cofedp:0710 Information asymmetries and securitization design (2007). (40) RePEc:knz:cofedp:9909 Backward Stochastic Differential Equations and Stochastic Controls: A New

Perspective (1999). (41) RePEc:knz:cofedp:0405 Why Do Asset Prices Not Follow Random Walks? (2004). (42) RePEc:knz:cofedp:0022 Temporal aggregation of stationary and nonstationary FARIMA (p, d, 0) models (2000). (43) RePEc:knz:cofedp:0703 Customer Trading in the Foreign Exchange Market: Empirical Evidence from an Internet Trading Platform (2007). (44) RePEc:knz:cofedp:9903 Analyzing the Time between Trades with a Gamma Compounded Hazard Model.

An Application to LIFFE Bund Future Transactions (1999). (45) RePEc:knz:cofedp:9917 Tacit Collusion under Destination - and Origin-Based Commodity Taxation (1999). (46) RePEc:knz:cofedp:0009 On the Relationship of Information Processes and Asset Price Processes (2000). (47) RePEc:knz:cofedp:0404 Conditionally parametric fits for CAPM betas (2004). (48) RePEc:knz:cofedp:0020 Determinants of Inter-Trade Durations and Hazard Rates Using Proportional Hazard ARMA Model (2000). (49) RePEc:knz:cofedp:0701 Dynamic Modeling of Large Dimensional Covariance Matrices (2007). (50) RePEc:knz:cofedp:0506 Option Pricing: Real and Risk-Neutral Distributions (2005). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 Recent citations received in: 2008 Recent citations received in: 2007 (1) RePEc:knz:cofedp:0702 Panel Intensity Models with Latent Factors: An Application to the Trading Dynamics on the Foreign Exchange Market¤ (2007). CoFE Discussion Paper Recent citations received in: 2006 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||