|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

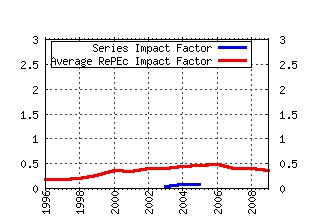

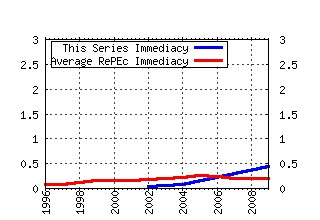

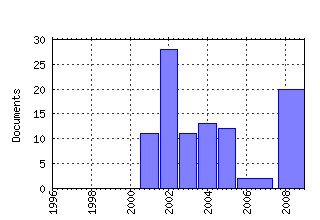

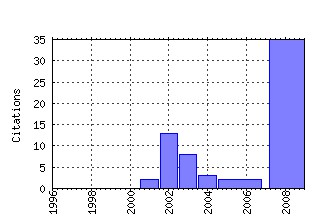

Documentos del Instituto Complutense de Análisis Económico Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:ucm:doicae:0910 The Ten Commandments for Optimizing Value-at-Risk and Daily Capital Charges (2009). (2) RePEc:ucm:doicae:0907 A Decision Rule to Minimize Daily Capital Charges in Forecasting Value-at-Risk (2009). (3) RePEc:ucm:doicae:0904 Do We Really Need Both BEKK and DCC? A Tale of Two Covariance Models (2009). (4) RePEc:ucm:doicae:0918 Has the Basel II Accord Encouraged Risk Management During the 2008-09 Financial Crisis? (2009). (5) RePEc:ucm:doicae:0309 Flexible Tool for Model Building: the Relevant Transformation of the Inputs Network Approach (RETINA) (2003). (6) RePEc:ucm:doicae:1101 International Evidence on GFC-robust Forecasts for Risk Management under the Basel Accord (2011). (7) RePEc:ucm:doicae:0906 Modelling International Tourist Arrivals and Volatility: An Application to Taiwan (2009). (8) RePEc:ucm:doicae:1102 Risk Management of Risk under the Basel Accord: Forecasting Value-at-Risk of VIX Futures (2011). (9) RePEc:ucm:doicae:0203 A Note on the Pseudo-Spectra and the Pseudo-Covariance Generating Functions of ARMA Processes (2002). (10) RePEc:ucm:doicae:1132 Risk Management of Risk Under the Basel Accord: A Bayesian Approach to Forecasting Value-at-Risk of

VIX Futures (2011). (11) RePEc:ucm:doicae:1001 GFC-Robust Risk Management Strategies under the Basel Accord (2009). (12) RePEc:ucm:doicae:1114 Great Expectatrics: Great Papers, Great Journals, Great Econometrics (2011). (13) RePEc:ucm:doicae:0202 A Dynamic Model of Final Service Competition in fixed Electronic Communications under a Capacity

Interconnection Regime (2002). (14) RePEc:ucm:doicae:0403 The Welfare Cost of Business Cycles in an Economy with Nonclearing Markets (2004). (15) RePEc:ucm:doicae:0201 A flexible Tool for Model Building: the Relevant Transformation of the Inputs Network Approach (RETINA) (2002). (16) RePEc:ucm:doicae:0216 Dynamic Laffer Curve in an Endogenous Growth Model with Pollution (2002). (17) RePEc:ucm:doicae:0915 Modelling the Growth and Volatility in Daily International Mass Tourism to Peru (2009). (18) RePEc:ucm:doicae:0504 Fast estimation methods for time series models in state-space form (2005). (19) repec:ucm:doicae:0102 (). (20) RePEc:ucm:doicae:0223 Optimal hedging under departures from the cost-of-carry valuation: evidence from the Spanish stock

index futures market (2002). (21) RePEc:ucm:doicae:0409 Characterizing the Optimal Composition of Government Expenditures (2004). (22) RePEc:ucm:doicae:0222 An Error Correction Factor Model of Term Structure Slopes in International Swaps Markets (2002). (23) RePEc:ucm:doicae:0218 Analysis and Comparisons of some Solution Concepts for Stochastic Programming Problems (2002). (24) RePEc:ucm:doicae:1106 Why do variance swaps exist? (2011). (25) RePEc:ucm:doicae:0110 Structural Breaks and interest rates forecast: a sequential approach (2001). (26) RePEc:ucm:doicae:0301 Trade Shoks and Aggregate Fluctuations in an Oil-Exporting Economy (2003). (27) RePEc:ucm:doicae:0204 An ARMA Representation of Unobserved Component Models under Generalized Random Walk Specifications:

New Algorithms and Examples (2002). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 (1) RePEc:cte:wsrepe:ws097222 Comparing univariate and multivariate models to forecast portfolio value-at-risk (2009). Statistics and Econometrics Working Papers (2) RePEc:dgr:uvatin:20090039 Has the Basel II Accord Encouraged Risk Management During the 2008-09 Financial Crisis? (2009). Tinbergen Institute Discussion Papers (3) RePEc:pra:mprapa:20975 Optimal Risk Management Before, During and After the 2008-09 Financial Crisis (2009). MPRA Paper (4) RePEc:tky:fseres:2009cf639 Volatility Spillovers Between Crude Oil Futures Returns and Oil Company Stocks Return (2009). CIRJE F-Series (5) RePEc:tky:fseres:2009cf640 Modelling Conditional Correlations for Risk Diversification in Crude Oil Markets (2009). CIRJE F-Series (6) RePEc:tky:fseres:2009cf641 Forecasting Volatility and Spillovers in Crude Oil Spot, Forward and Futures Markets (2009). CIRJE F-Series (7) RePEc:tky:fseres:2009cf643 Has the Basel II Accord Encouraged Risk Management During the 2008-09 Financial Crisis? (2009). CIRJE F-Series (8) RePEc:ucm:doicae:0906 Modelling International Tourist Arrivals and Volatility: An Application to Taiwan (2009). Documentos del Instituto Complutense de Análisis Económico (9) RePEc:ucm:doicae:1001 GFC-Robust Risk Management Strategies under the Basel Accord (2009). Documentos del Instituto Complutense de Análisis Económico Recent citations received in: 2008 Recent citations received in: 2007 Recent citations received in: 2006 Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||