|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

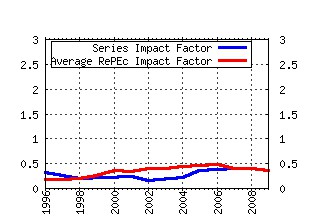

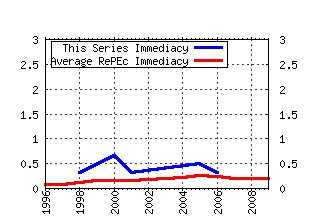

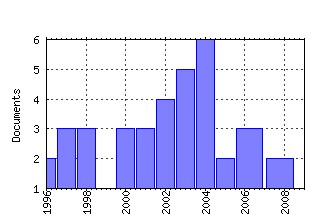

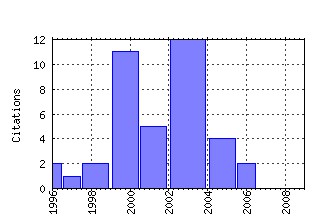

HSC Research Reports Raw citation data, Impact Factor, Immediacy Index, Published documents, Citations received, , Most cited papers , Recent citations and documents published in this series in EconPapers.

Most cited documents in this series: (1) RePEc:wuu:wpaper:hsc0301 Modeling electricity prices: jump diffusion and regime switching (2003). (2) RePEc:wuu:wpaper:hsc0001 Hurst analysis of electricity price dynamics (2000). (3) RePEc:wuu:wpaper:hsc0103 Estimating long range dependence: finite sample properties and confidence intervals (2001). (4) RePEc:wuu:wpaper:hsc9401 Can One See Alpha-stable Variables and Processes? (1994). (5) RePEc:wuu:wpaper:hsc0502 Heavy tails and electricity prices (2005). (6) RePEc:wuu:wpaper:hsc0003 Property insurance loss distributions (2000). (7) RePEc:wuu:wpaper:hsc0304 An introduction to simulation of risk processes (2003). (8) RePEc:wuu:wpaper:hsc0002 Energy price risk management (2000). (9) RePEc:wuu:wpaper:hsc0601 Short-term electricity price forecasting with time series models: A review and evaluation (2006). (10) RePEc:wuu:wpaper:hsc9601 Correction to: On the Chambers-Mallows-Stuck Method for Simulating Skewed Stable Random Variables (1996). (11) RePEc:wuu:wpaper:hsc9801 Origins of the scaling behaviour in the dynamics of financial data (1998). (12) RePEc:wuu:wpaper:hsc9802 Scaling in currency exchange: A Conditionally Exponential Decay approach (1998). (13) RePEc:wuu:wpaper:hsc0101 Levy-stable distributions revisited: tail index > 2 does not exclude the Levy-stable regime (2001). (14) RePEc:wuu:wpaper:hsc0501 Modeling catastrophe claims with left-truncated severity distributions (extended version) (2005). (15) RePEc:wuu:wpaper:hsc1102 Efficient estimation of Markov regime-switching models: An application to electricity spot prices (2011). (16) RePEc:wuu:wpaper:hsc9703 Spectral representation and structure of self-similar processes (1997). (17) RePEc:wuu:wpaper:hsc1003 Building Loss Models (2010). (18) RePEc:wuu:wpaper:hsc9702 The Lamperti transformation for self-similar processes (1997). Recent citations received in: | 2009 | 2008 | 2007 | 2006 Recent citations received in: 2009 Recent citations received in: 2008 Recent citations received in: 2007 Recent citations received in: 2006 (1) RePEc:pra:mprapa:1363 Point and interval forecasting of wholesale electricity prices: Evidence from the Nord Pool market (2006). MPRA Paper Warning!! This is still an experimental service. The results of this service should be interpreted with care, especially in research assessment exercises. The processing of documents is automatic. There still are errors and omissions in the identification of references. We are working to improve the software to increase the accuracy of the results. Source data used to compute the impact factor of RePEc series. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||